The Thursday Report – 3.5.15 – Live Long and Thursday & More Warped Humor

* This issue’s date is displayed in Stardate format, in honor of Leonard Nimoy and the Star Trek franchise. To convert a Gregorian calendar date into a Stardate, please click here for a Stardate calculator.

Live Long and Prosper: Leonard Nimoy

Secretary of State Filings Now Slower than a Damaged Klingon Freighter on Impulse Battery Drive

Planning for Ownership and Inheritance of Pension and IRA Accounts and Benefits – A Thursday Report Series Designed to Decipher the Complexities Associated with the Taxation of Retirement Plans, Part I by Christopher J. Denicolo, Alan S. Gassman, and Brandon Ketron

Well-Respected Multi-National Trust Company Opens Office in South Dakota – Very Nice Informational Book Available at No Charge!

Richard Connolly’s World Double Header

Thoughtful Corner – Business Etiquette in Interacting with Clients and Colleagues

Humor! (or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Live Long and Prosper: Leonard Nimoy

by Stephanie Herndon and Alan Gassman

Those of us who grew up watching television in the late 1960s while entranced by the space program, the promise of a more ideal society, and the desire to travel in time and see new worlds and civilizations could’ve had no better vehicle, at least on Thursday nights, than Star Trek, and Mr. Spock was a big part of that.

Star Trek’s predecessor was the western show Wagon Train, where a somewhat emotional leader and a logical first mate riding shotgun on explorations to unknown lands made for a very successful formula. Star Trek was almost entitled “Wagon Train to the Stars” and was marketed as a western in outer space before its premiere in 1966.

Star Trek was creator and producer Gene Roddenberry’s science fiction twist for a Wagon Train equivalent, and, with science fiction, Roddenberry could go further in exploring a character so logical that he had to be an alien from another planet. This character was named Spock. He was half human, with shielded and locked up emotions, and half Vulcan, an extraterrestrial humanoid species from the planet with the same name, known for their ability to live logically and with tremendous mental and mathematical power. Spock exemplified these Vulcan characteristics, not to mention the ability to read minds and to pinch people’s shoulders and make them pass out.

Roddenberry intended each episode of Star Trek to tell two stories each week: one of suspenseful adventure and one of morality, like the stories contained in Jonathan Swift’s Gulliver’s Travels. Spock was in constant combat with his emotions, revealing an extremely ironic sense of humor. The character’s journey on the show illustrated an evolution from being extremely starchy and impersonal in the first few episodes to becoming likeable and eventually one of the most beloved, fan-favorite characters of all time.

Spock was portrayed by Leonard Nimoy, an accomplished and talented actor who became an international phenomena through Spock and Star Trek. Nimoy never had the chance to play the role of Colonel Sanders, but he continued to return to Spock and the Star Trek universe throughout his lengthy career.

Gene Roddenberry died in 1991. The following year, a portion of his ashes traveled to space on the space shuttle Columbia before returning to Earth after the crew completed Mission STS-52. Five years after that, a spacecraft owned and operated by Celestis, a company known for performing space burials, was launched into Earth’s orbit aboard a Pegasus rocket. The Celestis spacecraft contained a portion of Roddenberry’s ashes, as well as the ashes of Timothy Leary and 22 other people. This spacecraft disintegrated into the atmosphere in 2002. Roddenberry, Nimoy, and the entire Star Trek team have been credited with fueling public interest in space and space exploration programs.

The computer on the Starship Enterprise was more fun than Siri and proved to be 45 years ahead of its time. Quite likely, Apple computers, the monumental success of Steve Jobs, and Siri would not have happened if a generation of then-teenagers were not helped to see the incredible possibilities that Roddenberry and his team made not only evident but also seemingly probable.

So much of the science fiction portrayed in Star Trek has come true, and so much more will come true as technology continues to grow.

If you have never seen Star Trek, some of our favorite episodes include “The Trouble with Tribbles,” (Episode 44), written by David Gerrold and directed by Joseph Pevney and “The City on the Edge of Forever,” (Episode 28) written by Harlan Ellison and directed by Joseph Pevney. “The City on the Edge of Forever” also features guest star Joan Collins as Edith Keeler, who (spoiler alert!) makes out with Captain Kirk.

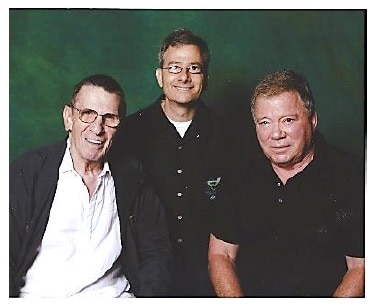

Leonard Nimoy and William Shatner (who played Captain Kirk on Star Trek) were very close friends. They, along with Gene Roddenberry, were highly interactive with each other and fans of the franchise.

Alan Gassman had a very deep discussion with Leonard Nimoy and William Shatner in Las Vegas in 2009 during the 1.7 seconds that he was given to have his picture taken with Nimoy and Shatner, each of whom asked him for his autograph and invited him to their after-the-signing party to discuss intergalactic trust law and the use of time travel to capture the time value of money and Kentucky Fried Chicken franchises in the Romulan Neutral Zone.

While waiting for approximately 45 minutes for his turn to be photographed with them ($200 per person at approximately 1 person a minute for 45 minutes – not a bad deal for them!) Alan noticed a close friendship between the two and that they appeared to have a lot of things they wanted to talk to each other about.

