The Thursday Report – 1.15.15 – On the First Day of Heckerling…

The Five Days of Heckerling Poem

Gassman Law Associates in the News

-

Biel Rio, Cheese, and Proceedings Supplementary

-

Bay News 9 Article and Appearance

Florida Law Trivia, Part I

Avoiding Disaster on Highway 709 – 9 Common Mistakes Related to Spousal Gift Splitting

Richard Connolly’s World – IRS Commissioner Predicts Miserable 2015 Tax Filing Season

Thoughtful Corner – Check Email Less to Reduce Stress

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

The Five Days of Heckerling

The Five Days of Heckerling

by Alan Gassman, Kristen Sweeney, and Chris Denicolo

(Don’t forget to read the footnotes!)

On the first day of Heckerling,

My love Marcia said to me,

“Stay away until the end of the week.”

I drove to Orlando; it was better than Disney!

There was a JEST talk by Howard Zaritsky[1].

On the second day of Heckerling,

Donaldson said to me,

Clayton QTIPs work wonderfully.

The Interactive booth was all one big party.

With Marty Shenkman, Natalie Choate, and tax geeks.

On the third day of Heckerling,

Blattmachr said to thee,

Use the SPLAT for a house on the beach (instead of a QPRT).

Jerry Hesch told me planning news, a thrill you need to seek,

And some issues that the IRS leaked.

On the fourth day of Heckerling,

Someone said to me,

“Are you and your partners serious or just JEST-ing?”

I think my favorite sponsor is Bloomberg BNA

Aen Webster let my smart aleck footnote stay[2].

On the fifth day of Heckerling,

Everyone starts to flee,

We’ll all be back in 2016!

Then on the Monday after Heckerling, my assistant shrieked at me:

You have twelve clients waiting,

Eleven new estate plans,

Ten dozen unanswered voicemails,

Nine new probate cases,

Eight letters pending,

Seven revised petitions,

Six angry attorneys,

FIVE IRS CLEARANCE LETTERS!!! 🙂

Four notebooks lost,

Three articles due,

Two binders of bills to review…

Oh, how long until the next Heckerling???

The Thursday Report would like to thank professional writer Kristen Sweeney for her assistance in the writing of this poem.

*********************************************

[1] I rose 7 feet in the air

When Howard was kind enough to compare

The JEST designed with my partner Chris Denicolo

In a way that I didn’t have to wear my helmet for polo.

Here’s what Howard said: “Alan Gassman and a couple of other lawyers…created what they call “The Joint Estate Step-Up Trust” or “JEST.” Okay, I kind of like that acronym. I am not a big fan of acronyms, but at least it is a word. DSUEA is not a word, and I really do not like using it. At least JEST is something. I think the JEST is a great technique for what it is seeking to do.” For his complete comments on the JEST system, please click here.

[2] Our Bloomberg BNA article on the Bifani case called “Way Down Upon the Bifani River” had the following footnote, which is important for an understanding of the case and Florida homestead: “The Suwannee River is a 246 mile black water river that can take you much of the way from the Bankruptcy Court in Tampa to the 11th Circuit Court of Appeals in New Orleans, which is where this case went before the debtor’s raft sank, made famous by Stephen Foster’s song, “Old Folks at Home” (Foster never saw the river but read about it). Mr. Gassman owns two lots on this river that he bought in 2007 and would gladly sell for half of what he paid, no extra charge for the alligators who live there. See Way Down Upon the Suwannee River Far Far Away, LLC on the Sunbiz Website, and also Hey Hey Santa Fey (river), LLC and Withlacoochee Coochee-Coo, LLC, which own his other failed river investments. This article is dedicated to the memory of Joan Rivers, who performed in Tampa Bay shortly before her death at age 81 with great energy and physical strength.”

Martin M. Shenkman

We have been enjoying our week at the 49th Annual Heckerling Institute on Estate Planning in Orlando. If you’ve missed this superb event, Marty Shenkman’s amazing and thorough daily write-ups on the sessions at Heckerling can be viewed on Steve Leimberg’s LISI (Leimberg Information Services, Inc.) service.

For an example of how tight and accurate Marty’s write-ups are, please click here.

The following appears in Marty’s write-up concerning the JEST system:

- With portability, you are not as concerned with the problem of the first spouse not having money. In fact, the best portability comes from an insolvent estate of the first spouse. They got no use of their exemption. The only problem is convincing them to file a federal estate tax return. This can be a little tricky. Somebody has to pay for preparing the return.

- The problem of 1014(e) was addressed by Alan Gassman and a couple of other lawyers in a series of articles – where they created what they call “The Joint Estate Step-Up Trust” (or “JEST”).

