Thursday Report – Issue 286

Edited By: Wesley Dickson

Thursday, August 20, 2020

Issue 286

Bar Exam Canceled – So Glad We Passed It Decades Ago!

When to Unplug Great Grandpa: Part 2

Understanding the PPP Workforce Reduction Rules After the August 4th, 2020 FAQs

For Finkel’s Followers

This Day in History and Humor

Upcoming Events

August 20 is a big day for NASA. On this day in 1975, NASA launched the Viking 1 probe towards Mars and exactly two years later launched the Voyager 2.

If I was NASA, I would have given the two missions a little space.

On August 20, 2019, NASA announced its plan to launch a mission to Jupiter’s ice-covered moon Europa with the intent of searching for life forms in 2025.

Trivia – Whose Father worked for NASA for over 25 years and interacted frequently with Wernher von Braun?

Email – info@gassmanpa.com with your answer!

Bar Exam Canceled – So Glad We Passed It Decades Ago!

This week’s news that the Florida Bar Exam had to be canceled less than 96 hours before applicants were set to go on their computers and take a one-day abbreviated version of the traditional test brought home that there are and will be many unexpected victims of COVID-19, and that we can be very thankful that we have our professional and home situations under control, while helping others.

Some of the emails that I received from young lawyers who missed taking the bar exam this week helped to bring this home. One student explained, “I paid Themis (a bar review company) over $2,000 and studied over 40 hours per week just to receive an email 3 days before the exam that it has been postponed again. I would never treat a client the way the Florida Bar has treated me.”

A second email that I was given permission to publish can be read below:

Dear Mr. Gassman,

I am not a job applicant, but since you included your email for potential applicants in your excellent Forbes article, I thought I would go ahead and email you anyway to thank you very much for your excellent and thorough article. Like many examinees, I’ve felt as though I’ve been shouting into the void for the last several months, and reading your article was the first time that it seemed like someone had heard. Your article laid out clearly the timeline of our frustrations, and I am so glad to have something to send to my family members that explains it better than my flustered phone calls have. It is also extremely cool of you to offer to hire two of my fellow in-limbo examinees in the interim. I have no doubt that you’ll find top-shelf people; this cohort is a hardy one. My very best wishes to you and yours in this unprecedented time.

Thank you again,

(name omitted)

Resilience is defined as the capacity to recover quickly from difficulties or toughness.

While we all have much to be thankful for, keeping resilience on the list, and remembering that life would not be nearly as much fun without challenges can help.

For all of you lawyers and other professionals who may need help with research, writing projects, or even backed-up clerical work, please keep in mind that there are over 1,100 individuals who would have taken the bar this week, and now must take it sometime in October, and have limited employment opportunities between now and then.

If you would like to receive some of the resumes that we have gotten as the result of our article please put “Send Resumes” in the RE line of an email to me and I will send you the resumes of those recent graduates who have consented to sharing these.

Our two articles on this situation can be viewed by clicking on the following links.

Over 1,000 Young Lawyers Are Stranded As Florida Bar Exam Is Canceled On 72 Hours Notice

Florida Bar Exam Catastrophe: Part 2 – And An Apology From The Florida Supreme Court

Please click several times because I get paid $0.001 per new reader. If you click 1,000,000 times I get $5.00!

When to Unplug Great Grandpa: Part 2

In 2011, I published an article in Estate Planning Magazine called Unplugging Great-Grandpa: Curious Consequences of the Current Estate Tax Regime, Email info@gassmanpa.com for a copy. I wrote it as both a parody and a summary of where the estate tax situation was at that time for individuals who could die in 2012 with up to $5,120,000 in assets without estate tax, when the exemption was coming down to $1,000,000 on January 1, 2013, due to the end of a 10-year tax cut, much like what is now in place to end on January 1, 2026.

Now we have a situation where taxes may be significantly increased in 2021, and legislation for this could be passed in the middle or even towards the end of 2021, to be effective January 1, 2021.

I am hoping that this will not occur anytime soon, and that if there is an estate tax exemption reduction (from the present level of $11,580,000 per person) that there will be plenty of warning for wealthy clients to make use of what remains of their estate and gift tax exemption, but Murphy’s Law says to plan for the worst, and has been true on many occasions.

It is therefore important to be ready for the possibility that Benjamin Franklin’s adage that there is nothing for certain but death or taxes may shine true with an increase of what families have to pay after the death of a loved one.

The increase in taxes would come not only from the lower estate tax exemption, but could also come from higher estate tax rates, capital gains to be paid on appreciated assets after a person dies, and higher ordinary income rates to apply when IRAs, annuity investments, and other items that we call “income with respect to a descendant” are paid out.