In any event, we can always salute the late 1960s, Gene Roddenberry, Leonard Nimoy, William Shatner, and others for giving us something else to watch besides Lost in Space, which aired the night before Star Trek each week and makes Star Trek look like the most advanced television show ever created by comparison. (CBS was originally offered Star Trek but passed it up in favor of Lost in Space. Star Trek then landed on NBC instead.)

Kudos to Roddenberry, NBC, and Paramount for a show and storylines that indirectly objected to the Vietnam War and encouraged interracial relationships and helping others. Star Trek showed that people from diverse backgrounds can work together to achieve phenomenal results and that the engineer (Mr. Spock) should always tell the Captain that things take a lot longer than they really take so that he can look like a hero.

Hats off to Leonard Nimoy for being an important part of the team that gave us a fantastic vision, great humor, and most importantly, great motivation for doing the right thing, respecting human rights, taking risks when appropriate, using intuition, and bucking the system in the right way and the right time.

Live long and prosper Leonard Nimoy! We will see you in the next nebula.

See our Humor section below for some of Leonard Nimoy’s best quotes as Mr. Spock. Don’t miss it!

Secretary of State Filings Now Slower than a Damaged Klingon Freighter on Impulse Battery Drive

Due to recent system updates, mass annual report filings, or both, we have noticed a delay in the filing of LLC Articles of Organization when filed through the Florida Department of State online filing system. While we have come to expect that LLC Articles of Organization submitted through the online filing system would result in a confirmation of filing within 24 hours, we recently have encountered a delay of 2-3 business days for some of our LLC filings.

Please also be aware that recent system upgrades seem to have added an extra “last step” screen that can be slightly confusing and may result in your corporate filing not being processed at all. After entering information on the LLC Articles of Organization and hitting “Continue,” you are taken to the Filing Information screen and asked to review the filing for accuracy. If the information entered is correct, you will click on “Continue” and are then taken to a screen that says, “Florida Limited Liability Company Online Filing Information,” where you will be provided with a Document Tracking Number and the charge amount for your filing.

Since this screen provides you with a Document Tracking Number, it is easy to assume that your filing is complete and nothing else is needed. Please note that from this screen, you will have to again click “Continue” to move to the payment screen (and receive a second Tracking Number.)

Our staff has erroneously assumed filing was complete after the first Document Tracking Number was provided. When the LLC was not filed in a timely manner, we contacted the State by phone to provide our Tracking Number and check the status. We were told they had no information regarding our document in their system. Apparently, no information is saved on the Department of State system until payment is processed. The initial Tracking Number you receive will not allow you to check the status of a filing unless you proceeded to the next screen, submitted payment, and received the second Tracking Number.

In situations where time if of the essence, we have found fax-filing with the Department of State (which requires that you have a Department of State account) is often the fastest way to generate a timely filing.

Planning for Ownership and Inheritance of Pension and IRA Accounts and Benefits – A Thursday Report Series Designed to Decipher the Complexities Associated with the Taxation of Retirement Plans

by Christopher J. Denicolo, Alan S. Gassman, and Brandon Ketron

The rules applicable to retirement plan and IRA distributions, contributions, rollovers, and otherwise can be difficult to understand and complex to implement. The applicable Internal Revenue Code Sections and Treasury Regulations are somewhat complicated and convoluted, and use many technical “terms of art.” This makes dealing with qualified plans cumbersome and difficult for laypersons and planners who are not experienced in this area.

We have attempted to simplify the applicable rules into a digestible format with concise explanations of the applicable rules. We have also prepared charts and explanations to illustrate the key concepts and mechanics of important definitions, rules, and planning strategies.

The Thursday Report proudly will provide a multi-part series to exhibit our materials and charts, and we hope that you enjoy this series as much as we did in putting it together.

IRA SERIES CHAPTER 1

There are many stages of IRA and pension distribution planning, and many different types of interactive knowledge needed. Nevertheless, a thumbnail sketch of the most important components of knowledge with reference to establishing and funding IRAs and making the best use of planning considerations follows:

I. Accumulation Stage

- IRA Contribution Rules for 2014 tax year

- Basic Contribution limit is the lesser of

- $5,500 (but $6,500 if over the age of 50)

- Taxable compensation for the year

- Reduced by the amount of Roth contributions, as described in C.2 below

- Other Limitations if covered by a qualified plan at work

- Contribution limit begins to be phased out at $96,000 of adjusted gross income, and is completely phased out at $116,000 of adjusted gross income for married filing jointly taxpayers.

- Phase out begins at $60,000 of adjusted gross income, and is completely phased out at $70,000 of adjusted gross income for single or head of household taxpayers.

- In order to deduct contributions for the 2014 tax year, contributions must be paid prior to the due date for the 2014 tax return (April 15th, 2015). Even if you have not yet made a contribution after year end, a contribution made prior to the filing of the tax return due date is eligible to be treated as made in the prior year.

- Basic Contribution limit is the lesser of

- Coverdell Education Savings Account (Education IRA) Contribution Rules – Grandmas and Grandpas should pay special attention to this. This allows tax-free growth and tax-free withdrawals to pay for permitted educational expenses.

