The Thursday Report – 7.20.17 – Stairway to Thursday

Re: Stairway to Thursday

Coordinating Business Conduct: Contractor Relationships and Insurances Part 1 by Chuck Wasson, Scotty Schenck & Alan Gassman

Two Ways That Medical Practices Can be Paid by Medicare—Beyond Fee for Service Billing and Ancillaries Part 1 by Alan Gassman and Scotty Schenck

Negotiating Leases for Your Business and Related Relationships by Alan Gassman and Scotty Schenck

Taxpayers Advocate Services by Stephanie Mas

Why All Appreciated Assets May be Best Owned by Partnership Taxed Entities and Why to Keep Partnerships Owning Securities Separate and Apart From Anything that Would be Identified as a “Trade or Business” by Alan Gassman & Brandon Ketron

The 2704 Regulations Are One Step Closer to Being Dead by Howard Zaritsky

The 3 Questions Every Business Owner Must Ask by David Finkel

Richard Connolly’s World

Humor! (Or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Alan at agassman@gassmanpa.com

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com

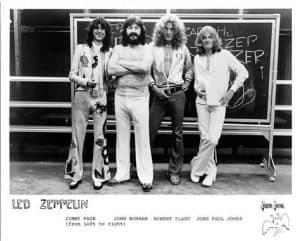

Quote of the Week

“I may not believe in myself, but I believe in what I’m doing.”

-Jimmy Page of Led Zeppelin

At their height, Led Zeppelin were able to cultivate a sense of mystery and fascination unlike most other bands at the time. Drawing on influences from blues, early rock and roll, English folk, and mythology, Led Zeppelin had a unique style of heavy rock that continues to captivate us today. In describing their sound, some tout Jimmy Page as a master of the guitar who had the ability to “sculpture noise” in ways that many have been unable to imitate. “He had a reason for every bit of distortion, feedback, reverberation and out-and-out noise” that was incorporated into the songs.

Led Zeppelin went on to have nearly a decade of success, but when band member Robert Plant’s son passed away the band had to cut their 1977 tour of America short. However, when they resurfaced in 1979 they lacked the same on-stage presence and crowd commanding ability that had once made them so successful.

Looking back, Robert Plant said that he wants “to maintain the dignity of the group. I think that the way that it is now, whatever it was that people loved, is not going to be spoiled. I think the active Led Zeppelin was bold and brave and honest, and it took risks and chances which are no longer possible if you start from scratch. It captured all of the wonderful elements of music to which we’d been exposed. We begged, borrowed and stole and then made something that was particularly original, and by which a lot of other music has been measured. And I’m very proud of people being so enchanted by it.”

In 2016 it was reported that Robert Plant and Jimmy Page were being sued for stealing the opening chords to the 1971 song, Stairway to Heaven, from the song Taurus by the band Spirit. Led Zeppelin ultimately won the copyright suit, but to the untrained ear the similarities between the two songs can be heard. To see a clip comparing the two click here.

Coordinating Business Conduct: Contractor Relationships and Insurances Part 1

by Chuck Wasson, Scotty Schenck & Alan Gassman

Schenck is a senior at Northeastern University studying journalism and applying to law school. He started interning with our law firm on June 20 and has already made a significant contribution. Watch out for this new lawyer on the block who should graduate and pass the bar in 2021.

Chuck Wasson has been active in the insurance industry for over twenty years, starting as an insurance adjuster at Sarasota’s Johns Eastern Company, to his current position as President at ARCW Insurance. Over the years, Chuck has developed a corporate philosophy of understanding that the insurance they sell can be purchased from a number of different agencies or outlets. For that reason alone, ARCW Insurance has strived to be different from the rest by being the one-stop shop for all insurance needs both commercial and personal. Chuck graduated from the University of Florida in 1988 and attained the Chartered Property Casualty Underwriter (CPCU) designation in 1998. In 2007, he was given the designation of Certified Insurance Counselor (CIC).

The title of this article is “Coordinating Business Conduct: Contractor Relationships and Insurances.” That last word – the word “insurances,” is why we’re really here. Insurance is our main topic, and we’ll talk about what lawyers and other professionals need to know about structuring business entities, business conduct, and, of course, the insurance part of it.