WHAT CAN A PERSON DO?

Besides being prepared with the knowledge of “when to unplug great-grandpa,” affluent families can plan now to determine how each individual can best use their $11,580,000 exclusion if and when the time comes that they must “use it or lose it.”

It is always surprising to me how many families with significant wealth have not addressed this issue, or done the type of planning with family limited partnerships, family limited liability companies, sales to trusts in exchange for notes bearing interest at low rates, or other opportunities that might not be available in the future.

Sometimes it occurs to me that Survival of the Fittest includes the fact that “smart and responsible people and their families will survive economically, and not so smart, unresponsive, or ill-advised wealthy families may not be so wealthy because of lack of taking the right steps.”

It was me who said the above, but I thought it looked better in quotes.

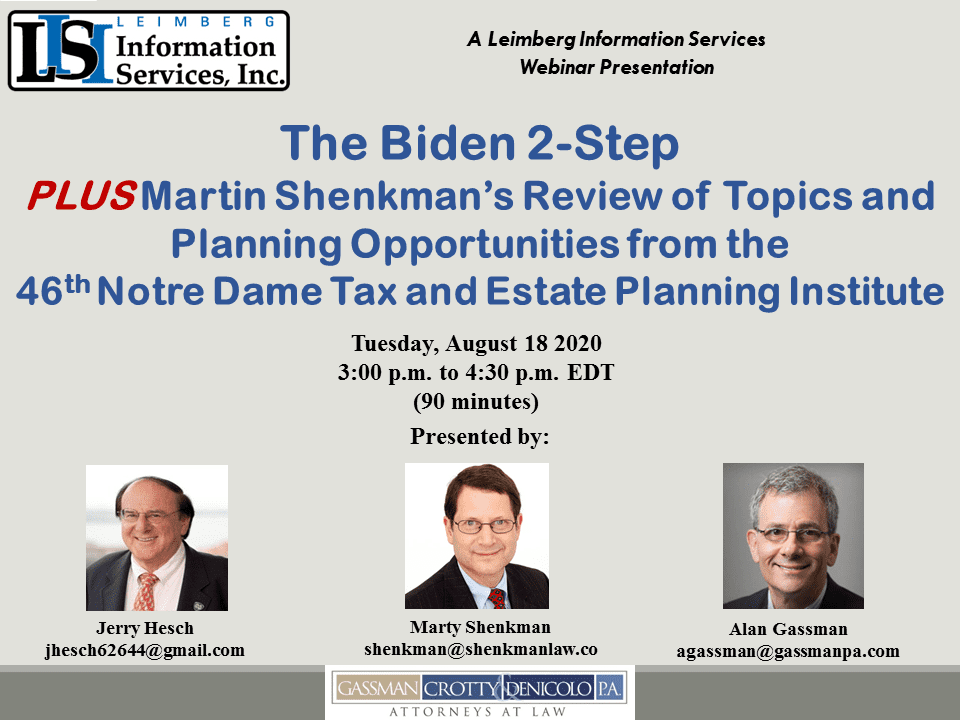

Tuesday I recorded a webinar called The Biden 2-Step that can be viewed on YouTube HERE.

For a copy of our article on the above email info@gassmanpa.com.

If there are significant tax law increases we may see the elimination of a new fair market value income tax basis that occurs for most assets when someone dies, higher income tax rates, and even possibly a capital gains tax that occurs on death, as if a person who died sold all of their assets, which is what the tax law of Canada has been for many years.

Families should at least budget for what the tax will be if these days come, and possibly consider reducing living expenses (including “non-necessary luxuries”) so that family wealth reserves and investments do not have to be depleted to pay for lifestyles that might not be affordable now, or at least after a tax increase.

Some families will need counseling to accomplish this, and others will be unable to ratchet down spending, thus making space for the next generation of affluent families who may win the next round of the never-ending battles with respect to “Survival of the Fittest” families in our unique society.

Such families are well-advised to stay in close contact with their certified public accountants, tax lawyers, and financial advisors to make sure that they are getting the best advice, especially between now and year-end, where the time and energy of such advisors may be relatively limited given the number of individuals and families that may be seeking advice “at the last minute” after the election.

By the way, the states that have more liberal rules to allow for someone with a terminal condition to complete their estate tax planning early (by dying) are as follows:

- California – End of Life Options Act – ABX2-15

- Colorado – End of Life Options Act – Proposition 106

- District of Columbia – Death with Dignity Act of 2016 – B21-0038

- Hawaii – Hawai’i Our Care, Our Choice Act – HB 2739

- Maine – Maine Death with Dignity Act – HP 948

- New Jersey – Aid in Dying for the Terminally Ill Act – Bill A1504

- Oregon – Oregon Death with Dignity Act – Ballot Measure 16

- Vermont – Patient Choice and Control at the End of Life Act (Act 39) – bill S.77

- Washington – Death with Dignity Act – Ballot Initiative 1000

- Montana – Baxter v. State, 224 P.3d 1211 (Mont. 2009)

I hope not to see you there.