- Contributions are limited to $2,000 per year per child. (Note –The limitation is on the total amount the child can receive per year, not on the amount contributed by each person. Therefore if multiple parties contribute to the Educational IRA the total contributions in the aggregate cannot exceed $2,000.)

- Balance must be disbursed on qualified education expenses prior to the beneficiary obtaining the age of 30 to avoid penalties and taxes.

- Only eligible if AGI of contributor is less than $110,000 ($220,000 if filing joint) (Planning Note – It is possible for the child to contribute to his or her own Educational IRA. If the contributor’s AGI is greater than the limitation, a gift of $2,000 can be made to the child, and the child contributes the money to the Educational IRA, assuming the Child’s AGI is below the limitation amount.

- Organizations such as corporations and trusts can also contribute, and there is no requirement for the organization’s income to be below a certain level.

- No contribution can be made after beneficiary reaches age 18, unless the beneficiary is a special needs beneficiary.

- Roth IRA Contribution Rules

- Basic Contribution limit is the lesser of

- $5,500 (but $6,500 if over the age of 50).

- Taxable compensation for the year

- Reduced by contributions to traditional IRAs – See A.1.c above

- Other Limitations

- Contribution limit begins to be phased out at:

- $188,000 for married filing jointly

- 127,000 for single, head of household

- If contributing to both Roth and Traditional IRA, contributions in the aggregate cannot exceed the $5,500 limitation ($6,500 if over age 50)

- Contribution limit begins to be phased out at:

- Basic Contribution limit is the lesser of

- Converting Traditional IRA into Roth IRA

- You can withdraw all or part of the assets from a traditional IRA and reinvest them WITHIN 60 DAYS into a Roth IRA.

- If you started taking substantially equal periodic payments from a traditional IRA, you can convert the amounts in the traditional IRA to a Roth IRA and then continue the periodic payments.

- You CANNOT convert amounts distributed in accordance with Required Minimum Distributions Rules into a Roth IRA

- Do not include in gross income any part of a distribution from a traditional IRA that is a return of basis, but the rest is subject to income tax upon conversion and does not always make good sense. See Leimberg Information Services Newsletter Archive #549 by Alan S. Gassman, Kenneth Crotty and Christopher Denicolo, entitled One Good Reason Not To Do A Roth IRA Conversion.

- Eligible Rollovers

- See IRS Chart in Chapter Two.

- How Many Rollovers Each Year?

- Internal Revenue Code Section 408(d)(3)(B) provides that there can be only one tax free rollover by an individual within a twelve month period.

- 2014 Tax Court Memorandum decision of Bobrow v. Commissioner confirmed this treatment by severely penalizing a taxpayer that attempted to roll over multiple IRAs in one calendar year.

- Creditor Protection of Owner

- Fla. Stat. Ann. § 222.21 provides that retirement plans are exempt from creditor claims as discussed in Chapter Three Section IV. Therefore, the U.S. Supreme Court decision of Clark v. Rameker [1], which found that the federal bankruptcy law will not protect IRAs for those residing in states that do not have exemption statutes for IRAs, will not apply to Floridians. Archive #251 by Christopher Denicolo, Alan S. Gassman and Brandon Ketron entitled Clark V. Rameker: Supreme Court Rules that Inherited IRAs Are Not Creditor-Exempt in Bankruptcy.

- The majority of other states treat retirement plans as creditor exempt but see 50 State plus D.C. Creditor Exemption Statutes for IRAs, Non‐ERISA 403(b) and Roth Variants provided by Ed Morrow in Appendix C that outlines the Creditor Protection Statutes for each State.

- The authors believe that a distribution received by an individual beneficiary of an inherited IRA/Plan or a rollover IRA/Plan will be considered to be exempt from creditor claims from normal general creditors under Florida Statute Section 222.21(2)(c), and may therefore be placed into an exempt asset (such as a variable annuity contract, a cash value life insurance policy, or a tenancy by the entireties account) without being considered a fraudulent transfer (the transfer of funds from one exempt class of asset directly to another exempt class of asset will generally not be considered to be subject to being set aside under the Florida Fraudulent Transfers Act), although a Florida Bar article authored by David Pratt and Lindsay A. Roshkind “Roth IRA Conversions as an Asset Protection Strategy: Does it Always Work?” Feb. 2011 Vol. 85, No.2 indicates that there is a possibility that distributions would not be considered to be exempt from creditor claims.

- QDRO Rules – transferring IRA and/or pension balances tax-free upon divorce.

- A Qualified Domestic Relations Order is a domestic relations order which creates or recognizes the existence of an alternate payee’s right to, or assigns to an alternate payee the right to, receive all or a portion of the benefits payable with respect to a participant under a qualified plan (i.e. employer sponsored).

- QDROs must contain the following information:

- The name and last known mailing address of the participant and each alternate payee.

- The name of each plan to which the order applies.

- The dollar amount or percentage (or the method of determining the amount or percentage) of the benefit to be paid to the alternate payee.

- The number of payments or time period to which the order applies.

- Recent Pronouncement on Canadian Registered Retirement Savings Plans (RRSPs) and Registered Retirement Income Funds (RRIFs)

- Taxpayers who hold these funds will now automatically qualify for tax deferral similar to US IRA and 401(k) funds.

- Previously Canadian taxpayers were required to file a Form 8891 in order to qualify for tax deferral. The IRS has now eliminated Form 8891, and taxpayers are no longer required to file this form for any year, past or present.

