The Thursday Report – 4.23.2015 – UF Tax Institute Special Edition

2nd Annual UF Tax Conference Information

Donate to the Stephen A. Lind Eminent Scholar Chair

Will the Real Life Expectancy Table Please Stand Up?

Not Every Home Will Grow at the “Average Rate” by Frank Catlett and Alan Gassman

Planning for Ownership and Inheritance of Pension and IRA Accounts and Benefits – The Charts You’ve Always Wanted, All in One Place

A Word from Scott Barnett

Richard Connolly’s World – The Surviving Spouse Estate Tax Trap

Seminar Spotlight – The 2nd Annual Ave Maria School of Law Estate Planning Conference

Florida Matters Radio Show to Re-Air Alan Gassman’s Talk on Same-Sex Marriage, Sunday, April 26 at 7:30 am on WUSF 89.7 FM

Humor! (or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Stephanie at stephanie@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

2nd Annual UF Tax Conference Information

Alan Gassman and Dennis Calfee review the t-shirts that are being given to Lind Chair qualified donors.

Alan Gassman, UF Tax student Maria Yole, and Mentor Mike Little

at the 2nd Annual UF Tax Conference

Alan Gassman, UF Tax Conference student Rene Vezina, and Mentor Andrew Comiter

at the 2nd Annual UF Tax Conference

Gassman, Crotty & Denicolo, P.A. is proud to be a contributing sponsor for the 2nd Annual University of Florida Tax Institute. Please visit our booth in the Exhibit Hall to meet Alan’s assistant, Maribeth, and sign up for one of the following opportunities:

- Meet Professor Calfee to talk about making a donation to the Lind Chair to get a free t-shirt.

- Sign up to attend a Saturday summer workshop with Professor Calfee, Alan Gassman and a number of tax students to discuss much of what it takes to be a successful professional. ($150 donation to the law school for each non-student attendee – scholarships available for recent alumni.)

- 80% of the proceeds from the sales of our books will go to the University of Florida Tax Program, and earmarked especially to buy beer for the professors who gave Alan a B or better while he was there in any course.

- Sign up to provide a 30 minute mentorship phone call or meeting with a University of Florida Tax law student at a time of your convenience. They have a lot of questions and this is a very scary place in their lives – you can help them make some big decisions and let them see that our profession is a friendly universe. Thank you to everyone who donated 30 minutes last night, under the influence of alcohol, each of which had a nice candid conversation with a young up-and-coming tax lawyer.

- Receive a special edition collectors t-shirt or gator ring toss toy for making a $200 or more pledge this week to the Lind Chair, or the same items signed by Professor Calfee for a $400 or more pledge.

Donate to the Stephen A. Lind Eminent Scholar Chair

by Professor Dennis Calfee

The Stephen A. Lind Eminent Scholar Chair in Federal Income Taxation is part of a group solicitation project to raise an endowed fund of $1.5 million for the Graduate Tax Program at the Levin College of Law. This Chair honors Professor Stephen Lind, who taught tax courses at the College from 1970 to 1998 and was one of the founding faculty members of the Graduate Tax Program.

The income from the endowed fund will be used to attract an Eminent Scholar in Taxation who is not a member of the College faculty at the time an offer is extended to occupy this chair. This Eminent Scholar will replace faculty members who have taught in the graduate tax program for many years. This Chair ideally will be occupied by someone who mirrors Steve both professionally and personally.

Contributions to this project qualify for a deduction under Section 170. Pledges can be over a five-year period or payable in any year in the five-year period.

Thank you, in advance, for your assistance with this project to honor Steve. He has touched and influenced so very many in a very positive way over his academic tenure. If you have any questions, please contact Professor Dennis Calfee at (352) 273-0911.

Currently, the Stephen A. Lind Eminent Scholar Chair, Fund number F019521, held at the University of Florida Foundation, has nearly $400,000 in contributions and pledges. We are proud to be donors to this chair and the Calfee chair