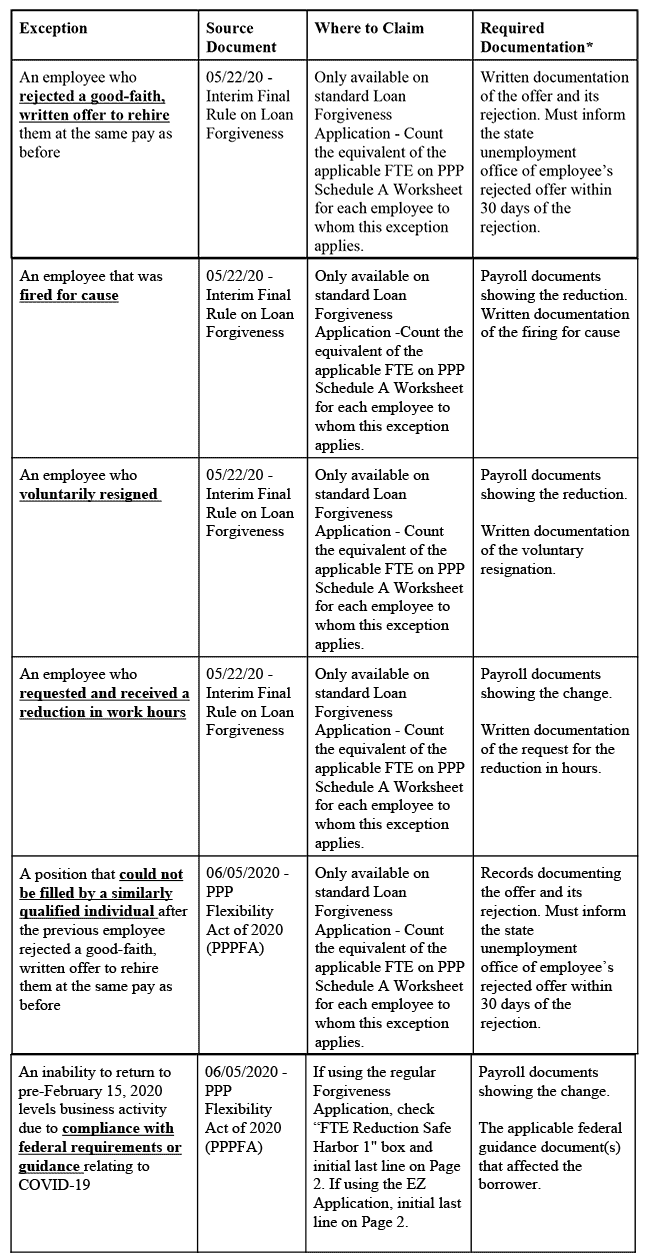

Understanding the PPP Workforce Reduction Rules After the August 4th, 2020 FAQs

Exceptions, guidance, and resources.

The most important aspect of the Paycheck Protection Program is a borrower’s ability to have their loan forgiven if they meet certain criteria. Under the CARES Act, which created the PPP, one of those criterion was that, during their loan coverage period, the borrower had to maintain the same workforce levels they had prior to February 15, 2020. After all, the whole point of the PPP was to keep workers employed throughout the COVID crisis. Borrowers who didn’t maintain their workforce hours (or FTE as it is known in the PPP world) would have a pro rata reduction in forgiveness unless they met one of the six exceptions provided by the rules.

The SBA introduced the four original exceptions in an Interim Final Rule released on May 22nd. The PPP Flexibility Act of 2020, which was enacted on June 5th, created two new exceptions, the most notable of which provides that a reduction in workforce hours that is the result of an effort by the borrower to comply with federal COVID related health laws or guidelines will be excused from any reduction in forgiveness associated therewith. It is important to note that this is the only exception that can be used in the EZ Forgiveness Application, which does not require any detail or calculations as to this exception on the Application itself.

Furthermore, on August 4th, 2020, after over a month of silence regarding PPP guidance, the SBA issued 23 new Frequently Asked Questions and Answers, a number of which provided guidance on workforce reductions and how they would affect a borrower’s forgiveness. As borrowers proceed through their covered periods they are often finding themselves in workforce reduction scenarios that are quite specific to their business, but how those scenarios should be treated for forgiveness purposes can be ambiguous under the current rules. The August 4th guidance will be discussed in greater detail later in this article.