- The concept looks a great deal like the tax basis revocable trust, with one very clever distinction, and that is that the assets of the donor surviving spouse that are includible only because of the General Power of Appointment (where the first spouse to die does not have enough assets to fully fund their exemption) to bring the estate up to the exemption amount, which are thus includible only because of 2041, and are attributable to the property that was owned by and contributed by the surviving spouse. These will go into a non-marital trust that the surviving spouse is not a beneficiary of, and the rest is for marital deduction funding. That absolutely ought to work in terms of 1014(e).

- You still have the question of whether the spousal gift is the moment before or the moment after, and when you are explaining the technique to the client in writing, you need to point out this one little tiny item of uncertainty. You can state that you think it unlikely that this will be a problem – that all the private rulings take favorable positions. All of them. There are none taking an unfavorable position. That’s something. We can cite them, but we can’t rely on them, but it is still something.So they have some significance.

- Once the client can get past that one little piece of risk, I think the JEST is a great technique for what it is seeking to do. It is a way to minimize the problems of 1014(e). I commented earlier that you can accomplish the same concept if you are dealing with an inter-spousal gift within one year of death, you say “fine, the access I was given within one year of death is a little different – non-marital trust. It is a great technique– – the cases I mentioned about the – whether or not it is really a general power. I had a debate with Mitch Ganns, who said – the rulings don’t really say that, and I went back and read them, and said, yes they do really say in my opinion they really do say that, and while Mitch is one of those people I usually defer to in judgment – I really disagree on this one.

- So, the JEST actually is a workable technique to get the basis step-up on the estate of the spouse to die, when they don’t have money or enough money. It is a way around 1014(e) – the tax basis revocable trust – not so much.

- The JEST is a material improvement.

- Page 201 – I’ve got to say, that Alaska and now, Tennessee, community property trust is probably the simple best basis play in estate planning, and no one seems to be using it, and I am a little – I think it is outrageous that it isn’t being proposed more often, but there it is.

- We mentioned that community property has a really swell rule that both sides get a basis step-up on the first spouse’s death. (Howard continued to cover the Alaska and Tennessee Community Property Trust discussion, stating that it is the best technique available).

You can get a free trial subscription to LISI or sign in as a member to read the rest of Marty’s remarkable reports by clicking here.

Gassman Law Associates in the News

Biel Rio, Cheese, and Proceedings Supplementary

The December 18th and January 1st editions of the Thursday Report featured write-ups on the Florida District Court of Appeals Biel Rio case, where it was determined that a debtor who had engaged in a fraudulent transfer more than four years before was nevertheless subject to having the transfer set aside under a proceedings supplementary brought in state court by the creditor.

The solution to this would’ve been for the debtor to file bankruptcy, as explained in our new Leimberg commentary letter that is being released tonight on the Leimberg system. To view our Leimberg letter, please click here. This is not to be confused with limburger cheese or Charles Lindbergh, although Steve Leimberg likes cheese and probably could fly an airplane across the Atlantic Ocean.

If you are not subscribed to the Leimberg system, we highly recommend that you click here and sign up for a free trial. Try it; you’ll like it, whether that’s the Leimberg system or limburger cheese, which reminds us of the Monty Python Cheese Shop skit, which you can watch by clicking here. (There will doubtlessly be more clicks on the Monty Python skit than on our article, which we promise to not take personally – well, not too personally!) For a write-up on limburger cheese, click here. It may smell like sulfur, but it tastes somewhat better. Buy 12, get one brie!

And now for something completely different!

Bay News 9 Article & Appearance

Bay News 9 was kind enough to profile our book entitled The Florida Legal Guide for Same-Sex Couples on their website. The complete article can be viewed by clicking here and reads as follows:

Clearwater Attorney Writes Book, Helps Same-Sex Couples

by Chris Hopper, Reporter

Marriage can be wonderful, but if you’re not sure of all the legal challenges, the process can also be a nightmare.

“There are a myriad of legal and tax issues that face somebody deciding whether or not to get married,” said Alan Gassman, a Clearwater attorney.

Same-sex couples across the state of Florida tied the knot for the first time on Tuesday, January 6.

It was a joyous moment for thousands, but with that happiness comes some new legal challenges. To understand the legal complications of marriage, Gassman wrote a book called The Florida Legal Guide for Same-Sex Couples.

“I really felt that there was a need for this type of information,” said Gassman.

Gay or straight, the average person couldn’t possibly know all the rules off-hand.

“Things like your homestead property settlements, alimony obligations, a dramatic change in your social security rights, the list just goes on and on,” Gassman said.

It took Gassman and his team hundreds of hours to put together all the research.

“A same-sex couple that has been together 15 to 20 years now getting married are going to be treated much differently, they typically have separate property, they have separate children, they have a myriad of considerations.”

Gassman said it’s not about spoiling the celebration for same sex couples, it’s about helping them navigate the journey.

