The Thursday Report – January 23, 2014 – Dental Jokes, Heckerling & Steve Leimberg

Heckerling Pearls of Wisdom – Part 1

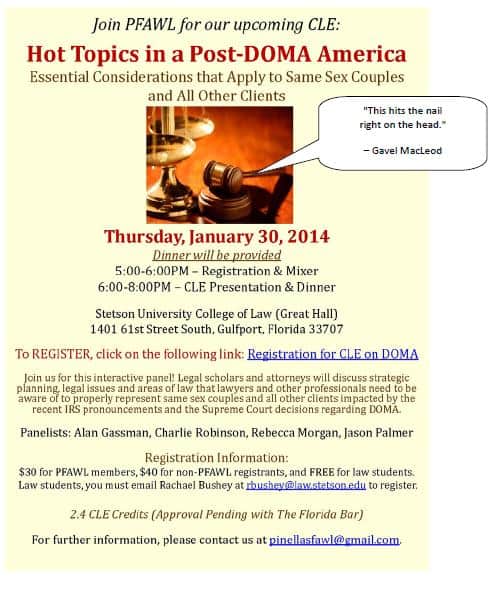

Seminar Announcements: Steve Leimberg’s Revolutionary Legal and Estate Planning Practice Acceleration Talk at the University of Florida Tax Institute and PFAWL CLE Talk on DOMA

Affordable Healthcare Plans – The Website is Working – Example Results

Physician Personal Creditor Protection Planning for Healthcare Lawyers and Financial Advisors – with Joel Bronstein’s Outline and Checklist

Lewis Saret’s Wealth Strategies Journal 2.0

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Heckerling Pearls of Wisdom – Part 1

We attended the University of Miami Heckerling Institute on Estate Planning last week and summarized a few of the outlines and presentations for our readers, which are as follows:

Thomas W. Abendroth – Portability: Now Available in Generic Form:

• Consider not using a credit shelter trust and instead relying on portability.

• Provide that assets of the first dying spouse equal in value to the spouse’s portability allowance will pass outright to the surviving spouse, and then have the surviving spouse make a gift to an irrevocable trust using the portability allowance. Because this will be a grantor trust for the surviving spouse he or she can pay the income taxes incurred on the trust assets, and will thus work much like a “super charged credit shelter trust”, with the one difference being that the surviving spouse will not be a beneficiary of the trust unless it is properly structured and situated in an asset protection jurisdiction.

• To use the GST exemption of the first dying spouse in the example above, have the excess assets of the first dying spouse be held in a QTIP, and make a reverse GST election on the estate tax return. This will allow the GST exemption of the first dying spouse to be used on the QTIP assets. Therefore, provide that assets disclaimed from the credit shelter trust will be payable to a QTIP trust to facilitate the above.

Paul Lee- Venn Diagrams: Meet Me at the Intersection of Estate and Income Tax

• Favor recommending estate tax planning strategies that use financial leverage (such as installment sales to grantor trusts and GRATs), rather than advising clients to make large lifetime gifts. Lifetime gifts only shield the future appreciation of the gifted assets from estate tax, while leveraged estate tax planning strategies that take advantage of the low interest rate environment can result in greater estate tax savings while preserving much of the client’s exemption that can otherwise be used in making a lifetime taxable gifts or reducing or eliminating eventual estate tax.

• Income tax planning has become an integral part of the estate planning process. With state and federal income tax rates sometimes exceeding the estate tax rate, advisors need to consider the income tax ramifications of estate planning strategies, and whether clients will be better served by prioritizing planning for income tax avoidance rather than estate tax avoidance. Accordingly, some clients will be better served by causing inclusion of assets in their taxable assets in order to obtain a step-up in basis.

• It is important to draft trust agreements to provide for flexibility for income tax planning in the future. One drafting strategy involves creating a committee of independent trust protectors that would have the power to bestow a general power of appointment upon the grantor’s spouse or other beneficiaries of the trust in order to cause estate tax inclusion for step-up basis purposes. Another is the possible use of the JEST (Joint Exempt Step Up Trust) for married couples residing in non community property states.