Insurance agents can really vary in technical skills, in caring and in effort projected. It can take a lot of work and a lot of research to decide what the best combination of carriers are for a particular situation. That’s why we’re talking to one of the best, Mr. Chuck Wasson.

First, let’s talk about how important it is, any time you look at a business situation or professional practice situation, to see what your risks are and how they are arranged.

We’re sitting with a physician client. We begin by looking at his medical practice situation. We notice there’s a car in the medical practice. If that car is in an accident and the driver is negligent that medical practice could lose all its assets. Why the heck is there a car in a medical practice? Beats me, but I assume they’re not bringing their medical services on a road trip with them. That medical practice could have set up an LLC to own that car and avoided quite a bit of liability.

We also notice the medical practice has two offices. Why isn’t that medical practice two different medical practices? One office does weight loss and one does general practice. Is there a way to keep them separate? There’s somebody who comes in and does a risky type of procedure in either office. That person is paid as an employee. Could we make that person an independent contractor, have patients sign off, and have the contractor pay us rent, but not be responsible for their malpractice? This same type of analysis can go with any kind of business.

For example, imagine we have a client who wants his beautiful acreage on a farm to be used for his friends to go hunting, hiking, and to enjoy themselves. It really is some gorgeous acreage, but what if somebody gets hurt on that property and decides to sue. Well, we’re certainly not going to leave our client in hot water. We’re going to plan for that liability. We’ll have a land owning company with a triple-net lease on the acreage. That company owns the equipment there and some cows, and then when people do use the property for whatever purpose, they’ll have to sue the land owning company and, of course, there are going to be signs on the property pursuant to the Florida statutes. Visitors are going to sign releases, and parents are going to sign releases for their children. We’re also going to have insurance covering everybody because you just can’t be too careful.

Now, we’re going to talk to Chuck Wasson about (1) some different business arrangements that he likes seeing and (2) what sort of coverages we, as advisors, need to be understanding of and what types of lacking in coverage we need to be cognizant of.

Question (Alan Gassman): What should business creators be mindful of when planning for insurance?

Answer (Chuck Wasson): Usually businesses think of insurance agents as a tail-end service, something they get after going through all their planning. But this mentality inverts what should be done, and what good legal representation will advise. Why? Because when you put a business together, when your clients put a business together, you know an insurance agent is integral making sure that the aspects of that business are covered.

There are two types of insurance agents. The first is what we call a “captive agent,” who only represents one company. How is a captive agent supposed to put together a personalized plan for you when he can only consult one insurance carrier?

I am an independent agent. I believe this distribution channel is better than a captive agent. No business is similar to another business. Each of them have their own little quirks and issues that you have to deal with. Now as an independent agent, I’ve got 30 between personal lines and commercial – I’ve got 30+ carriers that I can go to. That’s the kind of flexibility you, as a business, are looking for. Independent agents usually have more latitude in finding and negotiating insurance plans.

A lot of the coverages that we are going to talk about are things that are lacking in an insurance program. No one wants to be paying everything for insurance, and there are ways that you can maybe self-insure on certain things, or take a higher deductible to help lower some costs, but there are certain coverages that you really need to look at.

Question: What can you tell us about Employment Practice Liability insurance policies?

Answer: Employment practice liability is one of the foremost importance. Most people know the coverage that we see in this type of policy—sexual harassment, wrongful termination, and religious discrimination. I also see things where an employee sues the employer because they felt that they should have received a promotion and another colleague received that promotion over them.

Over the past five or six years, I have seen plenty of wage and hourly claims. So much so that insurance companies have had such a bad loss ratio on those, they have kind of paired this coverage back. Here’s an example of this type of claim. You’ve got an employee that says that they worked overtime and they haven’t been paid for the overtime, and you usually see that is in a situation where an employee has been terminated or quit. They go back and say, “Hey, I worked all these overtime hours and I never was paid for it.” In years past, there would be coverage for both the indemnity or the damages portion, plus effects. Because of the amount of claims that we have seen, especially here in Florida, essentially all (I estimate around 95 percent of) carriers have taken the indemnity portion away, and what you are left with is a sub-limit for defense costs only, and we usually see those ranging from $25,000 to about $100,000.

There are still a few carriers that will write the indemnity portion, but there is going to be a substantial premium if you go that route. We suggest that you always at least look at that to see if the particular business is able to get the indemnity portion and what the pricing of those two different options are.