The chart below summarizes the key characteristics of each exception as of August 4th, 2020:

*Borrowers are required to maintain, but not necessarily submit, all of the above required documentation. Borrowers must maintain such required documentation for 6 years following forgiveness of the loan.

Given the circumstances of many borrowers who reduced workforce hours, this new exception for compliance with government health guidelines will be an important “get out of jail free card”.

Here is what we know about how to determine whether a workforce hours reduction can be considered to have been attributable to federal health guidelines so far:

Thousands of borrowers who took PPP loans but were subsequently compelled to close or limit business operations in compliance with government orders were left wondering “what about us?”

A looming question for PPP borrowers once local governments and states began to hand down shutdown orders was how will this affect my PPP loan? How is a business supposed to spend their loan proceeds appropriately and avoid reducing their workforce hours if the state orders them to close up shop during their covered period? Surely, these borrowers could not be punished. Their workforce reductions were not their own doing. Rather, it was the government’s.

The enactment of the PPP Flexibility Act of 2020 on June 5th began to address this question by stating that businesses would not be punished for a reduction in FTEs due to compliance with requirements or guidance issued by the CDC, HHS, or OSHA, but did not address compliance with local or state-issued shutdown orders. This glaring omission in the exception rules was addressed by the June 22nd Interim Final Rules which states that since state and local government orders are based in part on guidance from the three federal agencies mentioned above, that those who were forced to reduce their workforce hours in compliance with government orders and guidelines would also not be penalized. The June 22nd Interim Final Rules are discussed in more detail below.

The applicable language of the Act is as follows:

During the period beginning on February 15, 2020, and ending on December 31, 2020, the amount of loan forgiveness under this section shall be determined without regard to a proportional reduction in the number of full-time equivalent employees if an eligible recipient, in good faith is able to document an inability to return to the same level of business activity as such business was operating at before February 15, 2020, due to compliance with requirements established or guidance issued by the Secretary of Health and Human Services, the Director of the Centers for Disease Control and Prevention, or the Occupational Safety and Health Administration during the period beginning on March 1, 2020, and ending December 31, 2020, related to the maintenance of standards for sanitation, social distancing, or any other worker or customer safety requirement related to COVID–19.

How does this new exception apply to borrowers?

Though the language above is short, there is much information to be analyzed and understood.

First, the period for which this exception applies is only from February 15th to December 31st.

At the time that new exception was released some interpreted the rules to mean that borrowers seeking to claim the exception would need to wait until after December 31st to file for forgiveness.

Fortunately, the SBA has since announced that borrowers may file for forgiveness any time after their loan proceeds have been properly spent. This fixed time period also means that borrowers who got their loan early and finished their covered period before June 5th (when the exception was created) can retroactively claim the new exception if they have not filed for forgiveness yet.

The exception states that businesses must be unable to return to “the same level of business activity” that they were operating at prior to February 15th. While “business activity” has never been explicitly defined, we can safely assume it is likely to be by reference to the borrower’s total employee hours or other appropriate unit of measurement. This is because the Flexibility Act says a “reduction in the number of full-time equivalent employees” will be excepted from loan forgiveness reductions if this exception is claimed. This is opposed to an interpretation of “same level of business activity” that would be more related to sales, units manufactured, or some other indicator.

The fact that borrowers can only cite to guidance issued during the period from March 1st to December 31st as evidence of compliance with government guidelines creates an interesting paradox. This is because borrowers must maintain their workforce as of before February 15th while the exception states that a borrower can only cite to guidance issued after March 1st as evidence of compliance with government guidelines. In effect, this could mean that any workforce reduction that occurred between February 15th and March 1st cannot be disregarded under this new exception, but that does not seem to be what was intended, so this 14 day gap will probably be ignored by most applicants.

This new exception doesn’t ask much of a borrower seeking to claim it – only that they are able to, “in good faith,” document their inability to operate at the pre-February 15th level. But what exactly does that mean? For one, we know that borrowers can only claim an inability to operate as it pertains to “the maintenance of standards for sanitation, social distancing, or any other worker or customer safety requirement related to COVID–19.” Since borrowers are required to “document” their inability to operate, this likely means that they will be required to produce evidence of the amount of workforce hours that were eliminated as well as the borrower’s reason for doing so. For example, a borrower’s attestation that they had to reduce their workforce “because of social distancing” will not be sufficient. Instead, a borrower could document that given “the confined dimensions of the workspace and the recommended 6 foot distance between individuals in this setting, it would be impracticable to maintain the same number of employees and shift rotation schedule.”