Richard W. Nenno – There’s No Place Like Home, But Where’s Home? The Role of “Residence” and “Domicile” in State Income and Transfer Tax Planning — Foreign Service Officers, Corporate Executives, NBA Referees, and More

• Learn what will cause an individual and a trust to be considered to be a resident of a state to be able to sever the contacts with the state to avoid having to pay income tax to that state.

• Change the location of the trust before there is a recognition event. The worst case scenario for clients is to be taxable in more than one state because of the location of the client’s domicile, residence, or place of employment.

Christopher R. Hoyt- Health Care Surtax: Individuals —- Dancing Under a 3.8% Limbo Pole

• The 3.8% Net Investment Income Tax went into effect for tax years ending after December 31, 2012 for affluent individuals, estates and trusts. The tax applies to the lesser of the taxpayer’s (1) Net Investment Income; or (2) the amount by which an individual taxpayer’s modified adjusted gross income exceeds $200,000 ($250,000 for married couples filing joint returns). For trusts and estates, the modified adjusted gross income threshold is $12,150 in 2014.

• “Net Investment Income” for the purposes of this tax means interest, dividends, annuities, royalties, rents, profits from a trade or business in which the taxpayer does not materially participate, profits from a trade or business of the trading of financial instruments or commodities (without regard to material participation), and taxable income from the disposition of property (such as capital assets) other than property disposed of in the course of the taxpayer’s trade or business in which the taxpayer materially participates.

• There are generally 2 ways to reduce a taxpayer’s exposure to the 3.8% surtax: (1) reduce the taxpayer’s income below the applicable threshold amount; or (2) reduce the taxpayer’s Net Investment Income, which can be done by converting income from Net Investment Income into income that is not Net Investment Income (e.g., by materially participating in the taxpayer’s trade or business), or by shifting Net Investment Income to family members in lower brackets or charities.

Donald O. Jansen– When Business Life Insurance Results in Income or Compensation — Depends on Who Owns the Policy

• Generally, where the employee owns the life insurance policy on his or her life, and the employer pays the premiums on the policy, the premium payments are considered to be compensation to the employee, and are therefore included in the employee’s gross income (with a corresponding deduction to the employer for the premiums paid). The policy death benefits are income tax-free under Internal Revenue Code Section 101.

• Where the employer owns the life insurance policy on the employee’s life, and the employer pays the premiums on the policy, the premium payments are generally not taxable to the employee if the employee does not actually or constructively receive the policy without substantial limitations.

• In some situations, both the employer and employee will share the cost responsibility for the life insurance policy on the life of the employee. The taxation of this type of arrangement is governed by the split dollar rules, which entitle the employer to receive out of the policy death benefits or the cash value of the policy at least the premium payments funded by the employer (or sometimes a larger amount). Split dollar arrangements generally can be divided into 2 categories: the loan regime, and the economic benefit regime. The loan regime entails the employee owning the policy and the employer loaning monies to the employee to provide funding for the policy premiums. At the termination of the split dollar arrangement, the employer would be entitled to receive repayment of its loan, with accrued interest based on a collateral assignment of the policy proceeds. Under the economic benefit regime, the employee provides funding for the premium payments each year based upon the “term cost” of the insurance coverage. The employee is the owner of the policy, and often endorses all or part of the policy proceeds to the employer to be payable upon the termination of the split dollar arrangement.

• When choosing between whether to use annual gifting and estate exemption allowances to allow for discounted entity transfers or to pay life insurance premiums, many planners will conclude that it is best to engage in discounted gifting while funding life insurance premiums by split dollar advances or from trusts that have assets that will be exempt from federal estate tax.

Gail E. Cohen- When You Must Adjust — How, When, Why and What Do the Professionals Do?

• The Uniform Principal and Income Act was enacted in 1997, and sets forth the general principle of investing trust assets for total returns. This approach blurs the distinction between income and principal, and gives the trustee discretion to adjust trust returns between principal and income.