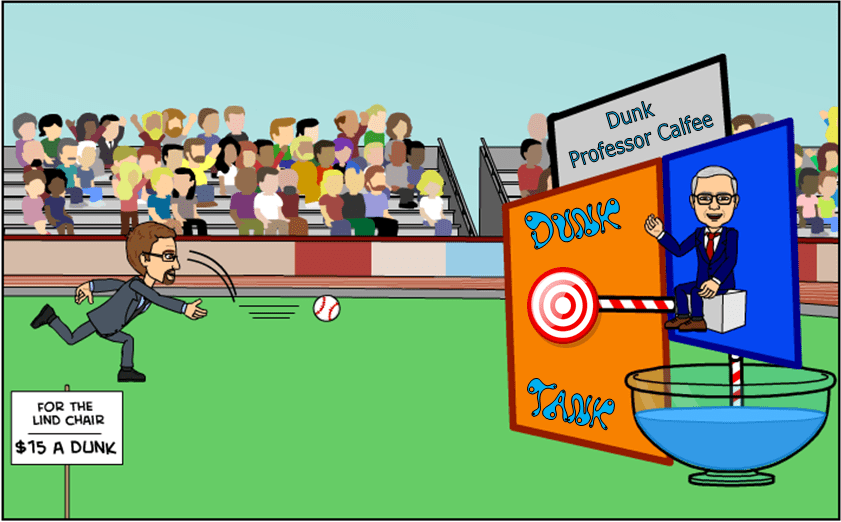

We are also pleased to announce that at the Florida Tax Institute, Professor Dennis Calfee will sit at the dunking booth during the Ethics portion of the Conference. Those who discreetly duck out and donate $15 towards the Stephen A. Lind Chair will get the chance to dunk Professor Calfee!

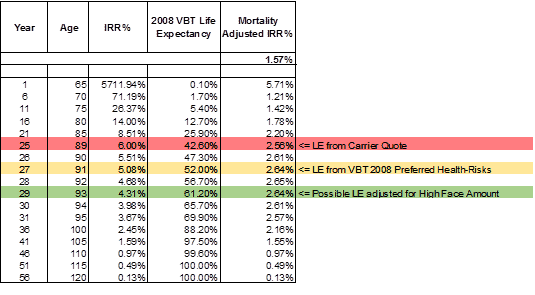

Will the Real Life Expectancy Table Please Stand Up?

by Alan Gassman, Brandon Ketron and Barry Flagg

The 1950s and 1960s television contest show “To Tell the Truth,” featured a panel of four celebrities whose object was to correctly identify a described contestant who had an unusual occupation or experience. The contestant was sworn to tell the truth, but was accompanied by two imposters who were free to answer the questions of the panel anyway they pleased. After the celebrity panel voted on who they thought was the real contestant, host Bud Collyer would ask “Will the real [person’s name] please stand up?”

When clients buy life insurance someone has to explain that the rate of return will be based upon how long the client will live, hence the question will the real life expectancy table please stand up?

For example, a 65 year old non-smoker female has an 89 year life expectancy according to one of the biggest life insurance carriers (and probably several of them).

If she is to pay (two thirds of $258,000) a year for her life to receive a $10,000,000 death benefit, what is the probable rate of return?

But, according to the Society of Actuaries 2008 Valuation Basic Table, life expectancy for a 65 year old female who meets non-smoker Preferred health-risk underwriting criteria is age 91, as opposed to the 89 years forecasted by the life insurance carrier.

Which table should we believe?

The two year difference has a big impact – the rate of return calculation comes to 5.51%, as opposed to the 6.53% forecasted by the carrier.

Assuming that the Society of Actuaries 2008 Valuation Basic Table described above is accurate, would the average affluent American who can afford a $172,000 a year premium be more or less likely to live to his or her life expectancy?

One would think that this person would have better medical care, better education, and less stress, at least from a financial standpoint, than the average American.

The Society of Actuaries sponsored the High Face Amount Mortality Study published in April 2012 that compared policies with a face amounts greater than $1,000,000 to those with smaller face amounts concluded by study that individuals were more likely to live if their lives were insured by $1,000,000 or more by an expected mortality ratio of 82% by face amount and 84% by policy count. In laymen’s terms, this means that the life expectancy of an individual whose life was insured by $1,000,000 or more, should be expected to have a longer life expectancy. Assuming that the insured’s life expectancy is increased to age 93, the rate of return drops to 4.68%, which is much lower than the original 6.53% forecast.

That said, the individual’s life expectancy may not be 93, but if life expectancy is to be used as a measure for the rate of return that is reasonable to expect, then the age 89 life expectancy indicated by the carrier appears incorrect. The life expectancy indicated by the 2008 VBT for Preferred health-risks is age 91, and the High Face Amount Mortality Study published by the Society of Actuaries indicates that the LE for high face amount policies/high net worth insured is older than 91. As such, the rate of return at life expectancy is likely less than 5.0% and potentially less than 4.0%. In addition because the rate of return is very sensitive to the accuracy of the life expectancy, and because life expectancy is an inherently imprecise variable (i.e. no more accurate than flipping a coin), the range of returns that are reasonable to expect are quite volatile.

The chart below shows the rate of return expected on death, highlighting the carrier’s projected life expectancy, the 2008 Valuation Basic Table’s life expectancy, and the possible increased life expectancy for an individual with a high face policy

The rate of return at selected ages is as follows:

Other Considerations

Many of the large carriers take their guarantees out to age 121, but the life insurance carrier estimates that this person only has a 1.24% chance of living to age 105.

One carrier in the situation above would be willing to reduce the premiums on the life insurance policy by $3,652 (2.1%) if the death benefit guarantee is only good until age 105.

One option would be to decrease the guarantee to age 105 and invest the difference in the premiums. For example of the $3,652 difference were invested at a 4% rate of return, the client will have accumulated an additional $466,956 by age 105. If the difference were invested at an 8% rate of return, the client will have an additional $1,025,599 by age 105.