- Grandfather Rule – TEFRA 242(b) elections

- In 1982 TEFRA made significant changes to the Required Minimum Distribution Rules.

- If elected prior to January 1, 1984 242(b) allows Plan Participants to use the more liberal rules prior to TEFRA

- Significant Rules allowed pre TEFRA

- Required Minimum Distributions can be postponed past age 70 1/2 until retirement, regardless of whether the Plan Participant owns more than 5% of the company.

- Death Benefits are not subject to the 5 Year Rule, or the At Least as Rapidly Rule.

II. Access Before Age 59 ½

- Generally any amount withdrawn prior to the age 59 ½ is subject to an additional 10% excise tax

- Exceptions

- 60 Day Rule – Any money can be withdrawn temporarily, as long as the money is placed back into the account within 60 days of the withdrawal.

- The taxpayer has unreimbursed medical expenses that are more than 10% (or 7.5% if you or your spouse was born before January 2, 1949) of your adjusted gross income.

- The distributions are not more than the cost of taxpayer’s medical insurance due to a period of unemployment.

- Taxpayer is totally and permanently disabled.

- Taxpayer is the beneficiary of a deceased IRA owner. The surviving spouse who is named as a beneficiary of a deceased participant’s IRA/plan who has not reached age 59 ½, may withdraw funds from the plan without being subject to the 10% excise tax unless or until the IRA/plan has been rolled over to the surviving spouse’s own IRA. This would be a good reason to delay making a complete rollover before being sure that distributions from the IRA/plan for a spouse under age 59 ½ will not be needed. A disadvantage of the above is that the surviving spouse will not be able to change the disposition of the assets remaining under the deceased participant’s IRA/plan if the spouse dies without having completed a rollover into his or her own IRA/plan.

- Taxpayer is receiving distributions in the form of an annuity.

- The distributions are not more than the taxpayer’s qualified higher education expenses. [2]

- The taxpayer uses the distributions to buy, build, or rebuild a first home up to $10,000 for any of the following:

- The taxpayer

- The taxpayer’s spouse

- The taxpayer’s child or the taxpayer’s spouse’s child

- The taxpayer’s grandchild or the taxpayer’s spouse’s grandchild

- The taxpayer’s or the taxpayer’s spouse’s parent or other ancestor

- Roth IRA conversions

- Qualified Domestic Relations Orders (QDROs) – A transfer from one spouse to another in the event of a divorce. (Why are these not called Qualified Domestic No Longer Have A Relationship Orders?)

III. Prohibited Transactions, Trusteed IRA’s, and LLCs Owned Under IRA

- Generally an IRA is limited to traditional investment categories

- Prohibited Investments Include:

- Life Insurance

- Certain types of derivative positions

- Antiques/Collectibles

- Most coins, but exceptions include

- One, one-half, one-quarter or one-tenth ounce U.S. gold coins (American Gold Eagle coins are the only gold coins specifically approved for IRAs. Other gold coins, to be eligible as IRA investments, must be at least .995 fine (99.5% pure);

- one ounce silver coins minted by the Treasury Department;

- any coin issued under the laws of any state;

- a platinum coin described in 31 USC § 5112(k) ; and

- gold, silver, platinum or palladium bullion (other than bullion that is made into a coin) of a certain fineness that is in the physical possession of a trustee that meets the requirements for IRA trustees under Code Sec. 408(a).

- IRA trustees are permitted to impose additional restrictions on investments. For example, while the IRS does not prohibit an IRA from investing funds in real estate, due to the administrative burdens many IRA trustees do not permit IRA owners to invest in real estate.

- However IRAs can invest in alternative arrangements if properly structured. Strict rules still apply, and the IRA can risk losing its tax-deferred status if these rules are violated.

- A prohibited transaction occurs when the IRA engages in a transaction with a disqualified person, which includes

- the IRA owner

- the IRA owner’s spouse

- the IRA owner’s ancestor

- the IRA owner’s lineal descendant

- any spouse of the IRA owner’s lineal descendant(s)

- investment advisors

- the IRA custodian or trustee

- certain entities in which the IRA owner owns at least 50% interest, such as a corporation, partnership or trust

- A prohibited transaction occurs when:

- sale or exchange, or leasing, of any property occurs between the IRA and a disqualified person;

- there is lending of money or other extension of credit between the IRA and a disqualified person;

- there is a furnishing of goods, services or facilities between the IRA and a disqualified person;

- the assets are transferred to – or used by or for the benefit of – a disqualified person;

- any action by a disqualified person who is a fiduciary whereby the fiduciary deals with the income or assets of the IRA in his or her own interests or for his or her own account; or

- receipt of any consideration by Plan Participant from any disqualified person who is a fiduciary dealing with the plan in connection with a transaction involving the income or assets of the plan

- For potential sample Operating Agreement language see Appendix B

IV. Access After 59 ½

- Distributions are taxable at ordinary income from a Traditional IRA unless:

- Rolled over within 60 days (only one per year per taxpayer under the Bobrow v. Commissioner case, discussed at Appendix D)

- Considered as a return of a nondeductible contribution

- The Coffee and Cream Situation (Partly Taxable Distributions)

- Basis (investment in the contract) is received for any non- deductible contributions or rolled over after tax amounts made into an IRA.