• Fiduciaries need to consider potential conflicts of interest between current and remainder beneficiaries when exercising discretion in adjusting between principal and income. Often, the interests of current and remainder beneficiaries are at odds, and the fiduciary should be careful not to favor one class of beneficiaries over another without regard to maximizing the total return of the trust. With any decision, the trustee should document the process and reasoning for choosing an appropriate investment strategy for the trust in order to provide support for making the applicable decision.

• Trustee may implement a unitrust conversion whereby the trust will be converted into a unitrust that distributes a percentage of the value of the assets to the current beneficiaries each year. This can be a solution to balancing the interests of the current and remainder beneficiaries. This can occur under QTIP marital deduction trusts that would otherwise pay “income” to the surviving spouse.

Mickey R. Davis– Funding Unfunded Testamentary Trusts

• Funding testamentary trusts are often based upon formula funding clauses. The allocation of appreciation and depreciation that occurs between the date of death of the grantor and the date of funding is based upon the formula clause that is in the applicable trust instrument. The type of formula funding clause that is the best fit for a particular client generally cannot be determined at the time of drafting. Nevertheless, advisors should be wary of using pecuniary funding clauses in drafting testamentary trusts because an income tax realization event can occur if a pecuniary devise is funded with assets that have appreciated since the date of death.

• Consider the income tax basis of assets when funding testamentary trusts. For example, allocating appreciated assets to a marital trust might be preferable because the assets in the marital trust will receive a step-up in basis on the death of the surviving spouse. Also, it is important to coordinate probate assets with non-probate assets when funding credit shelter trusts.

• When credit shelter trusts are required to be funded per the trust instrument, but are not funded, advisors will need to look at their applicable state law to determine whether the credit shelter trust can be funded long after the decedent has died. There are several approaches that can be taken to address the issue of how assets are held under the law, and whether the IRS will respect the existence of the credit shelter trust. Mr. Davis’ outline goes into excellent detail with respect to these approaches.

Check back next week for more summaries from Heckerling.

Seminar Announcements:

Don’t Miss Steve Leimberg’s Revolutionary Legal and Estate Planning Practice Acceleration Talk in Tampa at the University of Florida Tax Institute on Friday, February 21, 2014 at the West Shore Hyatt at 8:30 a.m.

Steve Leimberg, Author and Photographer

(Click here to view Leimberg Information Systems.

Click here to view Steve Leimberg’s Photography Website)

“Steve Leimberg’s photography website gives naked trusts a new meaning.”

This talk alone is more than worth the $200 day pass cost, and the other speakers and topics for that day are as follows:

• 9:30 a.m. – John J. Scroggin on Basis Planning

• 11:00 a.m. – Lauren Y. Detzel and David Pratt on Formula Clauses: A-Z

• 12:15 p.m. – Samuel A. Donaldson on an Annual Update and Humor Extraordinaire!

All of that, of course, is secondary to the fact that our Thursday Report will be released the day before and personally autographed by Steve for anyone who has purchased any of the books that we are selling so that 75% of the sales revenues will go to the tax program.

Here is more information on Steve’s presentation. If you have never seen him speak you will not want to miss this:

WHAT’S IN IT FOR YOU?

Steve Leimberg’s MARKETING AN ESTATE PLANNING PRACTICE will show you how to build your name – and your firm’s name – into a brand name in your city – and bring more – and higher net worth quality clients into your office – and keep them there in a continuous lifelong stream.

Loaded with creative and innovative ideas, Leimberg’s talk will give you mind-stretching insights such as his “Positive Differentiation” Theorem, “Leimberg Leveraging”, the HT3 formula, The “Firestorm Technique”, The “Silence of the Lambs” Principal, The “Lexus” Technique, the “Nikon” Concept, “Mini-Marketing System, and “the “Pepperoni Bread Principle.

Steve’s objective is no less than to help you see the marketing of your name and your practice as the key to move your professional life to your “personal next level.”