State Law Indirectly Applies.

Finally, as is a standard pattern with PPP guidance, the apparently not so thoroughly thought out creation of this exception led to even more questions. The Act states that a borrower who complies with CDC, HHS, or OSHA guidelines may claim the new exception. This limitation appeared to leave borrowers who shut down or reduced their operations in compliance with state or local guidelines out in the cold.

The SBA addressed this lingering issue in the Interim Final Rule on Revisions to Loan Forgiveness Interim Final Rule released on June 22nd by allowing State law required close-downs to qualify.

What Does the Interim Final Rule Issued on June 22 Mean for Borrowers?

The new June 22nd Interim Final Rule provides as follows:

Borrowers are also exempted from the loan forgiveness reduction arising from a reduction in the number of FTE employees during the covered period if the borrower is able to document in good faith an inability to return to the same level of business activity as the borrower was operating at before February 15, 2020, due to compliance with requirements established or guidance issued between March 1, 2020 and December 31, 2020 by the Secretary of Health and Human Services, the Director of the Centers for Disease Control and Prevention (CDC), or the Occupational Safety and Health Administration related to the maintenance of standards for sanitation, social distancing, or any other worker or customer safety requirement related to COVID–19 (COVID Requirements or Guidance). Specifically, borrowers that can certify that they have documented in good faith that their reduction in business activity during the covered period stems directly or indirectly from compliance with such COVID Requirements or Guidance are exempt from any reduction in their forgiveness amount stemming from a reduction in FTE employees during the covered period. Such documentation must include copies of applicable COVID Requirements or Guidance for each business location and relevant borrower financial records.

The Administrator, in consultation with the Secretary, is interpreting the above statutory exemption to include both direct and indirect compliance with COVID Requirements or Guidance, because a significant amount of the reduction in business activity stemming from COVID Requirements or Guidance is the result of state and local government shutdown orders that are based in part on guidance from the three federal agencies.

Further, according to the CDC, their guidance is “meant to supplement – not replace – any state, local, territorial, or tribal health and safety laws, rules, and regulations with which businesses must comply.”

It appears that the key to successfully claiming the exception for compliance with government health guidelines will be proper documentation. This makes sense since a great many borrowers reduced their workforces in order to stay compliant with CDC guidelines. But what exactly does proper documentation entail? The June 22nd Interim Final Rule specifically states, “[proper] documentation must include copies of applicable COVID Requirements or Guidance for each business location and relevant borrower financial records.”

Not only will borrowers be required to cite to the specific guidance document that their action was in compliance with, but they will also be required to produce applicable financial records, which will likely include payroll statements.

It may also be best practice for a borrower to document each step taken towards maintaining compliance with the guideline they are relying upon. For example, a borrower that reduced hours of operation might consider attaching an addendum to their forgiveness application that states “in compliance with CDC Guideline #1234, which suggests limiting a business’s hours of operation to daylight hours only, Borrower has taken the necessary steps to adjust its’ hours of operation and has reduced its’ workforce by 10% to account for the reduced hours of operations.”

One more item of note is the fact that there doesn’t seem to be a time requirement for compliance with requirements or guidance issued. If this is the case, a borrower that was shut down for only a short-time by say a “shelter in place order” from its local government may be able to claim this exception for the entire Covered Period. While it remains unknown if the SBA would accept this method for claiming the exception, there hasn’t been any indication they will not. Further guidance from SBA on how to apply this exception would certainly be welcomed.

Borrowers hoping to claim this exception due to state or local government orders should look to the order that affected them to see if that order specifically cites to guidance from the HHS, CDC, or OSHA. When documenting this exception it will be best practice to include the state order, the federal guidance the state order cites to. Tracking down the correct guidance document can prove to be difficult considering that, between the three applicable federal agencies, hundreds of COVID guidance documents have been released since March 1st. Thankfully, all three agencies provide searchable indexes of their guidance documents. Links to those indexes can be found below:

CDC – https://www.cdc.gov/coronavirus/2019-ncov/communication/guidance-list.html?Sort=Date%3A%3Adesc

OSHA – https://www.osha.gov/pls/publications/publication.AthruZ?pType=AthruZ#C

HHS – https://www.hhs.gov/coronavirus/index.html

How to claim this exception on the Forgiveness Applications

It is one thing to qualify for this exception. It is another thing to actually claim it on the correct application when it comes time to file for forgiveness. While each of the exceptions requires a borrower to submit supporting documentation, different exceptions will require different steps from the borrower depending on which forgiveness application the borrower is submitting.