- Until your entire basis has been distributed, each distribution is partly non-taxable and partly taxable.

- The taxable and non-taxable portion is determined by the following formula:

![]()

V. Before 70 ½

- No distributions are required prior to reaching age 70 ½

- No difference between original owner, surviving spouse who received by roll over as direct beneficiary, or divorced spouse under QDRO

- Inherited IRAs are different, whether in trust or outright, minimum distribution rules will apply.

VI. After 70 ½ (actually after April 1 of the calendar year after the taxpayer reaches the age of 70 ½)

- Exception for Participant in Qualified Pension Plan who owns less than 5% of the Employer

- The Required Minimum Distribution rules apply during the lifetime of the taxpayer and/or to a surviving spouse who has rolled over an inherited IRA as a direct beneficiary thereof.

- $100,000 per year Charity Exception (Note – only extended through the 2014 tax year, but past history would indicate that it is likely to be extended to subsequent years)

VII. After Death of Participant

- Surviving Spouse Beneficiary

- Sole Beneficiary

- Spouse has option to roll over IRA and treat it as his or her own

- Can elect to be treated as beneficiary, and surviving spouse’s life expectancy will be recalculated annually

- Surviving spouse as sole beneficiary via estate/will or revocable trust

- One of multiple beneficiaries

- Separate Accounts can be established

- Spouse can elect to roll over his or her portion and treat as his or her own IRA.

- Surviving Spouse as beneficiary of Conduit Trust

- Surviving Spouse as beneficiary of Accumulation Trust.

- The best practice may be to have an Accumulation Trust that can be toggled into a Conduit Trust

- Income distribution requirements must be met for trust to qualify for the marital deduction.

- Sole Beneficiary

- Individual Beneficiaries

- Separate Account/Trust Rules

- Life Expectancies are not recalculated annually

- Charitable Beneficiaries

- Beware of the traps associated with having a charity named as a beneficiary of a trust that is named as beneficiary of the IRA/Plan

- Generally, as long as the charitable distribution is made directly from the IRA, it is not taxable

- Dispositions to Trust – Here is Where the Rest of the World Lies!

VIII. And Much More…

Stay tuned for the next installment of this series, Chapter Two, which will feature a rundown of the players involved in planning for ownership and inheritance of pension and IRA accounts and benefits, an acronym chart, and several illustrations to demonstrate different methods for calculating IRA distributions and enhance your learning experience.

Christopher Denicolo can be reached at christopher@gassmanpa.com.

******************************************************

[1] 134 S. Ct. 2242 (2014)

[2] Qualified Education Expenses include: tuition, fees, books, supplies, and equipment required for enrollment or attendance at an eligible educational institution. In addition if the student is at least a half-time student, room and board are qualified education expenses.

Well-Respected Multi-National Trust Company Opens Office in South Dakota – Very Nice Informational Book Available at No Charge!

Earlier this week, Trident Trust Company, Inc. announced the establishment of Trident Trust Company (South Dakota) Inc., a public trust company licensed and regulated by the South Dakota Division of Banking.

This new office will allow professional advisors and their clients to employ South Dakota’s highly-rated trust laws in a variety of planning situations including:

- Acting as trustee of South Dakota revocable and irrevocable trusts established by US or foreign settlors (grantors)

- Acting as trustee of Qualified Domestic Trusts (QDOT)

- Serving as successor trustee of foreign trusts re-domiciled into South Dakota

- Acting as trustee of South Dakota Dynasty Trusts

- Establishing and administering Private Trust Companies

To see a summary of the South Dakota trust legislation and the benefits Trident Trust can offer, please click here to download the free Quick Guide to South Dakota Trusts, provided courtesy of Trident Trust Company (South Dakota) Inc.

Richard Connolly’s World

Double Header

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares with us pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature some of Richard’s recommendations with a link to the articles.

This week, the first article of interest is “Trusts That Can Trim State Income Tax” by Liz Moyer. It was featured in The Wall Street Journal on January 23, 2015.

Richard’s description is as follows:

These trusts may have funny-sounding names, but for some high-net-worth individuals, they are serious tax-minimization tools.

Known as incomplete nongrantor trusts, they are often formed in Delaware, Nevada, and sometimes Wyoming, hence their acronyms DING, NING, and WING. Those states are chosen because they don’t tax the income of trusts established there, even by people who live elsewhere, or have favorable tax rules.

In a typical scenario, an individual would put into the trust an asset or assets that already have gone up a lot in value or that he or she hopes will appreciate sharply, such as shares in a private company that plans to go public. The aim is usually to sell the securities, at which point federal tax would be due – but not state tax. Alternatively, the trust could be used to hold assets that throw off a lot of income each year, sheltering that income from state tax.

While Ohio tax law makes use of this strategy difficult, this article could trigger inquiries from clients.

Please click here to read this article in its entirety.

The second article of interest this week is “Treasure Island: Puerto Rico Bids to Become New Age Tax Haven” by Lauren Gensler. The article was featured in the March 2, 2015 issue of Forbes magazine and was published on their website on February 11, 2015.

Richard’s description is as follows:

As the US Treasury Department continues to tighten its noose around offshore accounts, a new tax haven has sprung up under its nose in the Caribbean. Welcome to Puerto Rico, island of tropical breezes, and (for new arrivals only!) a 0% tax rate on certain dividends, interest, and capital gains.