You’ll learn Steve’s “mini-marketing systems” plan to effectively structure a stronger and even more successful estate, financial, business, employee benefit, and charitable planning practice.

You’ll learn the incredible marketing concepts that brought groups at the Heckerling Institute, the American Bar Association’s Tax Section Annual Meeting, The National Association of Estate Planners and Councils Annual Meeting, and the Annual Meeting of the AICPA’s Estate and Financial Planning Sections to their feet.

ABOUT STEVE LEIMBERG:

Steve Leimberg is “MR. MARKETING.” In a one month period of time, Steve was quoted in the Wall Street Journal and Fortune Magazine on Charitable Split Dollar, Forbes Magazine and Standard and Poor’s Outlook on Total Return UniTrusts, in Bloomberg’s Wealth Manager on Charitable Lead Trusts, and in Medical Economics on Abusive Trusts. The late Sylvia Porter called Steve Leimberg a crusader for personal financial freedom and he has served as an advisor for and TV show guest of Jayne Bryant Quinn. He was most recently quoted in the New York Times and Wall Street Journal.

If you are ready to move up to your “Personal Next Level” …

Don’t miss this very profitable session:

It will enrich your practice forever!

Also sign up for a trial membership of Steve Leimberg’s amazing newsletter system by clicking here.

Same Sex Marriage and Associated Laws We Should All Know About Anyway, on Thursday, January 30, 2014 at Stetson Law School

Affordable Health Care Plans – The Website is Working – Example Results

We asked our law students to tell us how Obama Care would apply for a Pinellas County based 40-year old earning $20,000 a year.

The Bronze Plan with a $6,300 deductible and no co-payment obligation beyond that would cost $34/month with Humana, or $50 a month with Humana with a $4,850 deductible and co-payments of $75 or less per doctor visit until a certain point is reached.

The Silver Plan would be $61/month for a $900 deductible and smaller co-pays.

The Gold Plan would be $97/month for a $2,500 deductible and smaller co-pays.

The Platinum plan would be $131/month for a $1,000 deductible and smaller co-pays.

The details and a checklist chart can be viewed by clicking HERE.

We have found clients who are paying more out of pocket for healthcare than what the Obama Plan would cost them, and those clients presently do not have access to expensive testing or facilities or specialists that are on the Obama Care plans.

The Obama Care website can be accessed by clicking HERE.

Another result of Obama Care is the extensive survey that hospital patients are requested to fill out.

A sample hospital survey for pediatric services to be filled out by parents is attached.

Pediatric hospitals certainly are going to have to stay on their toes when this type of feedback is being requested.

You can view the survey by clicking HERE.

Physician Personal Creditor Protection Planning for Healthcare Lawyers and Financial Advisors – with Joel Bronstein’s Outline and Checklist

On January 17, 2014, Joel Bronstein, Esq. of Bronstein, Carlson, Gleim & Smith in St. Petersburg, Florida presented an excellent outline and checklist to the 2014 Representing the Physician Annual Conference in Orlando, Florida.

Joel has been generous enough to give us permission to reproduce the outline and checklists, which can be viewed by clicking here.

We thank Joel not only for sharing his outline with the Thursday Report readers but also for the many times he has spoken at the Representing the Physician Seminar, and for his stewardship and dedication to The Florida Bar activities, including having been the Chairman of the Tax Section of The Florida Bar, and having served as the Chairman of the Continuing Legal Education Committee for The Florida Bar.

Joel’s contact information is as follows:

Joel D. Bronstein, Esquire

Bronstein, Carlson, Gleim & Smith

360 Central Avenue

Suite 1200

St. Petersburg, FL 33701

727-898-6691

jbronstein@bcgs-law.com

Lewis Saret’s Wealth Strategies Journal 2.0

Lewis Saret of Lewis J. Saret, Attorney at Law in Washington, DC has a fantastic Wealth Strategies Journal that he publishes on developments in estate planning and taxation, asset protection, business succession planning, fiduciary issues and many other issues. The Journal is free to anyone who wishes to receive it. To sign up please click here.