Assuming that the client would live until age 106 (and there is a 0.97% chance of this according to the Actuarial Society 2008 Valuation Basic Tables) $10,000,000 will be lost, but that is 40 years from now, and by then there may be no estate tax, and if inflation averages 3% per year from now until 40 years from now the value of $10,000,000 will only be equal to $3,065,584 of buying power in today’s dollars, and the value of this person’s $100,000,000 investment portfolio will be expected to be approximately $461,630,000 if it grows at 4% per year (after taxes) for 40 years.

By the same token if the $172,000 is invested at 4% (which may be the average long term bond rate of return in the United States for the next 40 years) then $ 16,998,164 will have been accumulated after taxes.

How is a fiduciary to decide whether to buy this policy under a trust established by the client’s husband before he died?

Do you pay the extra $172,000 per year as insurance in case the medical industry has the revolution we all hope for (I’m sorry sir – your pancreas is not working properly but we can grow a new one in a pig and transplant it for you in the next 24 months).

Not Every Home Will Grow at the “Average Rate”

by Frank Catlett and Alan Gassman

Frank A. Catlett is a State-Certified General Real Estate Appraiser (FL), General Real Estate Appraiser (NC), and Certified General Real Property Appraiser (GA) with over 37 years of experience. Mr. Catlett is President of Trigg, Catlett & Associates, located in Tampa, Florida, which provides appraisal and brokerage services to not only the Tampa Bay, but most parts of Florida as well as North Carolina.

A great many senior Americans borrow money on “Reverse Mortgages” based in part on being told that their homes will go up in value with “national or regional averages,” which is often not the case.

For many of these homeowners, the better decision would be to downsize and not try to hold onto more house than they can afford. The decision to stay in a house that is too large causes the loss of investment resources in return and increased expenses. One national study has indicated that the cost of maintaining a home is based upon 3.53% of its value. Having a $200,000 home, when only a $100,000 home is needed, may therefore cost the senior citizen not only the investment return on $100,000, but also an additional 3.53% or more per year in expenses for utilities, taxes, insurance, and maintenance.

The reverse mortgage industry has encouraged many seniors to stay in their “too large” homes, based in part upon showing them projections that will indicate a likelihood of a 4% per year increase in value.

In fact, a 2013 actuarial report prepared for the US Federal Housing Administration (FHA) has indicated that a “worst case scenario” bottom 25th percentile Monte Carlo simulation has predicted that home prices could go down by more than 20% between 2014 and 2018 and might not recover to 2018 levels until 2024.

While the “average home” in a given area can be expected to increase in value on average over a term of years, the retiree’s home will typically be expected to go up in value at a slower rate, if it does go up in value, for the following reasons:

1.) The home gets older every year. The age of a home is a factor in valuation and appreciation. If the average home in a given area is 28 years old now, and the average house will be 26 years old in 20 years, then a 48-year-old home 20 years from now will be worth less than a 26-year-old home will be and will not be expected to have kept up with the “average growth rate.”

2.) The above is corroborated by the fact that homes have a typical estimated life expectancy of 60 years, and thus, depreciate in value to some extent. An appropriate rate of depreciation might be 1.667% of the value of the home itself each year, separate and apart from the land, because typically, a 60 year life expectancy will apply (1/60 = 1.667%). On the other hand, should this be 3.333% per year (2 x 1.667%) if the home is 30 years old to begin with?

If a typical house is worth 77.5% of the combined value of the house and land together, and the 77.5% house portion is going up by 3.5% statistically, not counting age, but then depreciating at 1.667% a year, then 22.5% of the total value (the land portion) is going up by 3.5% annually, and 22.5% of the value (the home portion) is going up by the excess of 3.5% over 1.66%, which is 1.89% per year.

Therefore, the average growth rate for a house might only be 2.2433% ((22.5% x 3.5%) + (77.5% x 1.89%)), on average.

3.) Senior citizens typically do not restore or renovate their homes, especially if they are of the average household that has the need to borrow on a reverse mortgage. A high percentage of the “average” homes in any given area have new kitchens, bathrooms, and other primary aspects installed or refurbished every 20 to 25 years. A senior citizen’s home will have a much lower restoration rate on average, which would bring the average growth rate in the above example well below the 2.2433% described above.

4.) Oftentimes, neighborhoods or surrounding areas start to turn for the worse, and mobile homeowners will move to more secure economic areas and neighborhoods where values normally increase at or above the average. Reverse mortgage borrowers are not able to do this, and are thus unable to move when value issues are likely to arise, and thus, have a less than average chance of being situated in a proper neighborhood for appreciation to be expected.

Based upon the above, we believe that it is a significant fallacy, and actually, a deceptive trade practice, for the reverse mortgage industry to tell homeowners that their homes can be expected to go up in value based upon statistical averages now being used.