Yes, this is legal. While the US asserts a sweeping right to tax citizens’ income wherever they live and wherever it’s earned, Section 933 of the tax code exempts residents of Puerto Rico from paying US income tax on their Puerto Rico sourced income. Instead, the Commonwealth of Puerto Rico has the exclusive right to tax local income as it sees fit.

Sadly, moving to Puerto Rico won’t buy you a total dispensation from the Internal Revenue Service. Uncle Sam still wants his cut on dividends you receive from US public companies, profits from mainland private businesses, pensions, and deferred compensation earned in the states, and Social Security benefits.

Make no mistake: to benefit from Act 22, you must become a bona fide Puerto Rico resident, which means being on the island at least 183 days a year. You can’t just rent a post office box in San Juan and call it “home” while keeping a $5 million house and your ties back in the States. Your business, family, bank and brokerage accounts, driver’s license and yacht should all move with you to the island.

To see this article in its entirety, please click here.

To see our write-up on this topic, co-authored with Puerto Rico attorney Erick Negrón, please click here.

Thoughtful Corner

Business Etiquette – Interacting with Clients & Colleagues

The following are a few tips concerning business etiquette when interacting with clients and colleagues.

1.) Learn How to Write

As a lawyer, you will be doing a lot of writing, including contracts, documents, letters, presentations, and more. This writing will be read by judges, clients, juries, and other attorneys.

Ask someone for an honest appraisal of your writing. Judges more than anyone go on and on about how poor many new lawyers are at drafting language for agreements, orders, and otherwise.

Clients have no way of knowing whether you are a good lawyer or not, but they will know if you cannot write worth a darn, and they will really know if what you write is not understandable to them. If the language in your correspondence to a client is not clear to the client, it probably won’t be comprehensible to a judge or a jury, either.

Ask someone else to read your letters and documents before you send them unless or until you truly have the hang of this invaluable skill.

Spend extra money as needed for a good proofreader or a good secretary. Require your employees to use spell check and grammar check, if available.

It is never too late to learn how to write, even if you are already a couple years out of law school, but it is too late to attempt to practice law before learning how to write. Documents and letters should not sound like an 8th grader’s text messages.

2.) Be on Time

Make every effort to arrive on time for appointments, whether that appointment takes place inside or outside of your office. Make every effort to be available for scheduled calls, if someone is scheduled to call you, or to be on the line on time if you are calling someone or calling in to a conference call.

Answer emails in a timely manner. Keep to previously agreed upon schedules, or make every effort to give ample notice if something in your schedule needs to change.

Clients and other business associates appreciate knowing that their time is respected and valued. Being on time is courteous and professional and will earn you the reverence of clients and colleagues.

3.) Do What You Say You Will Do

When you promise to deliver a work product and/or respond to a question in a specific time frame, make sure you honor that promise.

If you are unable to provide a response or a result in the time frame that you promised it, acknowledge this and apologize to the person who was waiting on you.

Doing what you say you will do demonstrates integrity. Your clients and associates will feel comfortable giving you work and/or referrals when they know that you will deliver what is promised.

This concludes our series on Business Etiquette. We will appreciate any questions, comments, or suggestions offered for the above article. It has been excerpted from a PowerPoint that we will present to third year law students and alumni (and you, too, if you would like to attend!) at the Ave Maria School of Law on a date to be determined. The presentation will be on professional acceleration. For more information, you can email Alan Gassman at agassman@gassmanpa.com or Janine Gunyan at janine@gassmanpa.com.

Humor! (or Lack Thereof!)

Leonard Nimoy’s Best Star Trek Quotes

The following are some of Leonard Nimoy and Mr. Spock’s best quotes:

“May I say that I have not thoroughly enjoyed serving with humans? I find their illogic and foolish emotions a constant irritant.” – Mr. Spock

“Computers make excellent and efficient servants, but I have no wish to serve under them.” – Mr. Spock

“My folks came to the US as immigrants, aliens, and became citizens. I was born in Boston, a citizen, went to Hollywood, and became an alien.” – Leonard Nimoy

“We must acknowledge once and for all that the purpose of a diplomacy is to prolong a crisis.” – Mr. Spock

“Spock is definitely one of my best friends. When I put on those ears, it’s not like just another day. When I become Spock, that day becomes something special.” – Leonard Nimoy

Upcoming Seminars and Webinars

LIVE ORLANDO PRESENTATION:

THE ADVANCED HEALTH LAW TOPICS AND CERTIFICATION REVIEW 2015

Alan Gassman will speak at The Advanced Health Law Topics and Certification Review 2015 on HEALTHCARE TAX ISSUES.

To see the complete schedule for this program, please click here.

Date: March 6 – 7, 2015 ǀ Alan Gassman will speak on March 6 at 11:00 AM

Location: Hyatt Regency Orlando International Airport | 9300 Jeff Fuqua Blvd., Orlando, FL 32827

Additional Information: For more information, please email agassman@gassmanpa.com.

***********************************************

LIVE WEBINAR:

Alan Gassman and Barry Flagg, CPF, CLU, ChFC, GFS, of Veralytic will present a 22.5-minute webinar on SPLIT-DOLLAR IN 15 MINUTES.

Date: March 17, 2015 | 5:00 p.m.

Location: Online webinar

Additional Information: To register, please click here or email Alan Gassman at agassman@gassmanpa.com for more information.