Here are some of the recent articles profiled in the Wealth Strategies Journal: (Click each one to be directed to the text of the article)

• NYT Article on How a Doctor Decided to Become a CFP

• Tax Break for IRA Gifts Expires Soon

• Oklahoma’s Reduction in Top Rate Ruled Unconstitutional

• New Mexico Supreme Court Legalizes Same-Sex Marriage Statewide

• How to Regain Tax Exempt Status

• The Affordable Care Act’s Impact on Business Reporting Requirements

• Developing A Medium Term Investment Strategy With A Three To Five Year Term

• Beware of Tax Preparer Fraud During Tax Season

• Alimony Payments and Tax Status

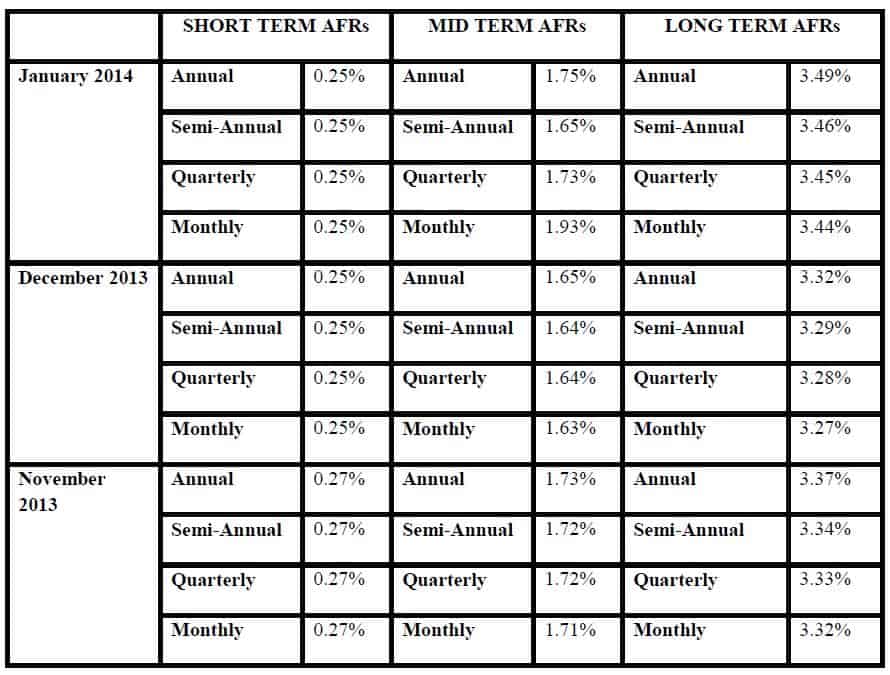

Applicable Federal Rates

Seminars and Webinars

THE 444 SHOW – USING FOCUS GROUPS TO CREATE EFFECTIVE TRIAL GRAPHICS

Date: Thursday, January 23, 2014 | 4:00 p.m.

Location: Online webinar

Speakers: Marcus Castillo and Josh Hoeppner

Additional Information: To register for the webinar please visit www.clearwaterbar.org

PINELLAS COUNTY CHAPTER OF THE FLORIDA ASSOCIATION OF WOMEN LAWYERS SEMINAR

Alan Gassman will be speaking on Same Sex Marriage and Associated Laws We Should All Know About Anyway.

Date: January 30, 2014 | 5:30 p.m.

Location: Stetson Law School, Gulfport, Florida

Additional Information: For more information on this event please contact agassman@gassmanpa.com.

UNIVERSITY OF FLORIDA TAX INSTITUTE INFORMATIONAL WEBINAR

Date: Tuesday, January 28, 2014 | 12:15 p.m.

Location: Online webinar

Speakers: Bruce Bokor, Alan Gassman, and additional speakers to be announced.

Additional Details: To register for the webinar please email Janine Gunyan at Janine@gassmanpa.com

LUNCH TALK – SOCIAL MEDIA

Date: Monday, February 3, 2014 | 12:30 p.m.