Further, 4% as a normal projection rate seems ludicrous when the average home rate value increase in the last 20 years in the United States has been only 3.4%, before taking into account the issues described above.

Planning for Ownership and Inheritance of Pension and IRA Accounts and Benefits – The Charts You’ve Always Wanted, All in One Place

by Christopher J. Denicolo, Alan S. Gassman, and Brandon Ketron

The rules applicable to retirement plan and IRA distributions, contributions, rollovers, and otherwise can be difficult to understand and complex to implement. The applicable Internal Revenue Code Sections and Treasury Regulations are somewhat complicated and convoluted, and use many technical “terms of art.” This makes dealing with qualified plans cumbersome and difficult for laypersons and planners who are not experienced in this area.

We have attempted to simplify the applicable rules into a digestible format with concise explanations of the applicable rules. We have also prepared charts and explanations to illustrate the key concepts and mechanics of important definitions, rules, and planning strategies.

The Thursday Report proudly will provide a multi-part series to exhibit our materials and charts, and we hope that you enjoy this series as much as we did in putting it together.

To see previous editions of this presentation, please click below:

Chapter 1, Chapter 2, Chapter 3, Chapter 4, Chapter 5, Chapter 6, Chapter 7

This week, we are featuring all of the charts that were included in Chapters 1 through 7 of this presentation.

To see all of the charts included in the first seven chapters of our Planning for Ownership and Inheritance of Pension and IRA Accounts and Benefits presentation, please email agassman@gassmanpa.com.

A Word from Scott Barnett

Our friend Scott Barnett, J.D., LL.M., was kind enough to give us the following testimonial for our Planning for Ownership and Inheritance of Pension and IRA Accounts and Benefits series.

“The Gassman firm has, again, captured in one series an important aspect of tax and retirement planning. Qualified plans hold a mammoth part of the retirement assets needing planning. This new series on distributions is needed and well done.”

– Scott F. Barnett, J.D., LL.M. (Taxation)

scottfbarnett@scottfbarnettconsulting.com

Thanks very much, Scott, for your endorsement!

Richard Connolly’s World

The Surviving Spouse Estate Tax Trap

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares with us pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature some of Richard’s recommendations with a link to the articles.

This week, the article of interest is “The Surviving Spouse Estate Tax Trap” by Ashlea Ebeling. It was featured on Forbes.com on March 25, 2015.

Richard’s description is as follows:

The Internal Revenue Service is poised to release permanent regulations on portability, a newish provision of the estate tax law, and the American Institute of CPAs is requesting that the IRS make the rules more family-friendly. The problem is if you don’t know what portability is and how to elect it, you could be hit with a surprise federal estate tax bill.

The AICPA is concerned about estates not being able to take advantage of portability because many executors – and some accountants and lawyers – are unaware that you have to file an estate tax return at the first spouse’s death to elect portability.

In a letter to the IRS, the AICPA is asking for two other common sense fixes to the portability regime. To elect portability, executors have to file an estate tax return (Form 706 runs 31 pages, and the instructions are 53 pages). Instead, the AICPA says the IRS should provide a short form 706-EZ (like the 1040-EZ for income taxes) to make the portability election.

The other fix would be to allow a surviving spouse to file for portability. Now only the executor of a decedent’s estate can make the election. But it’s the surviving spouse – who may not be the executor – who has a vested interest in filing an estate tax return to elect portability – and save taxes at the second death.

Please click here to read this article in its entirety.