The Forgiveness Application EZ:

Most borrowers that (1) did not reduce the annual salary or hourly wages of any employee by more than 25% during the covered period AND (2) was unable to operate at the same level of business activity as before February 15, 2020 due to compliance with requirements established or guidance issued prior to March 1st can file for forgiveness using the PPP Loan Forgiveness Application Form 3508EZ.

The EZ Application was designed to allow small borrowers and those who knew they would not be subject to forgiveness reductions to quickly and easily apply for forgiveness. This is why a borrower is able to claim the exception for compliance with federal guidelines on the EZ Application. Imagine for a moment that you are a borrower that owns a non-essential business that was ordered to close immediately after you received your PPP loan, and you stayed closed for the remainder of your covered period. Obviously, you likely would not have been able to maintain full employment and you will have reduced your workforce hours. The exception still allows you to obtain full forgiveness in this scenario, assuming that the loaned amount was spent on payroll costs for the employees that you were able to retain or other permitted non payroll costs, but it would be a waste of time to fill out the entire 5 page regular Forgiveness Application which requires complex calculations and documentation. Instead, you may claim the exception simply by filling out the EZ Application as required and initialing the last line on Page 2 just before the signature blocks. You will still need to provide the applicable documentation, of course. But claiming this exception on the EZ Application will be as easy as checking a box.

The Standard Loan Forgiveness Application

The claiming the exception on the standard loan forgiveness application operates much the same way that it does on the EZ Application. Again, the borrower will simply be required to initial the last line on page 2 just before the signature blocks. Borrowers will still need to provide all applicable documentation to successfully claim the exception on the standard loan forgiveness application.

Interestingly, a borrower is never asked to perform any calculations in an effort to claim the exception for compliance with federal health guidelines. Instead, on both applications, borrowers are simply required to certify in good faith that they were “unable to operate between February 15, 2020 and the end of the Covered Period at the same level of business activity as before February 15, 2020 due to compliance with [federal health guidelines].” The standard loan forgiveness application does require one additional step which is to check the box near the bottom of page 3 that indicates the borrower qualifies for FTE Reduction Safe Harbor #1.

By only requiring a good faith certification, the SBA has effectively made this an “all-or-nothing” exception. Your reductions are either entirely forgiven or they are not. This is opposed to the other 5 exceptions which require a borrower to calculate and include on the PPP Schedule A Worksheet the FTE of an employee to which the exceptions apply.

How to Account for Workforce Salary Reductions

It is inevitable that workforce reductions that cannot be discounted by the above-mentioned exceptions will occur for some borrowers, especially in scenarios where an employee’s salary or hourly wage was reduced. These types of scenarios are addressed by FAQ #4 under the Loan Forgiveness Reductions FAQs section of the August 4th FAQ release.

Regarding pay reduction’s effects on forgiveness the FAQ states, “If the salary or hourly wage of a covered employee is reduced by more than 25% during the Covered Period or the Alternative Payroll Covered Period, the portion in excess of 25% reduces the eligible forgiveness amount unless the borrower satisfies the Salary/Hourly Wage Reduction Safe Harbor.” Question #4 also provides three extremely helpful examples that illustrate how a borrower should handle pay reductions when it comes to applying for forgiveness.

Example 1: A borrower received its PPP loan before June 5, 2020 and elected to use an eight-week covered period. Its full-time salaried employee’s pay was reduced during the Covered Period from $52,000 per year to $36,400 per year on April 23, 2020 and not restored by December 31, 2020. The employee continued to work on a full-time basis with a full-time equivalency (FTE) of 1.0. The borrower should refer to the “Salary/Hourly Wage Reduction” section under the “Instructions for PPP Schedule A Worksheet” in the PPP Loan Forgiveness Application Instructions. In Step 1, the borrower enters the figures in 1.a, 1.b, and 1.c, and because annual salary was reduced by more than 25%, the borrower proceeds to Step 2. Under Step 2, because the salary reduction was not remedied by December 31, 2020, the Salary/Hourly Wage Reduction Safe Harbor is not met, and the borrower is required to proceed to Step 3. Under Step 3.a., $39,000 (75% of $52,000) is the minimum salary that must be maintained to avoid a penalty. Salary was reduced to $36,400, and the excess reduction of $2,600 is entered in Step 3.b. Because this employee is salaried, in Step 3.e., the borrower would multiply the excess reduction of $2,600 by 8 (if it had instead selected a 24-week Covered Period, it would multiply by 24) and divide by 52 to arrive at a loan forgiveness reduction amount of $400. The borrower would enter on the PPP Schedule A Worksheet, Table 1, $400 as the salary/hourly wage reduction in the column above box 3 for that employee.