Question: Are employees the only people employers have to worry about in regard to employment practice liability?

Answer: The short answer is no. The ways in which your employees interact with people outside the business can result in third-party exposure, and there are two important aspects to this. The situation that we have seen on these is where you have a front desk person and you have a delivery person that comes in every week to make a routine delivery. They start getting a little friendly with each other, and the employee feels that they are threatened—maybe that delivery person is making some sexual advancements towards the employee, and the employee complains about it, but doesn’t feel like the employer has really protected them or tried to make that situation cease. We have seen those claims.

The other third party we have seen is where a client will come in, or a vendor, and they feel like they have been discriminated for any kind of reason, based on race, religion, sex, and maybe you have a vendor that is trying to come in and do some business and they feel like because of their race or their sex that they are not getting an opportunity and they turn around and they will sue the employer for that kind of situation.

Question: Let’s say my employees use their own cars for work-related errands, or maybe they use a company car. What do I need to be concerned with from a liability standpoint?

Answer: What about that medical practice with the car? Well for them, there’s hired and non-owned auto business insurance. It is amazing that we still see this on policies with the coverage that is not included. Hired and non-owned auto policies cover a corporation for any employee use of their personal vehicles on company time.

Why is that important? Imagine you’ve got an employee who runs to the bank to make a deposit, runs to the supply store, runs out to get lunch for the staff. They get in an accident, and it’s their fault. Generally what happens is that employee is sued, and then through depositions, they find out that the employee was working for the employer. Can you guess what happens next? I can almost guarantee you every single time that the employer is going to be sued as well. And it is another good reason to check the insurance of your employees that make routine use of their own car, check their insurance and make sure they have adequate liability limits.

What else do you need to know about vehicles? Personal versus commercial vehicles, and some of the main differences that we see on it—for one thing, you can take two cars that are the exact same model, exact same make, and if you put one on a commercial policy and one on a personal policy, the commercial policy is always going to be more expensive. The underwriter is going to assume that, because it is a commercial policy, the car will be on the road more and, ergo, have a higher chance of getting into an accident.

Florida right now is probably the loss leader for most insurance companies when it comes to automobile coverage. Everyone is going to see decent rate increases on your auto coverage within the next twelve months. Take Hartford for example, their company would be profitable on auto insurance if they carved Florida out. Florida actually was the loss leader of Hartford in 2016. Why? Gas is cheaper, so people are driving more; we all know people who drive with their phones and not with their eyes: we are getting more distracted drivers; cars are more expensive to repair; and what was a $700 or $800 bumper a couple of years ago is now a $2,000 bumper with cameras and other technology causing the cost of vehicle repairs to rise.

When getting you a commercial auto policy, you must list the permissible drivers—every single driver that could possibly use that vehicle. If you don’t, there is a chance that a claim could be denied. With a personal vehicle, as long as you are a permissive user, and it is on an occasional basis, you don’t have to list drivers. I can give anyone my car, and let them drive it, the insurance is going to follow the vehicle. If it is in an accident, it is going to be on my policy, but I don’t have to list all the drivers on a personal policy. So I stress to all of my commercial clients, whenever you make a change, you have to make sure that the drivers who potentially could use the vehicle are listed on that policy.

There are certain carriers that will allow a corporately-owned vehicle that is titled in a corporation. Sometimes they will allow them a personal policy, it just depends on the carrier. There are probably a handful of insurers out there that will do it, so if your business is in a corporate name and it needs to be on this type of policy, just find a carrier that will let you do that.

Tune in to the next Thursday Report for Part 2!

Two Ways That Medical Practices Can be Paid by Medicare—Beyond Fee for Service Billing and Ancillaries Part 1

by Alan Gassman & Scotty Schenck

We welcome questions comments and any suggestions on this draft article, which is destined to go better places.

Between 2011 and 2015, Medicare released two new ways that medical offices can be paid to help provide good care for patients.

Both methods involve primarily non-physician time and services, and can substantially increase the revenues and quality-of-patient care if handled effectively and efficiently with the relatively large Medicare population.

Chronic Care Management, first instituted in 2015, enables medical practices to earn up to $43 per month by providing an infrastructure to track and be responsive to patients who have two or more chronic conditions that meet the definitions described below.