Seminar Spotlight

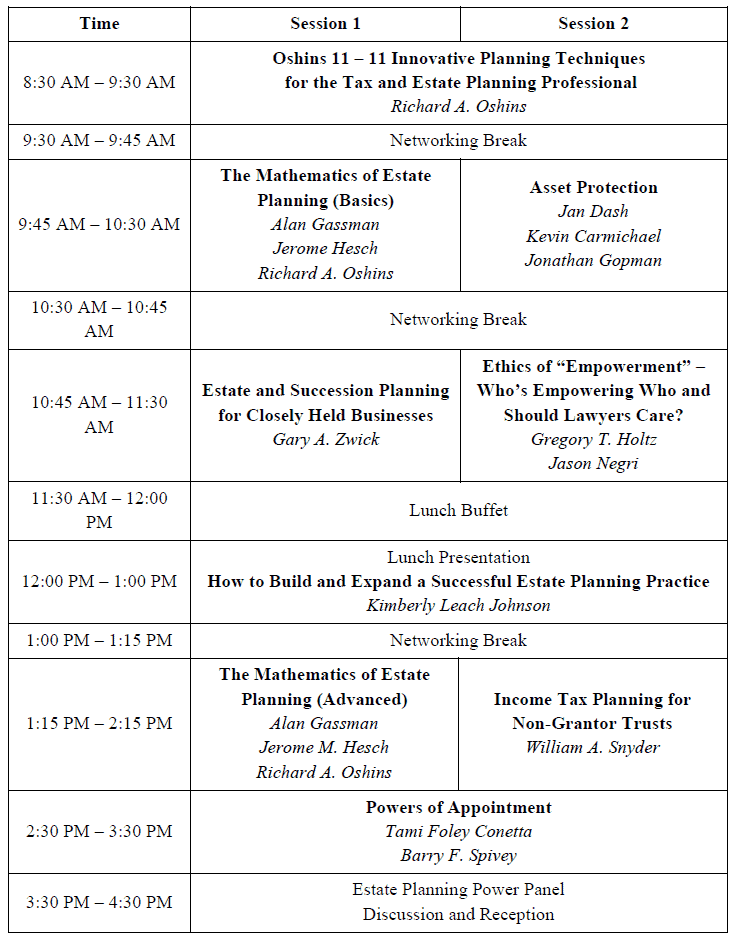

The 2nd Annual Ave Maria School of Law Estate Planning Conference

The 2nd Annual Ave Maria School of Law Estate Planning Conference will take place at the Ave Maria School of Law in Naples, Florida on May 1, 2015.

This conference is designed for estate planners, including attorneys, trust officers, accountants, insurance advisors, and wealth management professionals. The one-day program will include lectures and panel discussions designed to examine current developments in estate planning and to strengthen the practitioner’s knowledge and application of estate planning techniques.

The Ave Maria School of Law Estate Planning Conference qualifies for 9.5 General CLE Credits, 1.0 Ethics CLE credits, 7.0 Elder Law Certification Credits, 7.0 Wills, Trusts & Estates Certification Credits, and 6.25 CTFA Credits. Don’t miss this exciting opportunity!

The schedule for the event is as follows:

To register for this great event, please click here.

For more information, please contact Jean Takacs at jtakacs@avemarialaw.edu or by phone at (239) 687-5405. You may also contact Alan Gassman at agassman@gassmanpa.com.

Florida Matters Radio Show to Re-Air Alan Gassman’s Talk on Same-Sex Marriage, Sunday, April 26 at 7:30 am on WUSF 89.7 FM

The U.S. Supreme Court will be holding oral arguments this week on several same-sex marriage cases. As such, WUSF will be re-airing Alan Gassman’s radio interview with Florida Matters on Sunday, April 26, 2015 at 7:30 a.m. WUSF is 89.7 FM. The 4 minute summary version of Alan’s talk can be heard by clicking here and the link to listen to the interview with Alan and Michael Reedy can be heard on Sunday by clicking here. Tune in and let us know any questions or comments you may have!

Humor! (or Lack Thereof!)

Please enjoy the latest from our comedy contributor, Ron Ross!

IN THE NEWS:

Scientists in Cerne Abbas have used the Large Hadron Super-Collider to smash together a proton and an electron to recreate conditions at the time of the Big Bang – Attorneys claiming to represent the respective particles arrived and immediately demanded compensatory damages for their clients.

******************************************************************************

An iambic pentameter poem by Ron Ross:

Iambic pentameter is a commonly used type of metrical line in traditional English poetry and verse drama. The term describes the rhythm that the words establish, which is measured in small groups of syllables called “feet”.

In Xanadu did Kublai Khan a stately pleasure dome decree

With a treasure room and a mortgage fixed at percentage five point three

Then the vicious Mongol Horde rode in and the Khan’s palace was sacked

The treasure room was looted and the dome was slightly cracked

Now cash poor, Kublai tried to modify his rate

But the bankers, being bankers, refused to negotiate

So Kublai sent a friend to a friend in the Mongol Horde

Saying, “Why settle for less, don’t you know where the real treasure is stored?”

The Mongols robbed the bank and burned every mortgage and lien

And spent the night, finding they enjoyed being someplace clean

They used to live in the saddle to steal what others own

Now they take your money the legal way, at “Mongol Horde Savings and Loan”

******************************************************************************

THE STAGES OF GRIEF FOR A LAWYER WHO HAS JUST LOST A CASE:

DENIAL of a motion to set aside the judgment.

ANGER at the person who was late bringing the coffee, which must be the reason the case was lost.

BARGAINING with the opposing attorney to go “double or nothing” on the next case.

ACCEPTANCE of a job offer to argue in mock court on behalf of the witch that Hansel and Gretel threw in the oven.

Upcoming Seminars and Webinars

LIVE BLOOMBERG BNA WEBINAR:

Professor Jerome Hesch, Kenneth Crotty, and Christopher Denicolo will present a 90-minute webinar for Bloomberg BNA Tax & Accounting on MATHEMATHICSLAND FOR ESTATE PLANNERS.

This webinar includes over 30 interactive spreadsheets and explanatory tools that you need to know how to use to best serve your clients!

Date: Monday, April 27, 2015 | 2:00 PM

Location: Online webinar

Additional Information: To register for this webinar, please email Alan Gassman at agassman@gassmanpa.com.