*******************************************************

LIVE WEBINAR:

Alan S. Gassman, Christopher J. Denicolo, and Edwin P. Marrow, III will present a 90-minute Strafford Publications, Inc. webinar entitled STRUCTURING JOINT EXEMPT STEP-UP TRUSTS: EVOLVING TOOL TO MAXIMIZE STEP-UP IN BASIS.

In an environment wherein the focus is shifting toward maximizing income tax basis step-up, counsel must be knowledgeable of all tools necessary to reach this goal. One tool that is beneficial for preserving both the inheritance tax exemption and basis step-up is the joint exempt step-up trust (JEST).

This panel will review questions such as:

- What are the best practices for structuring a JEST?

- What drafting techniques must be implemented to maximize basis step-up at both the first-to-die and surviving spouse’s deaths?

- What is the IRS guidance on this tool offered through the Technical Advice Memorandum and Private Letter Rulings?

- Under what circumstances is the JEST most appropriate?

Date: Tuesday, March 24, 2015 | 1:00 PM – 2:30 PM

Location: Online Webinar

Additional Information: For more information or to register, please click here. You may also email Alan Gassman at agassman@gassmanpa.com.

***************************************************

LIVE WEBINAR:

Alan Gassman and Barry Flagg, CPF, CLU, ChFC, GFS, of Veralytic will present a 30-minute webinar on COMPARING THE FINANCIAL STRENGTH AND RISKS ASSOCIATED WITH DIFFERENT LIFE INSURANCE CARRIERS.

Date: March 31, 2015 | 5:00 p.m.

Location: Online webinar

Additional Information: To register, please click here or email Alan Gassman at agassman@gassmanpa.com for more information.

*******************************************************

LIVE OLDSMAR PRESENTATION:

FICPA SUNCOAST SCRAMBLE GOLF TOURNAMENT

Kenneth J. Crotty and Christopher J. Denicolo will speak at the FICPA Suncoast Scramble Golf Tournament on the topic of MATHEMATICS FOR ESTATE PLANNERS INCLUDING 10 ESTATE PLANNING STRATEGIES NOT TO MISS.

Date: Friday, May 1, 2015 | CPE Presentations from 9:00 AM – 11:30 AM

Location: East Lake Woodlands Country Club | 1055 E Lake Woodlands Parkway, Oldsmar, FL 34677

Additional Information: For more information about registration, sponsorship, or this event, please click here or click here to download the Tournament brochure.

***********************************************************

LIVE NAPLES PRESENTATION:

2nd ANNUAL AVE MARIA SCHOOL OF LAW ESTATE PLANNING CONFERENCE

Alan Gassman, Jerry Hesch, and Richard Oshins will present THE MATHEMATICS OF ESTATE PLANNING. If you liked Donald Duck in Mathematics Land, you will love The Mathematics of Estate Planning. This will not be a Mickey Mouse presentation.

Other speakers include Richard Oshins on 11 Outstanding Planning Ideas, Jonathan Gopman on Asset Protection, Bill Snyder, Elizabeth Morgan, Greg Holtz, and others.

Please let us know any questions, comments, or suggestions you might have for this amazing conference, which features dual session selection opportunities in one of the most beautiful conference facilities that we have ever seen.

Date: Friday, May 1, 2015

Location: Ave Maria School of Law | 1025 Commons Circle, Naples, Florida

Additional Information: For more information, please click here or email Alan Gassman at agassman@gassmanpa.com.

******************************************************

LIVE MIAMI PRESENTATION:

FLORIDA BAR WEALTH PRESERVATION PROGRAM

Denis Kleinfeld and Alan Gassman have released the schedule and topics for FUNDAMENTALS OF ASSET PROTECTION AND ADVANCED STRATEGIES. This seminar will be presented on May 7th and May 8th, 2015, and is sponsored by the Tax Section of the Florida Bar. Attendees can select one day or the other, or to attend both days.

Day One will be for fundamentals and will be an excellent review or an introduction to the basic rules and practice aspects of creditor protection planning for both new and experienced practitioners.

Day Two will be an advanced treatment of creditor protection and associated planning, which will be of great use to both new and experienced practitioners.

Date: May 7 – 8, 2015

Location: Hyatt Regency Miami | 400 SE 2nd Avenue, Miami, FL 33131

Additional Information: To pre-register for this conference, please click here. For more information, please email Alan Gassman at agassman@gassmanpa.com.

***********************************************************

LIVE BRADENTON, FLORIDA PRESENTATION

Alan Gassman will speak at the Manatee County Physician Education Seminar on the topics of CREDITOR PROTECTION AND THE 10 BIGGEST MISTAKES DOCTORS CAN MAKE: WHAT THEY DIDN’T TEACH YOU IN MEDICAL SCHOOL.

Date: Tuesday, May 12, 2015 | Time TBA

Location: Surgery Center at Pointe West | 6015 Point,e West Boulevard, Bradenton, FL, 34209

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com.