Location: Online webinar

Speaker: Aparna Tutak

Additional Information: To register for this webinar please visit www.clearwaterbar.org

INDIVIDUAL AND GROUP MEDICAL PRACTICES BLOOMBERG BNA WEBINAR

Health care attorney Lester Perling, Pension Actuary Jim Feutz and Alan Gassman will be presenting a 90 minute webinar for Bloomberg BNA Tax and Accounting on Individual and Group Medical Practices.

Date: February 13, 2014 | 12:00 – 1:30 p.m. (90 Minutes)

Location: Online webinar

Additional Information: Please contact agassman@gassmanpa.com for more information.

THE 444 SHOW – CREDITOR PROTECTION UPDATE

Date: Thursday, February 27, 2014 | 4:00 p.m.

Location: Online webinar.

Speaker: Alan Gassman

Additional Information: To register for the webinar please visit www.clearwaterbar.org

LUNCH TALK – LAWYER REFERRAL SERVICE

Date: Monday, March 3, 2014 | 12:30 p.m.

Location: Online webinar

Speaker: David Robert Ellis, Esq.

Additional Information:To register for the webinar please visit www.clearwaterbar.org

FLORIDA BAR HEALTH LAW REVIEW 2014

Alan Gassman will be speaking on What Healthcare Lawyers Need to Know About Tax Law and Business Entities at this excellent annual Florida Bar conference that is attended not only by those who are taking the Board Certification exam but also healthcare lawyers and other advisors.

Other speakers will include Lester Perling who is the co-author of A Practical Guide to Kickback and Self-Referral Laws for Florida Physicians and a number of other books and publications, and Mickey Mouse, Donald Duck and the “dwarf planet” formerly known as Pluto!

Date: March 7 – 8, 2014

Location: Hyatt, Orlando, Florida

Additional Information: We thank Jodi Laurence and Sandra Greenblatt for all of their hard work in making this conference as successful as it is. For more information please contact Jodi at jl@flhealthlaw.com or Sandra at sg@flhealthlawyer.com.

HILLSBOROUGH COUNTY BAR ASSOCIATION HEALTH LAW SECTION LUNCHEON

Alan Gassman and Christopher Denicolo will be speaking at the Hillsborough County Bar Association’s Health Law Section Luncheon on the topic of Tax and Asset Protection Basics for Those Who Represent Physicians and Medical Practices

Date: March 12, 2014

Location: Chester H. Ferguson Law Center in Tampa, FL

Additional Information: For additional information please contact Co-Chairs Sara Younger (sara.younger@baycare.org) or Thomas Ferrante (tferrante@carltonfields.com).

LUNCH TALK – LAW PRACTICE EFFICIENCY TIPS

Date: Monday, April 7, 2014 | 12:30 p.m.

Location: Online webinar

Speaker: Alan S. Gassman

Additional Information: To register for this webinar please visit www.clearwaterbar.org

FICPA SUNCOAST CHAPTER MONTHLY MEETING

Alan S. Gassman will be speaking at the FICPA Suncoast Chapter’s monthly meeting on the topic of THE FLORIDA CPA’S GUIDE TO PLANNING WITH PHYSICIANS AND MEDICAL PRACTICES

Date: Thursday, April 17, 2014 | 4:00 p.m.

Location: TBD

Additional Information: For more information on this event please email agassman@gassmanpa.com or mary@clawsonasplus.com

DONOR LUNCHEON AT RUTH ECKERD HALL WITH PROFESSOR JERRY HESCH IN CLEARWATER, FLORIDA

Professor Jerry Hesch will be speaking at a Donor Luncheon on the topic of CHARITABLE TAX SAVINGS: HOW TO MAKE SURE THAT UNCLE SAM CONTRIBUTES HIS SHARE TO MAXIMIZE RESULTS

Date: Tuesday, April 22, 2014 | TIME TO BE DETERMINED

Location: TBD

Additional Information: For additional information please contact Suzanne Ruley at sruley@rutheckerd.net or Alan Gassman at agassman@gassmanpa.com

RUTH ECKERD HALL PLANNED GIVING MEETING

Professor Jerry Hesch will be speaking at the Ruth Eckerd Hall Planned Giving Meeting in Clearwater, Florida on the topic of INNOVATIVE CHARITABLE GIVING TECHNIQUES FOR THE WELL TUNED ESTATE PLANNER

Date: Tuesday, April 22, 2014 | 4:00 p.m.