***********************************************************

LIVE OLDSMAR PRESENTATION:

FICPA SUNCOAST SCRAMBLE GOLF TOURNAMENT

Kenneth J. Crotty and Christopher J. Denicolo will speak at the FICPA Suncoast Scramble Golf Tournament on the topic of MATHEMATICS FOR ESTATE PLANNERS INCLUDING 10 ESTATE PLANNING STRATEGIES NOT TO MISS.

Date: Friday, May 1, 2015 | CPE Presentations from 9:00 AM – 11:30 AM

Location: East Lake Woodlands Country Club | 1055 E Lake Woodlands Parkway, Oldsmar, FL 34677

Additional Information: For more information about registration, sponsorship, or this event, please click here or click here to download the Tournament brochure.

***********************************************************

LIVE NAPLES PRESENTATION:

2nd ANNUAL AVE MARIA SCHOOL OF LAW ESTATE PLANNING CONFERENCE

Alan Gassman, Jerry Hesch, and Richard Oshins will present THE MATHEMATICS OF ESTATE PLANNING. If you liked Donald Duck in Mathematics Land, you will love The Mathematics of Estate Planning. This will not be a Mickey Mouse presentation.

Other speakers include Richard Oshins on 11 Outstanding Planning Ideas, Jonathan Gopman on Asset Protection, Bill Snyder, Elizabeth Morgan, Greg Holtz, and others.

Please let us know any questions, comments, or suggestions you might have for this amazing conference, which features dual session selection opportunities in one of the most beautiful conference facilities that we have ever seen.

Date: Friday, May 1, 2015

Location: Ave Maria School of Law | 1025 Commons Circle, Naples, Florida

Additional Information: For more information, please visit http://estateplanning.avemarialaw.edu/ or email Alan Gassman at agassman@gassmanpa.com.

******************************************************

LIVE MIAMI PRESENTATION:

FLORIDA BAR WEALTH PRESERVATION PROGRAM

Denis Kleinfeld and Alan Gassman have released the schedule and topics for FUNDAMENTALS OF ASSET PROTECTION AND ADVANCED STRATEGIES. This seminar will be presented on May 7th and May 8th, 2015, and is sponsored by the Tax Section of the Florida Bar. Attendees can select one day or the other, or to attend both days.

Day One will be for fundamentals and will be an excellent review or an introduction to the basic rules and practice aspects of creditor protection planning for both new and experienced practitioners.

Day Two will be an advanced treatment of creditor protection and associated planning, which will be of great use to both new and experienced practitioners.

Date: May 7 – 8, 2015

Location: Hyatt Regency Miami | 400 SE 2nd Avenue, Miami, FL 33131

Additional Information: To register for this conference, please click here. For more information, please email Alan Gassman at agassman@gassmanpa.com.

***********************************************************

LIVE BLOOMBERG BNA WEBINAR:

Professor Jerome Hesch, Alan Gassman, and Barry Flagg will be presenting a 90-minute webinar for Bloomberg BNA Tax & Accounting on THE TAX ADVISORS GUIDE TO PERMANENT LIFE INSURANCE AND STRUCTURING TOOLS AND TECHNIQUES.

Date: Tuesday, May 12, 2015 | 2:00 PM

Location: Online webinar

Additional Information: To register for this webinar, please email Alan Gassman at agassman@gassmanpa.com.

******************************************************************

LIVE BRADENTON, FLORIDA PRESENTATION

Alan Gassman will speak at the Coastal Orthopedics Physician Education Seminar on the topics of CREDITOR PROTECTION AND THE 10 BIGGEST MISTAKES DOCTORS CAN MAKE: WHAT THEY DIDN’T TEACH YOU IN MEDICAL SCHOOL.

Coastal Orthopedics, Sports Medicine, and Pain Management is a comprehensive orthopedic practice which has been taking care of patients in Manatee and Sarasota Counties for 40 years. They have sub-specialized, fellowship-trained physicians as well as in-house diagnostics, therapy, and an outpatient surgery center to provide comprehensive, efficient orthopedic care.

Date: Tuesday, May 12, 2015 | Time TBA

Location: Coastal Orthopedics and Sports Medicine | 6015 Pointe West Boulevard, Bradenton, FL, 34209

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE STUART, FLORIDA PRESENTATION

Alan Gassman will be the featured “headline” speaker the Martin County Estate Planning Council Annual Tax and Estate Planning Seminar. He will be doing a three-hour talk on the topics of JESTs, MATHEMATICS FOR ESTATE PLANNERS, AND THE ESTATE PLANNER’S GUIDE TO PLANNING FOR IRA AND PENSION BENEFITS – YES, YOU CAN FINALLY UNDERSTAND THESE RULES!

Date: May 15, 2015 | 8:15 AM – 4:30 PM; Alan Gassman speaks from 9:00 AM to 12:00 PM

Location: Stuart Corinthian Yacht Club | 4725 SE Capstan Avenue, Stuart, FL 34997

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com or Lisa Clasen at lclasen@kslattorneys.com.