This particular example is helpful because, previously, many people had interpreted the 25% wage reduction rule to include the entire percentage reduction in wages when calculating the forgiveness reduction as opposed to just the amount of the wage reduction that exceeded the 25% reduction threshold.

Example 2: A borrower received its PPP loan before June 5, 2020 and elected to use a 24-week Covered Period. An hourly employee’s hourly wage was reduced from $20 per hour to $15 per hour during the Covered Period. The employee worked 10 hours per week between January 1, 2020 and March 31, 2020. The borrower should refer to the “Salary/Hourly Wage Reduction” section under the “Instructions for PPP Schedule A Worksheet” in the PPP Loan Forgiveness Application Instructions. Because the employee’s hourly wage was reduced by exactly 25% (from $20 per hour to $15 per hour), the wage reduction does not reduce the eligible forgiveness amount. The amount on line 1.c would be 0.75 or more, so the borrower would enter $0 in the Salary/Hourly Wage Reduction column for that employee on the PPP Schedule A Worksheet, Table 1.

If the same employee’s hourly wage had been reduced to $14 per hour, the reduction would be more than 25%, and the borrower would proceed to Step 2. If that reduction were not remedied as of December 31, 2020, the borrower would proceed to Step 3. This reduction in hourly wage in excess of 25% is $1 per hour. In Step 3, the borrower would multiply $1 per hour by 10 hours per week to determine the weekly salary reduction. The borrower would then multiply the weekly salary reduction by 24 (because the borrower is using a 24-week Covered Period). The borrower would enter $240 in the Salary/Hourly Wage Reduction column for that employee on the PPP Schedule A Worksheet, Table 1. If the borrower applies for forgiveness before the end of the 24-week Covered Period, it must account for the salary reduction (the excess reduction over 25%, or $240) for the full 24-week Covered Period.

This example once and for all clarifies that the 25% reduction rule only applies to reductions in excess of 25%. So long as an employee’s salary is not reduced by more than 25%, the borrower will not have to account for the wage reduction in their forgiveness calculations.

Example 3: An employee earned a wage of $20 per hour between January 1, 2020 and March 31, 2020 and worked 40 hours per week. During the Covered Period, the employee’s wage was not changed, but his or her hours were reduced to 25 hours per week. In this case, the salary/hourly wage reduction for that employee is zero, because the hourly wage was unchanged. As a result, the borrower would enter $0 in the Salary/Hourly Wage Reduction column for that employee on the PPP Schedule A Worksheet, Table 1. The employee’s reduction in hours would be taken into account in the borrower’s calculation of its FTE during the Covered Period, which is calculated separately and may result in a reduction of the borrower’s loan forgiveness amount.

This example is important because it clarifies that the 25% wage reduction rule only applies to actual reductions in wages as opposed to a reduction in total compensation that resulted from a reduction in the employee’s working hours.

The exception for compliance with federal health guidelines is arguably the greatest relief the SBA has provided to borrowers except for forgiveness of the loan itself. At this stage of the COVID crisis it is hard to imagine a business that hasn’t been adversely affected by government shutdown orders or that hasn’t implemented new policies based on federal health guidelines. These FTE exceptions have been referred to as “get out of jail free cards” by expert advisors so it is curious that the SBA is so willing to apply this exception to such a broad swath of borrowers with very few mechanisms in place to ensure that borrowers are not claiming the exception in bad faith. After following the evolution of the PPP for months you would have to forgive someone if they came to believe that the SBA and the Treasury have adopted the attitude of “welp, the money has already been allocated. We may as well just forgive as many of these loans as possible.”

As we hurdle to the month of August with no timetable for the much anticipated end of the COVID crisis, now is the time for Congress to come together and finalize the next COVID relief package. We hope that through this arduous process of creating and amending the PPP program, the SBA and the Treasury will have learned some valuable lessons and will be ready to implement an efficient and effective PPP 2.0 sometime in the near future. Until then, stay tuned for future updates.

For Finkel’s Followers

By: David Finkel

Just the other day I was thinking about a business owner that I had coached several years ago. Since he may read this column, I will call him Terrance (not his real name).

Terrance owned a seasonal hospitality business in southern Utah and worked eighty plus hours a week, every year from May through October.

The rest of the year, he “only” had to put in a light fifty-to sixty-hours a week but come May this jumped to twelve to fourteen hours a day, seven days a week.

Now this schedule was hard enough on Terrance physically, but emotionally it was killing him. Can you imagine – every day he got up and left the house before his kids were awake and didn’t get home until his kids were in bed asleep.

Every day… for six months out of the year… year after year after year…

When I first met Terrance and he told me his story, it broke my heart.