People can buy Gassman’s book on Amazon for their Kindle.

When the video becomes available on the Bay News 9 website, we will be sure to link to it in a future Thursday Report. Sorry we didn’t know that they were going to film Alan’s desk, which was allegedly a bit messy!

Thanks to reporter Chris Hopper, who can be reached by clicking here.

To purchase the Kindle edition of our book for only $0.99, please click here.

Florida Law Trivia, Part I

The first three people to email us all six correct answers will get an advanced copy of questions 7 through 12!

- Unless the Operating Agreement or Articles of Organization provide _____________ to the LLC having a manager or being managed by its members, the LLC will be treated as a member-managed LLC.

- Words of wisdom

- Words of similar import

- Words of similar export

- Whatever words you want

ANSWER: (B) The new LLC Act in Florida may override the Operating Agreement so that the majority of members can override the managing member depending upon the terms of the Operating Agreement and/or Articles of Organization. Unless the operating agreement or articles of organization provide “words of similar import” to the LLC having a manager or being managed by its members, the LLC will be treated as a member-managed LLC. Florida Statute § 605.0407(1)(b) specially provides that “words of similar import” do not, in and of themselves, include the terms managing member or managing members. If all of the members are managing members, then essentially there will be no change to the management of the LLC under the new Act.

- The Florida Homestead Tax Exemption is usually $25,000.

TRUE or FALSE

ANSWER: FALSE. The Florida Homestead Tax Exemption, which is normally $50,000 and also prevents escalation of appraised value by the greater of the CPI or three percent (3%) per year, can cause significant confusion and loss of opportunities. The homestead must be the primary residence of the owner or owners by December 31 of the year before the exemption begins to apply, and the owner or owners must apply for the Homestead Tax Exemption on or before March 1st of the following calendar year. Instructions are provided by the county property appraiser.

- The property appraiser sends a Notice of Proposed Property Taxes, or a _____________ notice in August, and the owner has 25 days to contest the proposed value after receiving the notice.

- Truth-in-Lending

- Truth and Lies

- Truth or Dare

- Truth-in-Millage

ANSWER: (D) The Truth-in-Millage, or TRIM, Notice contains the property’s value on January 1, the millage rates proposed by each local government, and an estimate of the amount of property taxes owed based on the proposed millage rates. The date, time, and location of each local government’s budget hearing are also provided on the notice. This provides property owners the opportunity to attend the hearings and comment on the millage rates before approval.

- Equity from a protected homestead can be sold and used to invest in mutual funds without being considered a fraudulent transfer.

TRUE or FALSE

ANSWER: FALSE. Equity from a protected homestead that is sold can only be safely used to purchase a protected replacement homestead or to open a designated bank account that is used to purchase a protected homestead without being considered a fraudulent transfer. While all other exempt assets can be converted into other exempt assets without being considered a fraudulent transfer, proceeds from the sale of a homestead that are transferred to a non-homestead-exempt asset will not be considered exempt.

- Post October 1, 2011, a __________________ will only permit an agent to act with respect to items specifically described in the Power of Attorney and will not authorize a number of acts to be taken unless they have been specifically authorized and initialed or separately signed under by the principal.

- Durable Power of Attorneys

- Weak Power of Attorneys

- Trusts

- Court Orders

ANSWER: (A) This Florida law will not prevent an out-of-state power of attorney that is in compliance with the law of another state to be given full force and effect. Pre-October 1, 2011, springing powers of attorney will still be honored but only if an affidavit delivered by the principal’s primary care physician states that: (1) the physician is licensed to practice medicine, (2) the physician is the primary care physician of the principal, and (3) that the physician believes the principal lacks the capacity to manage property.

- Florida Statute § 222.21 has not always provided that inherited IRAs were exempt from the creditors of beneficiaries.

TRUE or FALSE

ANSWER: TRUE. Fla. Stat. § 222.21 did not always provide that inherited IRAs were exempt from the creditors of beneficiaries. In 2011, the statute was refined to expressly provide that IRA and qualified retirement plan benefits payable to a surviving spouse and other beneficiaries of the retirement plan participant or IRA owner will be creditor protected if the beneficiary resides in Florida. Therefore, inherited IRAs and rollover IRAs will be considered as exempt assets in bankruptcy or otherwise, as long as the beneficiary resides in Florida or another state that provides exemption for these assets.

BONUS: If a WAVE is a Florida girl in the Navy, and a WAC is a Florida girl in the Army, then what is a WHOCK?

ANSWER: The answer will appear next week. Get your guesses ready!

Stay tuned for more trivia in our next edition of The Thursday Report.