************************************************

LIVE WEBINAR:

Alan Gassman and noted trust and estate litigator, LL.M in estate planning, and blog master Juan Antunez, J.D., LL.M. will be presenting a free 30-minute webinar on ARBITRATING TRUST AND ESTATES DISPUTES.

Don’t miss Juan’s wonderful blog site entitled Florida Probate & Trust Litigation Blog, which can be accessed by clicking here, and the many vary useful articles thereon.

Date: Tuesday, May 19, 2015 | 12:30 PM

Location: Online webinar

Additional Information: To register for this webinar, please click here.

**********************************************************

LIVE FLORIDA INSTITUTE OF CPAs (FICPA) WEBINAR

Alan Gassman, Ken Crotty, and Chris Denicolo will present a webinar on A PRACTICAL TRUST PLANNING CHECKLIST AND PRACTITIONER COMPLIANCE GUIDE FOR FLORIDA CPAs for the Florida Institute of CPAs.

Review a practical planning checklist and practitioner tax compliance guide to facilitate implementing a comprehensive overview of practical planning matters and tax compliance issues in your practice. This presentation will cover over 20 common errors and missed planning opportunities that accountants need to understand and counsel their clients on.

This course is designed for practitioners who wish to assure that trust planning structures and compliance are both aligned with client objectives and that common catastrophic errors and misconceptions can be corrected.

Past attendees have indicated that this is an interesting and practical presentation that offers a great deal of practical information for both compliance and planning functions, based upon an easy to follow checklist approach. Includes valuable materials.

Date: May 21, 2015 | 10:00 AM

Location: Online webinar

Additional Information: For more information, please contact Alan Gassman at agassman@gassmanpa.com or Thelma Givens at givenst@ficpa.org. To register, please click here.

**************************************************

LIVE MIAMI LAKES WORKSHOP:

Alan Gassman will be speaking at the Miami Lakes Bar Association Luncheon on the topic of ACCELERATING YOUR LAW PRACTICE. This luncheon will qualify for 2 CLE credits.

Date: Thursday, May 21, 2015 | 11:45 am – 1:45 pm

Location: Italy Today | 6743 Main Street, Miami Lakes, FL 33014

Additional Information: For more information, please contact Alan Gassman at agassman@gassmanpa.com.

******************************************************

LIVE UNIVERSITY OF FLORIDA PROFESSIONAL ACCELERATION WORKSHOP:

Alan Gassman will present a five hour workshop on legal practice and making the most of your legal practice to Professor Dennis Calfee’s summer workshop class. Experienced professionals are also welcome to attend by making a $150 donation to the Lind Chair.

Date: To Be Determined

Location: University of Florida | 2500 SW 2nd AE, Gainsville, FL 32611

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com.

*********************************************************

LIVE WEBINAR:

Alice Rokahr, President, Trident Trust Company (South Dakota) Inc., and Alan S. Gassman will present a free, 30-minute webinar entitled WHAT IS SO SPECIAL ABOUT SOUTH DAKOTS – DOMESTIC ASSET PROTECTION TRUST LAW AND PRACTICES.

Date: June 9, 2015 | 12:30 pm

Location: Online webinar

Additional Information: For more information, please contact Alan Gassman at agassman@gassmanpa.com or click here to register for this webinar.

**********************************************

LIVE BLOOMBERG BNA WEBINAR:

Professor Jerome Hesch, Alan Gassman, Ed Morrow, Christopher Denicolo, and Brandon Ketron will be presenting a 90-minute webinar for Bloomberg BNA Tax & Accounting on ESTATE AND TRUST PLANNING WITH IRA AND QUALIFIED PLAN BENEFITS: AN UNDERSTANDABLE SYSTEM WITH CHARTS AND EASY-TO-UNDERSTAND MATERIALS.

This presentation will include a 300 page E-book for each attendee.

Date: Wednesday, June 10, 2015 | 2:00 PM

Location: Online webinar

Additional Information: To register for this webinar, please email Alan Gassman at agassman@gassmanpa.com.

*******************************************************

LIVE AVE MARIA SCHOOL OF LAW PROFESSIONAL ACCELERATION WORKSHOP

Alan Gassman will present a full day workshop for third year law students, alumni, and professionals at Ave Maria School of Law. This program is designed for individuals who wish to enhance their practice and personal lives.

Date: August 22, 2015 | 9:00 AM – 5:00 PM

Location: Thomas Moore Commons, Ave Maria School of Law, 1025 Commons Circle, Naples, FL 34119

Additional Information: To download the official invitation to this event, please click here. To RSVP and for more information, please contact Donna Heiser at dheiser@avemarialaw.edu or via phone at 239-687-5405 or Alan Gassman at agassman@gassmanpa.com or via phone at 727-442-1200.