I’m a dad with three young sons myself. I’ve experienced how fast their childhood seems to disappear. There are personal milestones in your kids’ lives that you never rewind. I remember how it used to feel when my older two sons would reach for and hold my hand anywhere, we walked together—into a store, on a trail, or even down the stairs to breakfast.

It was one of the sweetest parts of being a dad for me, the feeling of their tiny hands in mine. Then the day arrived when they were about eight years old, and they stopped reaching for my hand. Just thinking about this makes me want to cry.

Of course, it’s normal and healthy—they’re growing up. But I miss it.

So, when Terrance told me about how for years, he sacrificed baseball games, family meals, and bedtime stories with his four kids to take care of his business responsibilities, I really felt for him.

There is good news at the end of his story, though so stay with me.

While there were many ways that he could have worked on his business (much like in your own) I encouraged him to focus on one single idea, and that idea turned his business and his life around.

Question Everything

I challenged Terrance to question each and every task he did for his business.

- Did he really need to do that report, or could someone else within the company put it together for him to review?

- Did he need to be the one to sign the paychecks?

- Did he need to handle every customer complaint, or could someone on his team be trained to handle it properly?

- Did he need to be there for that sales meeting?

And the list went on and on….

What he quickly realized is that the majority of the tasks on his plate, where there simply because he had failed to create systems and controls and delegate tasks to his team. There was just a handful of tasks that should have been on his to-do list, and those where the items that created the most value for his company.

Focus on Fewer, Better

Once he was able to identify where he should be spending his time, he was then able to really create value while still making time for his family. (Which by the way was only around 20 hours a week in the off-season and 35 during the busy season.) He even took his first ever vacation in the middle of the busy season!

I’m hoping that Terrance’s story sparks, inspires, or shakes you up enough that you start to do this same work on your business. The first step is to fundamentally change the way you structure your day, week, quarter, and business environment so that you can achieve incredible professional success and enjoy even richer personal and whole-life success, too.

Today in History and Humor

By: Wesley Dickson

- The first commercial radio station, 8MK, was launched in Detroit on this day 100 years ago.

- For some countries, August 20 is a day of freedom. Senegal broke from the Mali Federation and declared independence on this day in 1960 and Estonia decided to re-establish its independence in 1991.

- However, it also marks a period of restriction. Quebec was not allowed to secede from Canada per a decision of the Supreme Court of Canada brought down on August 20, 1998.

- Benjamin Harrison, the 23rd President of the United States, was born on August 20, 1833. This President Harrison was the grandson of William Henry Harrison, who served as the 9th President of the United States, marking the only time in history a grandfather-grandson duo has held the office.

- August 20, much to the chagrin of every Floridian, is World Mosquito Day. Interestingly enough, mosquitos may be the only creatures whose “day of celebration” calls for extermination as opposed to conservation efforts.

- Hungary was officially established in 1000 A.D. as a Kingdom by Stephen I. I establish that I am hungry most mornings as soon as I wake up.

- Alaska was first spotted on August 20, 1741 by Danish explorer Vitus Bering who was sailing for the Russians. Coincidentally, Russia was first spotted by Alaskan politician Sarah Palin who observed the large country from her house.

- The Dial phone was patented on this day in 1896 and would soon entirely replace the Rotary phone. Individuals with 9s and 0s in their numbers rejoiced.

- The American Professional Football Association was formed on August 20, 1920. This entity, which would eventually become the National Football League (NFL), held its first game on September 26, 1920. The game was very one-sided with the Rock Island Independents beating the St. Paul Ideals 48-0.

- On this day in 1960, the USSR recovers 2 dogs from space marking the first time living organisms had left Earth’s atmosphere and returned alive.

- The Economic Opportunity Act of 1964 was signed into law on August 20, 1964. This act, which was meant to combat the War on Poverty, was passed at a time when the US poverty rate was almost 20% (almost twice what it currently is under COVID quarantining measures).

- In 1964, Yankee’s player Phil Linz plays harmonica on the team’s bus despite Yogi Berra’s orders. Linz, who had a problem with authority, later stole a picnic basket despite Yogi Bear’s orders.

- On August 20, 1991, Dan Marino of the Miami Dolphins became the highest paid NFL player with a 5-year $25 million contract. In 2020, Kansas City Chiefs quarterback Patrick Mahomes broke the record by signing a 12-year $503 million contract. The contract averages Mahomes almost $42 million per year.

- Usain Bolt set the 200m world record (19.30) at the Beijing Olympics on August 20, 2008. Exactly one year later, Bolt would win the Athletics World Championship 200m dash.

Upcoming Events

Gassman, Denicolo & Ketron, P.A.

1245 Court Street

Clearwater, FL 33756

(727) 442-1200