Avoiding Disaster on Highway 709

9 Common Mistakes Related to Spousal Gift Splitting

by Kenneth J. Crotty

When a husband and wife consent to “split gifts” for a given calendar year, all of the eligible gifts that they both made are considered as having been transferred one-half by each spouse. This applies even if the assets transferred were owned by one spouse individually and not jointly or as tenants by the entireties. If spouses elect to split gifts on a gift tax return, such election will also apply for GST purposes. The following three conditions must be met for spousal gift-splitting:

- Both spouses must be US Citizens or residents on the date of the gift.

- Both spouses must consent to having all of the eligible gifts made by each of them treated as having been made one-half each.

- The spouses must have been married when all of the gifts were made during the year and cannot divorce and remarry during the remainder of the calendar year. I.R.C. § 2513(a).

Below are 9 of the most common mistakes we see with respect to spousal gift-splitting and how to avoid them.

Mistake #1 – Not Making the Election Correctly

- If the spouses agree to split the gifts, they need to confirm that they have appropriately completed Boxes 12, 13, 14, and 18 of the Form 709. You can see a sample Form 709 by clicking here.

- If both spouses need to file gift tax returns, both spouses will need to sign each of the returns where indicated.

- If both spouses need to file gift tax returns, the spouses should file both of the individual gift tax returns together in one envelope to help the IRS process the returns and to avoid correspondence from the IRS. Form 709 Instructions, page 5 (I.R.S. 2012).

Mistake #2 – Forgetting to Make the Election

- Generally, consent to split gifts cannot be made after the later of:

- April 15th of the year following when the gifts were made (or October 15th if an extension is applied for) or

- The date the donor spouse files the gift tax return

- This prevents a couple from filing a gift tax return reporting all of the gifts as having been made by one spouse and then waiting to see if the return is audited before electing gift splitting.

Mistake #3 – Having the Donor’s Spouse Split the Gift to a Trust that the Donor’s Spouse is a Beneficiary of or to a Trust that the Donor’s Spouse is Likely to Receive Benefits From

- If a split gift is gifted to a trust that has the ability to benefit one or both spouses, then the split gift may not be effective, unless the couple can demonstrate that it is highly unlikely that the beneficiary spouse will receive any benefits from the trust.

- See Private Letter Ruling 200345038 and the case of William H. Robertson vs. Commissioner, 26 TC 246 (1956).

Mistake #4 – Thinking it is Too Late to Make the Election – One Possible Exception to the April 15th Deadline

- An election to split gifts may be made by spouses after April 15th of the year following when the gifts are made if:

- No gift tax return has been filed by either spouse by April 15th, and

- When the gift tax return for the year in question is filed, the spouses elect to split the gifts

- It is important to note, however, that a late gift tax return cannot be filed splitting gifts if a notice of deficiency has already been sent by the IRS.

Mistake #5 – Dead or Incompetent Spouses Can Make the Election

- The executor for a deceased spouse may consent to split a gift made prior to the death of the deceased spouse. Treas. Reg. § 25.2513-2(c).

- However, a donor may not split the gift with his or her deceased spouse if the gift is made after the spouse’s death. Rev. Rul. 55-506, 1955-2 C.B. 609.

- The guardian for a legally incompetent spouse may consent to split a gift.

Mistake #6 – Spouses May Not Remarry During the Year

- It is important to note that spouses can elect to split gifts that were made when they were married, but only if they do not divorce and then remarry during the remainder of the year.

- If the spouses divorce and one spouse remarries before the end of the year, then the gifts made while the spouses were married cannot be split.

- In the event that clients divorce and one client has made a large gift which was intended to be split, consider adding in a provision in a marriage settlement agreement to ensure gift-splitting remains viable.

Mistake #7 – The Split is on All Gifts by Both Spouses – No “Picking and Choosing”

- If spouses elect to split gifts, the election is effective with respect to all eligible gifts made by either spouse to any third party.

- It is not possible for the clients to pick to split only some of the gifts.

- The only exception to this rule is gifts to a spouse. These gifts may not be split.

Mistake #8 – Thinking the Election is Irrevocable

- Many practitioners believe that the election to split gifts is irrevocable. While this is generally true, the following exception applies.

- Either spouse may rescind the election to split gifts if:

- The consent was originally made on a return filed before April 15th of the year after the gifts were made, and

- The consent is rescinded before April 15th of the year after the gifts were made

Mistake #9 – Sometimes the Consenting Spouse Does Not Need to File a Gift Tax Return

- The consenting spouse does not need to file a gift tax return if only one spouse made gifts, and

- All of the gifts are present interests, and

- The total amount received by each donee from the donor spouse does not exceed twice the annual exclusion ($28,000 for 2014),

- Only the spouse making the gifts needs to file a gift tax return, and the consent of the spouse splitting the gifts must be granted on the gift tax return.