****************************************************

LIVE FORT LAUDERDALE PRESENTATION:

Ken Crotty will be presenting a 1-hour talk on PLANNING FOR THE SALE OF A PROFESSIONAL PRACTICE – TAX, LIABILITY, NON-COMPETITION COVENANT, AND PRACTICAL PLANNING at the Florida Institute of CPAs Annual Accounting Show.

Date: September 18, 2015 | 3:30 PM – 4:20 PM

Location: Broward County Convention Center | 1950 Eisenhower Blvd, Fort Lauderdale, FL 33316

Additional Information: For additional information, please email Ken Crotty at ken@gassmanpa.com or CPE Conference Manager Diane K. Major at majord@ficpa.org.

*************************************************

LIVE SARASOTA PRESENTATION:

2015 MOTE VASCULAR SURGERY FELLOWS – FACTS OF LIFE TALK SEMINAR FOR FIRST YEAR SURGEONS

Alan Gassman will be speaking on the topic of ESTATE, MEDICAL PRACTICE, RETIREMENT, TAX, INSURANCE, AND BUY/SELL PLANNING – THE EARLIER YOU START, THE SOONER YOU WILL BE SECURE.

Date: Friday, October 23rd and Saturday, October 24th, 2015

Location: To Be Determined

Additional Information: Please contact Alan Gassman at agassman@gassmanpa.com for more information.

Notable Seminars by Others

(These conferences are so good that we were not invited to speak!)

LIVE PRESENTATION:

RUTH ECKERD HALL PLANNING GIVING COUNCIL MEETING

This exciting two-part event will feature an educational presentation and a networking session. Attorneys and CPAs may receive CLE and CPE credit for attending the educational presentation.

The educational presentation will be an entertaining, interactive workshop led by Jack Halloway, a well-known improvisational coach and actor. He is directing “The Complete Works of William Shakespeare (Abridged)” and will share some thoughts on how Shakespeare used law, lawyers, and money in his plays. Some improv will also be included.

Jack Halloway’s presentation will be followed by a social networking and info session. Enjoy some wine and time with fellow Planned Giving enthusiasts!

Everyone who brings a potential donor or new member to the Planning Giving Council will be entered into a raffle for 2 tickets to an upcoming show.

Date: April 21, 2015 | Educational Presentation begins at 4:30 PM | Networking sessions begins at 5:30 PM

Location: The New Murray Theatre at Ruth Eckerd Hall

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com. RSVPs may be sent to Maribeth Vongvenekeo at maribeth@gassmanpa.com, Suzanne Ruley at sruley@rutheckerdhall.net, or Kristy Philippe at kristy.philippe@ms.com.

******************************************************

LIVE PRESENTATION:

2015 UNIVERSITY OF FLORIDA TAX INSTITUTE

Date: Wednesday through Friday, April 22 – 24, 2015

Location: Grand Hyatt Tampa Bay | 2900 Bayport Drive, Tampa, FL 33607

Additional Information: Please visit http://www.floridataxinstitute.org/agenda.shtml for a complete schedule or contact Bruce Bokor at bruceb@jpfirm.com for more information.

******************************************************

LIVE ORLANDO PRESENTATION:

50TH ANNUAL HECKERLING INSTITUTE ON ESTATE PLANNING

Date: January 11 – January 15, 2016

Location: Hotel information to be announced

Additional Information: Information on the 50th Annual Heckerling Institute on Estate Planning will be available on August 1, 2015. To learn about past Heckerling programs, please visit http://www.law.miami.edu/heckerling/.

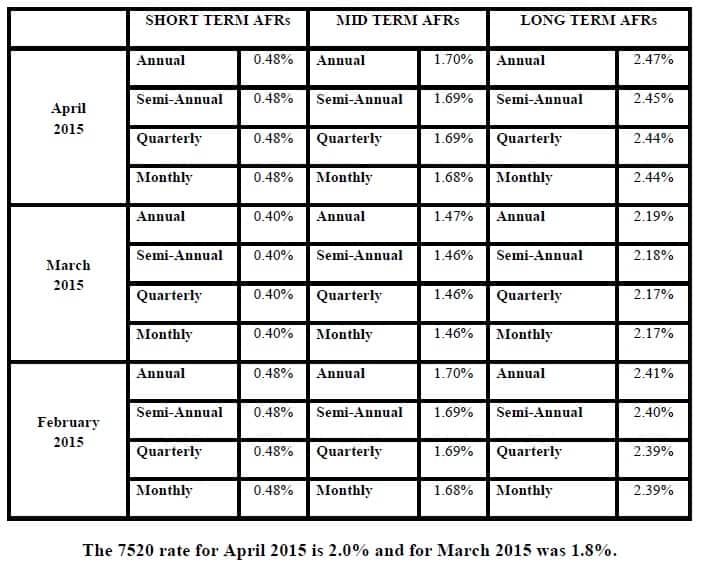

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.