**********************************************************

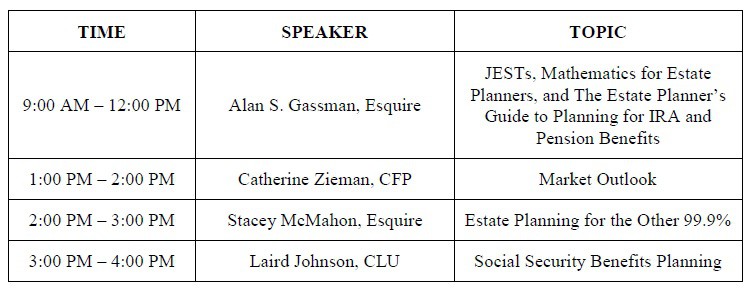

LIVE STUART, FLORIDA PRESENTATION

Alan Gassman will be the featured “headline” speaker the Martin County Estate Planning Council Annual Tax and Estate Planning Seminar. He will be doing a three-hour talk on the topics of JESTs, MATHEMATICS FOR ESTATE PLANNERS, AND THE ESTATE PLANNER’S GUIDE TO PLANNING FOR IRA AND PENSION BENEFITS – YES, YOU CAN FINALLY UNDERSTAND THESE RULES!

The tentative schedule for this one-day program is as follows:

Date: May 15, 2015 | 8:15 AM – 4:30 PM; Alan Gassman speaks from 9:00 AM to 12:00 PM

Location: Stuart Corinthian Yacht Club | 4725 SE Capstan Avenue, Stuart, FL 34997

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com or Lisa Clasen at lclasen@kslattorneys.com.

*************************************

LIVE FLORIDA INSTITUTE OF CPAs (FICPA) WEBINAR

Alan Gassman, Ken Crotty, and Chris Denicolo will present a webinar on A PRACTICAL TRUST PLANNING CHECKLIST AND PRACTITIONER COMPLIANCE GUIDE FOR FLORIDA CPAs for the Florida Institute of CPAs.

Review a practical planning checklist and practitioner tax compliance guide to facilitate implementing a comprehensive overview of practical planning matters and tax compliance issues in your practice. This presentation will cover over 20 common errors and missed planning opportunities that accountants need to understand and counsel their clients on.

This course is designed for practitioners who wish to assure that trust planning structures and compliance are both aligned with client objectives and that common catastrophic errors and misconceptions can be corrected.

Past attendees have indicated that this is an interesting and practical presentation that offers a great deal of practical information for both compliance and planning functions, based upon an easy to follow checklist approach. Includes valuable materials.

Date: May 21, 2015 | 10:00 a.m.

Location: Online webinar

Additional Information: For more information, please contact Alan Gassman at agassman@gassmanpa.com or Thelma Givens at givenst@ficpa.org. To register, please click here.

******************************************

LIVE SARASOTA PRESENTATION:

2015 MOTE VASCULAR SURGERY FELLOWS – FACTS OF LIFE TALK SEMINAR FOR FIRST YEAR SURGEONS

Alan Gassman will be speaking on the topic of ESTATE, MEDICAL PRACTICE, RETIREMENT, TAX, INSURANCE, AND BUY/SELL PLANNING – THE EARLIER YOU START, THE SOONER YOU WILL BE SECURE.

Date: Friday, October 23rd and Saturday, October 24th, 2015

Location: To Be Determined

Additional Information: Please contact Alan Gassman at agassman@gassmanpa.com for more information.

Notable Seminars by Others

(These conferences are so good that we were not invited to speak!)

LIVE PRESENTATION:

2015 UNIVERSITY OF FLORIDA TAX INSTITUTE

Date: Wednesday through Friday, April 22 – 24, 2015

Location: Grand Hyatt Tampa Bay | 2900 Bayport Drive, Tampa, FL 33607

Additional Information: Please contact Bruce Bokor at bruceb@jpfirm.com for more information.

**************************************

LIVE ORLANDO PRESENTATION:

50TH ANNUAL HECKERLING INSTITUTE ON ESTATE PLANNING

Date: January 11 – January 15, 2016

Location: Hotel information to be announced

Additional Information: Information on the 50th Annual Heckerling Institute on Estate Planning will be available on August 1, 2015. To learn about past Heckerling programs, please visit http://www.law.miami.edu/heckerling/.

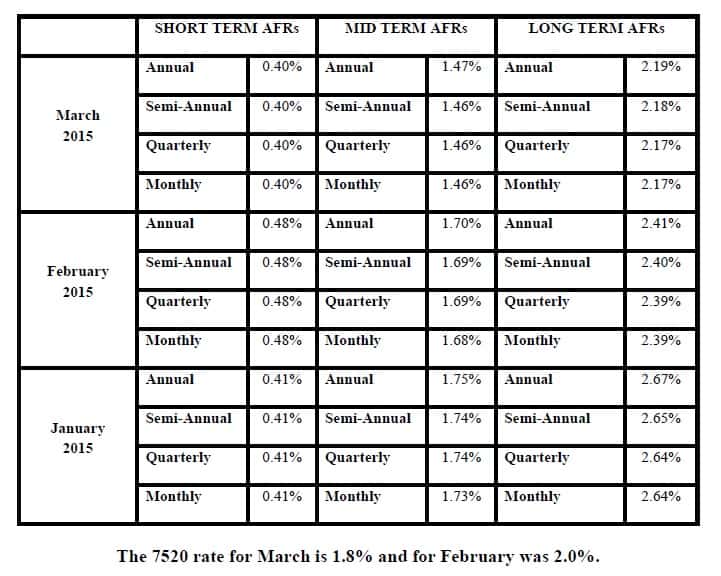

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.