Next time, on Avoiding Disaster on Highway 709, we look at the confusion regarding the gift tax and GST annual exclusions.

Richard Connolly’s World

IRS Commissioner Predicts Miserable 2015 Tax Filing Season

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares with us pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature one of Richard’s recommendations with a link to the article.

This week, the article of interest is “IRS Commissioner Predicts Miserable 2015 Tax Filing Season” by Ashlea Ebeling. It was featured in Forbes magazine on November 4, 2014.

Richard’s description is as follows:

Internal Revenue Service Commissioner John Koskinen warned that close to half the people trying to reach the IRS by phone might not get through during the upcoming 2015 tax filing season. “Phone service could plummet to 53 percent,” he told an audience of tax practitioners at the AICPA National Tax Conference in Washington, D.C. today. That would be down from an already unacceptable 72 percent during the 2014 filing season. The average hold time projection: 34 minutes! What’s to blame? Budget woes.

National Taxpayer Advocate Nina Olson was even gloomier. “This filing season is going to be the worst filing season since I’ve been the National Taxpayer Advocate {2001}. I’d love to be proved wrong, but I think it will rival the 1985 filing season when returns disappeared.”

Please click here to read the article in its entirety, including a discussion on the five key factors that will complicate the upcoming filing season.

Thoughtful Corner

Check Email Less to Reduce Stress

by Alan S. Gassman and Stephanie Herndon

A recent study by the University of British Columbia shows that individuals who check their emails only periodically at preset times each day are less stressed and more efficient than those who check emails constantly.

We doubt that very many people were surprised at the results of this study, which took 124 busy undergraduate students, graduate students, and health care, finance, academia, administrative, and information technology professionals and put them into two groups.

For the first week of the study, the first group was told that they could keep their email inboxes open throughout the day and check them as often as they liked, notwithstanding whether doing so is inefficient or interruptive in the long-run. These participants continued to check their email at approximately the same rate they did prior to beginning the study.

The second group was told that they could only review emails at three set times during each business day. They were also instructed to keep their inboxes closed and turn off email notifications on their phones so they could not be interrupted by emails or text messages during any other time.

These instructions were reversed for the study’s second week – the group allowed to keep their inboxes open all day had to switch to only checking their emails three times per day, and the group formerly under restrictions were allowed free reign of their inboxes once again.

Throughout the two week study, participants also answered brief daily surveys about their stress levels and how much work they got done throughout their days.

It should come as no surprise that stress levels were high when the three-times-per-day rules were first imposed. Most participants reported this practice to be quite difficult to follow. The suspense of not knowing what emails were sitting unanswered, the necessity of not being able to use the checking of emails as a diversion from concentrated effort, and the general changing of an important workplace habit made the first week a big adjustment.

As participants got used to their new routines, however, the group that was only checking emails three times per day reported feeling much less stressed and getting much more done! Their minds knew that they would not be interrupted by emails and that their work plans and patterns would not have to change with continuous and spontaneous interruption of thought.

When was the last time you looked down from 30,000 feet in the clouds to think through whether your email response system and habits are optimum for you, your team, and your clients?

Do clients want an immediate response, or would they rather have their work done by a professional who is thinking clearly, deliberately, and efficiently, without experiencing constant interruptions?

A number of very well respected and very busy professionals simply do not answer emails until the end of the day or sometimes even the next day.

The next time you are in line to buy a coffee, get a prescription filled, or get your second martini, check your thoughts instead of your emails. Make a date to think through how you should best be handling your emails and other office interruptions. Turn off your monitor and your iPhone and think about how to best live your life during a decade filled with distractions and an expectation of 24/7 availability.

Please email this to a friend and ask for an immediate response.

For more on the study referenced in this article, please click here.

Upcoming Seminars and Webinars

LIVE FLORIDA BAR FORT LAUDERDALE REPRESENTING THE PHYSICIAN LAW CONFERENCE:

Alan Gassman will speak at the 2015 Representing the Physician Seminar on the topic of DISASTER AVOIDANCE FOR THE DOCTOR’S ESTATE PLAN.

Please consider attending the Florida Bar 2015 Representing the Physician Seminar at the beautiful Renaissance Fort Lauderdale Cruise Port Hotel in Fort Lauderdale on Friday, January 16, 2015.

Start a great weekend there and then work yourself down to South Beach or stay at The Breakers in West Palm.

The topics (and speakers) are unbeatable. We thank chair Lester Perling for doing most of the work on this annual conference.

Date: January 16, 2015

Location: Renaissance Fort Lauderdale Cruise Port Hotel, 1617 SE 17th Street, Ft. Lauderdale, FL.

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com or click here to download the registration package.