Location: TBD

Additional Information: This session qualifies for 1 hour of continuing education creditor for lawyers and CPA’s. To attend please email Suzanne Ruley at sruley@rutheckerd.net or Alan Gassman at agassman@gassmanpa.com

1st ANNUAL ESTATE PLANNER’S DAY AT AVE MARIA SCHOOL OF LAW

Speakers: Speakers will include Professor Jerry Hesch, Jonathan Gopman, Alan Gassman and others.

Date: April 25, 2014

Location: Ave Maria School of Law, Naples, Florida

Sponsors: Ave Maria School of Law, Collier County Estate Planning Council and more to be announced.

Additional Information: For more information on this event please contact agassman@gassmanpa.com.

THE FLORIDA BAR ANNUAL WEALTH PROTECTION SEMINAR

Date: Thursday, May 8, 2014

Speakers: Speakers will include Barry Engel on Offshore Trust Planning and Developments Over the Past 2 Years in Asset Protection, Howard Fisher and Alex Fisher on “Designer Entities – The Cutting Edge in Asset Protection”, Denis Kleinfeld on The Roadmap to Wealth Protection Planning and Alan Gassman on Structuring Business and Investment Assets and Entities – Wealth Protection 401 for the Dedicated Planner.

Location: Hyatt Regency Downtown, Miami, Florida

Additional Information: For more information please contact agassman@gassmanpa.com

NOTABLE SEMINARS PRESENTED BY OTHERS

16th ANNUAL ALL CHILDREN’S HOSPITAL ESTATE, TAX, LEGAL & FINANCIAL PLANNING SEMINAR

Date: Wednesday, February 12, 2014

Location: All Children’s Hospital Education and Conference Center, St. Petersburg, Florida with remote location live interactive viewings in Tampa, Sarasota, New Port Richey, Lakeland, and Bangkok, Thailand

Sponsor: All Children’s Hospital

THE UNIVERSITY OF FLORIDA TAX INSTITUTE

Date: February 19 – 21, 2014

Location: Grand Hyatt, Tampa, Florida

Presenters: Martin McMahon, Jr., C. Wells Hall, III, Abraham N.M. Shashy, Karen L. Hawkins, Lawrence Lokken, Stephen F. Gertzman, James B. Sowell, John J. Rooney, Louis Weller, Ronald Aucutt, Karen Gilbreath Sowell, Herbert N. Beller, Peter J. Genz, Stephan R. Leimberg, John J. Scroggin, Lauren Y. Detzel, David Pratt and Samuel A. Donaldson

Sponsor: UF Law alumni and UF Graduate Tax Program

Additional Information: For more information and to register for the program please visit www.floridataxinstitute.org. There will be cocktail parties at the Grand Hyatt as part of the programs on Wednesday, February 19 at 5:00 p.m. and then again on Thursday, February 20 at 5:00 p.m. Please plan to attend these receptions. See how your classmates are doing and say hello to your favorite professors. (If they didn’t teach at Florida then you can call them on your cell phone during the cocktail hour). Help us strengthen and improve a UF LLM community, the school, and the synergism that results from these types of activities. Students will be in attendance and will greatly value conversations with an advice from alumni. Do you remember how you felt when you were in the LL.M. program and were able to interact with successful lawyers who gave you valuable feedback? There is also a reception for all attendees and the guests on February 10, 2014 at 5:00 p.m. for attendees and their spouses along with a reception on February 11, 2014 at 5:00 p.m. to thank the supports of the University of Florida, the law school and the LL.M. program.