Annual Wellness Visits, first instituted in 2011, consist of 20 minute or longer patient interviews and discussions with trained, but non-physician practice personnel and pay $172 for the first visit and $111 each year thereafter.

This paper describes the two programs and requirements associated therewith.

Conscientious medical practitioners in many specialties can consider adding these services for patients not receiving them elsewhere, and Medicare patients may begin to become educated and seek the benefits of these services as an enhancement to their otherwise applicable medical care.

Entrepreneurial organizations are gearing up to provide medical practices with protocols, personnel, and other infrastructure, which is permissible so long as patients and referral sources come solely from the practice, and not from such outside consultants.

******************************************************************************

Questions:

(1) What conditions qualify a patient for CCM services? What qualifies a patient for an Annual Wellness Visit?

CCM is afforded when a patient meets all of the following conditions: (i) Multiple (two or more) chronic conditions expected to last at least 12 months, or until death of the patient, (ii) chronic conditions place the patient at significant risk of death, acute exacerbation/decompensation, or functional decline, and (iii) a comprehensive care plan has been established, implemented, revised or monitored. The comprehensive care plan is part of the CCM service itself, and it must be established, implemented, revised, or monitored for a practitioner to bill for a given month. The patient must be made aware of the program and give consent, either written or verbal, to begin CCM services.

Qualifying chronic conditions can include, but are not limited to: Alzheimer’s disease/dementia, arthritis (osteoarthritis/rheumatoid), asthma, atrial fibrillation, autism spectrum disorders, cancer, cardiovascular disease, chronic obstructive pulmonary disease (COPD), depression, diabetes, hypertension, and infectious diseases such as HIV/AIDS.

An Annual Wellness Visit has noticeably fewer requirements and is available to anyone who has had Medicare Part B for at least 12 months. Medicare can only be billed once a year per patient for Annual Wellness Visits.

(2) Who can furnish chronic care management, or CCM, services? Who can bill for CCM services?

CCM services can be furnished by either the billing practitioner or clinical staff “under the direction of the billing practitioner on an ‘incident to’ basis … subject to applicable State law, licensure, and scope of practice.” U.S. Dept. of Health and Human Services, Centers for Medicare & Medicaid Services. Chronic Care Management Services. December 2016.

This means that any of the following three classes of individuals can perform CCM services:

(i) A physician (doctor of medicine or of osteopathy),

(ii) Non-physician practitioner (Medicare guidelines specifically list Physician Assistants, Certified Nurse Midwives, Clinical Nurse Specialists and Nurse Practitioners), or

(iii) Clinical staff directed by a physician or other qualified health care professional. See supra, Definition (7) (“non-physician practitioners and [Qualified Health Care Professional]s are synonymous”).

Billing, according to the Medicare, for chronic care management can be performed by:

(i) Physicians (doctors of medicine or of osteopathy) or

(ii) The following non-physician practitioners: certified nurse midwives, clinical nurse specialists, nurse practitioners, and physician assistants.

Medicare specifically notes that the Chronic Care Management services is not within the scope of practice of limited licensed physicians and practitioners, including clinical psychologists, podiatrists, or dentists. None of these individuals can perform or bill for CCM services in their current capacities.

(3) Who can furnish an Annual Wellness Visit? Who can bill for an Annual Wellness Visit?

According to the Code of Federal Regulations, Annual Wellness Visits can be furnished by any of the following:

(i) A physician (doctor of medicine or of osteopathy), certified nurse midwives, clinical nurse specialists, nurse practitioners, and physician assistants, or

(ii) A medical professional (including health educator, a registered dietician, nutrition professional, or other licensed practitioner) or a team of such professionals working under direct supervision of a physician. See supra, Definitions (5).

In addition, Annual Wellness Visits can be billed by any of the following:

(i) A physician (doctor of medicine or of osteopathy) or

(ii) Other qualified health care professionals (certified nurse midwives, clinical nurse specialists, nurse practitioners, and physician assistants).

(4) Do the individuals/professionals furnishing for CCM services or an Annual Wellness Visit have to be employees of a billing practitioner?