********************************************************

LIVE TAMPA PRESENTATION:

Alan Gassman will speak at the Tampa Bay Estate Planning Council Dinner Program on the topic of PLANNING WITH RETIREMENT ACCOUNTS. We have put a great many hours of time into a comprehensive, easy-to-understand outline that we plan to have become a book on this topic. Satisfaction guaranteed!

Date: January 21, 2015 | 5:30 p.m. – 7:30 p.m.; Alan Gassman will be speaking from 6:45 to 7:15.

Location: The Tampa Club, 101 E Kennedy Boulevard, 41st Floor, Tampa, FL

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com

***********************************************************

LIVE NEWPORT BEACH PRESENTATION:

Jerry Hesch will present THE MATHEMATICS OF ESTATE PLANNING at the Society of Trust and Estate Practitioners 4th Annual Institute on Tax, Estate Planning, and the Economy. This conference is a collaboration between STEP Orange County and the University of California, Los Angeles, School of Law.

Professor Hesch’s presentation will make use of the materials that Alan Gassman, Ken Crotty, and Chris Denicolo presented to the 40th Annual Notre Dame Tax & Estate Planning Institute on November 14, 2014.

Date: January 22 – 24, 2015

Location: California Marriott Hotel and Spa at Fashion Island, Newport Beach, CA

Additional Information: For more information, please email agassman@gassmanpa.com or visit http://www.step.org/4th-annual-institute-tax-estate-planning-and-economy.

**************************************************************

FREE LIVE WEBINAR SERIES ON LIFE INSURANCE FOR TAX ADVISORS:

Alan Gassman and Barry Flagg, CPF, CLU, ChFC, GFS, of Veralytic will present a 30-minute webinar on HOW TO READ LIFE INSURANCE ILLUSTRATIONS in the first of a series of webinars intended to help tax lawyers and CPAs understand how life insurance and life insurance structuring works from a technical and mechanical standpoint.

Bring your wrench and screwdriver as we look under the hood to see how we can do our clients some good!

Date: January 26, 2015 | 5:00 p.m.

Location: Online webinar

Please note the below announcements for subsequent installments of this series:

February 18, 2015 – Criticism of Hybrid Index Life Insurance Products – What the Heck are These, and Why are They Becoming So Popular?

March 4, 2015 – Premium Financing in 15 Minutes

March 17, 2015 – Split-Dollar in 15 Minutes

March 31, 2015 – Comparing the Financial Strength and Risks Associated with Different Life Insurance Carriers

Gassman, Crotty & Denicolo, P.A., and The Thursday Report receive no direct or indirect compensation from any investment advisors and have no financial relationship with Barry Flagg or Veralytic. We thank Barry for putting together what we are sure will be an informative and objective program!

Additional Information: To register for the January 26th webinar, please click here or email Alan Gassman at agassman@gassmanpa.com for more information.

***********************************************

LIVE WEBINAR:

Alan Gassman and Barry Flagg, CPF, CLU, ChFC, GFS, of Veralytic will present a 15-minute webinar on CRITICISM OF HYBRID INDEX LIFE INSURANCE PRODUCTS – WHAT THE HECK ARE THESE AND WHY ARE THEY BECOMING SO POPULAR?

Date: February 18, 2015 | 5:00 p.m.

Location: Online webinar

Additional Information: To register, please click here or email Alan Gassman at agassman@gassmanpa.com for more information.

*******************************************************

LIVE FREE ETHICS CREDIT WEBINAR:

Alan Gassman and Dr. Srikumar Rao will present a free 50-minute webinar on HOW TO HANDLE STRESSFUL MATTERS IN AN ETHICAL WAY.

This webinar will qualify for 1 hour of CLE Ethics Credit and is classified as Advanced. See Professor Rao’s Ted Talk YouTube video, and you will understand how important this webinar might be to accelerating your law practice and enhancing your enjoyment of the practice as well. You can sign up for this free webinar by clicking here.

Dr. Srikumar Rao is the creator of the original Creativity and Personal Mastery (CPM) course that has helped thousands of executives and entrepreneurs achieve quantum leaps in effectiveness. He earned a Ph.D. in Marketing from Columbia University and has taught the course at Columbia University, Northwestern University, University of California at Berkeley, and the London School of Business. He is the author of Happiness at Work and Are You Ready to Succeed? which can be reviewed by clicking here. Are You Ready to Succeed? has been published in over 60 languages!

Date: February 19, 2015 | 12:30 p.m.

Location: Online webinar

Additional Information: Please email Alan Gassman at agassman@gassmanpa.com for more information.

*******************************************************

LIVE AVE MARIA SCHOOL OF LAW PROFESSIONAL ACCELERATION WORKSHOP

Alan Gassman will present a full day workshop for third year law students, alumni and professionals at Ave Maria School of Law. This program is designed for individuals who wish to enhance their practice and personal lives.

Date: February 21, 2015 | 8:30am – 5pm

Location: Ave Maria School of Law, 1025 Commons Cir, Naples, FL 34119

Additional Information: To see the official program for this workshop, please click here.

To register for this program please email agassman@gassmanpa.com.

*******************************************

LIVE WEBINAR:

Alan Gassman and Barry Flagg, CPF, CLU, ChFC, GFS, of Veralytic will present a 15-minute webinar on PREMIUM FINANCING IN 15 MINUTES.

Date: March 4, 2015 | 5:00 p.m.

Location: Online webinar

Additional Information: To register, please click here or email Alan Gassman at agassman@gassmanpa.com for more information.

*******************************************************

LIVE ORLANDO PRESENTATION:

THE ADVANCED HEALTH LAW TOPICS AND CERTIFICATION REVIEW 2015

Alan Gassman will speak at The Advanced Health Law Topics and Certification Review 2015 on HEALTHCARE TAX ISSUES.

To see the complete schedule for this program, please click here.

Date: March 6 – 7, 2015 ǀ Alan Gassman will speak on March 6 at 11:00 AM

Location: Hyatt Regency Orlando International Airport, 9300 Jeff Fuqua Blvd., Orlando, FL 32827

Additional Information: For more information, please email agassman@gassmanpa.com.

***********************************************

LIVE WEBINAR:

Alan Gassman and Barry Flagg, CPF, CLU, ChFC, GFS, of Veralytic will present a 15-minute webinar on SPLIT-DOLLAR IN 15 MINUTES.

Date: March 17, 2015 | 5:00 p.m.

Location: Online webinar

Additional Information: To register, please click here or email Alan Gassman at agassman@gassmanpa.com for more information.

*******************************************************

LIVE WEBINAR:

Alan Gassman and Barry Flagg, CPF, CLU, ChFC, GFS, of Veralytic will present a 30-minute webinar on COMPARING THE FINANCIAL STRENGTH AND RISKS ASSOCIATED WITH DIFFERENT LIFE INSURANCE CARRIERS.

Date: March 31, 2015 | 5:00 p.m.

Location: Online webinar

Additional Information: To register, please click here or email Alan Gassman at agassman@gassmanpa.com for more information.

*******************************************************

LIVE NAPLES PRESENTATION:

2nd ANNUAL AVE MARIA SCHOOL OF LAW ESTATE PLANNING CONFERENCE

Date: Friday, May 1, 2015

Location: Ave Maria School of Law, 1025 Commons Circle, Naples, Florida

Additional Information: Alan Gassman, Jerry Hesch, and Richard Oshins will present The Mathematics of Estate Planning. If you liked Donald Duck in Mathematics Land, you will love The Mathematics of Estate Planning. This will not be a Mickey Mouse presentation.

Other speakers include Richard Oshins on 11 Outstanding Planning Ideas, Jonathan Gopman on Asset Protection, Bill Snyder, Elizabeth Morgan, Greg Holtz, and others.

Please let us know any questions, comments, or suggestions you might have for this amazing conference, which features dual session selection opportunities in one of the most beautiful conference facilities that we have ever seen.

And don’t forget to have a great weekend in Naples with your significant other or anyone who your significant other doesn’t know! Domino’s Pizza is extra.

******************************************************

LIVE MIAMI PRESENTATION:

FLORIDA BAR WEALTH PRESERVATION PROGRAM

Denis Kleinfeld and Alan Gassman have released the schedule and topics for FUNDAMENTALS OF ASSET PROTECTION, AND ADVANCED STRATEGIES. This seminar will be presented on May 7th and May 8th, 2015, and is sponsored by the Tax Section of the Florida Bar. Attendees can select one day or the other, or to attend both days.

Day One will be for fundamentals and will be an excellent review or an introduction to the basic rules and practice aspects of creditor protection planning for both new and experienced practitioners.

Day Two will be an advanced treatment of creditor protection and associated planning, which will be of great use to both new and experienced practitioners.

Date: May 7 – 8, 2015

Location: Hyatt Regency Miami, 400 SE 2nd Avenue, Miami, FL 33131

Additional Information: To pre-register for this conference, please click here. For more information, please email Alan Gassman at agassman@gassmanpa.com.

***********************************************************

LIVE FLORIDA INSTITUTE OF CPAs (FICPA) WEBINAR

Alan Gassman, Ken Crotty, and Chris Denicolo will present a webinar on A PRACTICAL TRUST PLANNING CHECKLIST AND PRACTITIONER COMPLIANCE GUIDE FOR FLORIDA CPAs for the Florida Institute of CPAs.

Review a practical planning checklist and practitioner tax compliance guide to facilitate implementing a comprehensive overview of practical planning matters and tax compliance issues in your practice. This presentation will cover over 20 common errors and missed planning opportunities that accountants need to understand and counsel their clients on.

This course is designed for practitioners who wish to assure that trust planning structures and compliance are both aligned with client objectives and that common catastrophic errors and misconceptions can be corrected.

Past attendees have indicated that this is an interesting and practical presentation that offers a great deal of practical information for both compliance and planning functions, based upon an easy to follow checklist approach. Includes valuable materials.

Date: May 21, 2015 | 10:00 a.m.

Location: Online webinar

Additional Information: For more information, please contact Alan Gassman at agassman@gassmanpa.com or Thelma Givens at givenst@ficpa.org. To register, please click here.

******************************************

LIVE SARASOTA PRESENTATION:

2015 MOTE VASCULAR SURGERY FELLOWS – FACTS OF LIFE TALK SEMINAR FOR FIRST YEAR SURGEONS

Alan Gassman will be speaking on the topic of ESTATE, MEDICAL PRACTICE, RETIREMENT, TAX, INSURANCE, AND BUY/SELL PLANNING – THE EARLIER YOU START THE SOONER YOU WILL BE SECURE

Date: Friday, October 23rd and Saturday, October 24th, 2015

Location: To Be Determined

Additional Information: Please contact Alan Gassman at agassman@gassmanpa.com for more information.

NOTABLE SEMINARS BY OTHERS

(These conferences are so good that we were not invited to speak!)

LIVE CLEARWATER PRESENTATION:

RUTH ECKERD HALL PLANNED GIVING ADVISORY COUNCIL MEETING

Ruth Eckerd Hall’s next Planned Giving Council Meeting will be a spectacular two-part event, featuring an educational presentation at 4:30 p.m. and a networking session at 5:30 p.m.

“Improve with Improv: Using Humor and Immediate Responses to Enhance Client, Professional, and Social Interaction” will be led by Jack Halloway, a well-known improvisational coach and actor. This workshop will cover the basic and effective methods of improvisation in order to increase participants’ ability to think quickly, listen closely, and feel more comfortable responding to situations.

The presentation will be followed by a social networking and information session led by Ruth Eckerd Hall’s President and CEO Zev Buffman.

Call Ruth Eckerd Hall, learn improvisation, get an hour of credit, a glass of wine, and a great time!

Date: Tuesday, January 20, 2015 ǀ 4:30 p.m.

Location: Ruth Eckerd Hall’s Margarete Heye Great Room

Additional Information: For more information, or to RSVP, please contact Alan Gassman at agassman@gassmanpa.com or Suzanne Ruley at sruley@rutheckerdhall.net.

********************************************************

LIVE ST. PETERSBURG PRESENTATION:

ALL CHILDREN’S HOSPITAL FOUNDATION

Date: Thursday, February 12, 2015

Location: Live Event at the All Children’s Hospital St. Petersburg Campus; Webcasts in Tampa, Fort Myers, Belleair, New Port Richey, Lakeland, and Sarasota

Additional Information: Speakers include Richard A. Oshins, Melissa Langa, Stephanie Loomis-Price, Steve R. Akers, William R. Lane, and Abigail E. O’Connor. For a full list of speakers and presentation descriptions, please click here. For a complete seminar schedule, please click here.

Please contact Lydia Bennett Bailey at Lydia.Bailey@allkids.org for more information.

********************************************************

LIVE PRESENTATION:

2015 FLORIDA TAX INSTITUTE

Date: Wednesday through Friday, April 22 – 24, 2015

Location: Grand Hyatt Tampa Bay, 2900 Bayport Drive, Tampa, FL 33607

Additional Information: Please contact Bruce Bokor at bruceb@jpfirm.com for more information.

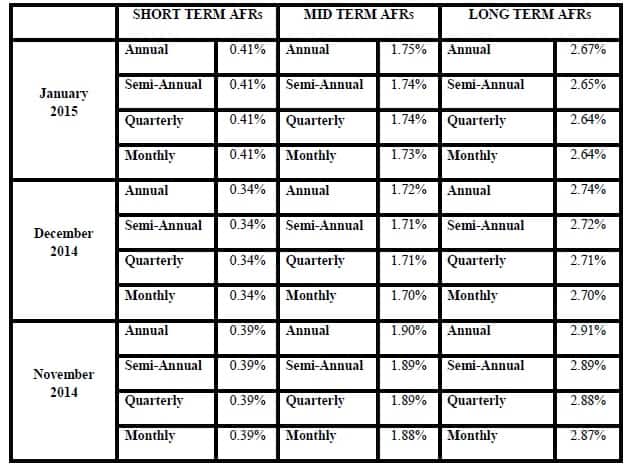

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.

The 7520 rate for January is 2.2% and for December was 2.0%.