According to the CPT, clinical staff are not required to be directly employed by the practitioner to bill for services. This regulation allows for third-party staff to perform CCM services incident to a practitioner services. There is also nothing barring the same practices regarding Annual Wellness Visits, so long as the third-party staff completing the visits are medical professionals under the direct supervision of a physician.

(5) Does the billing physician/practitioner have to be present in the same suite where CCM services are taking place? And does the billing physician/practitioner have to be present in the same suite where the Annual Wellness Visit is taking place?

For CCM, the billing practitioner does not have to be in the same office while clinical staff are furnishing CCM services.

If an Annual Wellness Visit is being completed by medical professionals under the direction of a billing practitioner, the practitioner would have to be directly supervising, or physically present in the same office suite while the visit is taking place. However, Medicare does not clarify whether the billing practitioner would have to be present if a non-physician practitioner was furnishing the Annual Wellness Visit.

******************************************************************************

Definitions:

(1) Centers for Medicare & Medicaid Services: Herein after “Medicare”, this is the government-funded and -managed health care system in the United States for the elderly (Medicare) and the impoverished (Medicaid). Both Chronic Care Management (CCM) and Annual Wellness Visits fall under the purview of the Centers for Medicare and Medicaid Services.

(2) Chronic Care Management: Also known as CCM, this monthly health care service is available to those with Medicare Part-B, a service available to US citizens or permanent residents (five continuous years) that are also 65 years or older. Patients must have two or more chronic conditions expected to last at least 12 months, or until death. Among other services, medical practices that bill for CCM must manage and update electronic health records for all their CCM patients, create and maintain a “comprehensive care plan;” provide 24/7 access to clinical staff, and coordinating care with home and community-based clinical service providers.

This requires at least “20 minutes of clinical staff time directed by a physician or other qualified health care professional,” and Medicare also assumes “15 minutes of work by the billing practitioner per month.” Medicare states that, in most cases, they believe that “clinical staff services will provide CCM services incident to the services of the billing physician.” As is seen below under (5) General Supervision, Medicare has made a special exception for CCM services to allow clinical staff to furnish services incident to and under the general supervision of the billing physician.

Physicians and billing practitioners use code CPT 99490 each month to earn up to $43 from Medicare. It is important to note that only one practitioner per month can bill for this service for a specific patient, first-come first-serve (or, in this case, first-collect payment).

(3) Complex CCM: This is chronic care management for patients who, in addition to the requirements for traditional CCM services, also have what Medicare calls “[m]oderate or high complexity medical decision making.” That decision making must be done by the billing practitioner. In addition, “60 minutes of clinical staff time” incident to the billing practitioner are necessary for complex CCM billing, as opposed to 20. Billing practitioners use CPT 99487 for a reimbursement of up to $94, and, for every additional 30 minutes of complex CCM services furnished, practitioners can use CPT 99489 for up to $47 for each billing of 99489.

Complex and regular CCM cannot be reported within the same month.

(4) Annual Wellness Visit: This annual health care service is available to those who have been enrolled in Medicare Part-B for at least 12 months. This includes the gathering of personal/family medical history, basic physical measurements (height, weight, BMI, and blood pressure), a Health Risk Assessment (HRA), and advice from the billing practitioner or clinical staff on how to address specific health risks.

(5) Direct Supervision: A direct supervision standard in a medical setting requires that a physician be in the same building as procedures and services are being furnished, and be able to provide assistance, though they do not have to be in the room or personally provide such services. In Florida, direct supervision by a physician requires the physical presence in the same office suite. See Fla. Stat. § 456.053(3)(e) (Defines direct supervision as “a physician who is present in the office suite and immediately available to provide assistance and direction throughout the time services are being performed”). See also Rule 64B8-2.001(1)(a), Florida Administrative Code (“‘Direct supervision’ shall require the physical presence of the supervising licensee on the premises”). This is the level of supervision required for Annual Wellness Visits.

(6) General Supervision: This standard is looser than direct supervision. Traditionally, general supervision means that physical presence is not required, but that the physician is on call and able to be reached by telecommunication if need be. It is defined in the Code of Federal Regulations as “under a physician’s overall direction and control but the physician’s presence is not required during the performance of the procedure.” See 42 C.F.R. § 410.32(3)(I). This is the level of supervision required for chronic care management (CCM) because Medicare made an exception specifically for that service. Typically, incident to services are under direct supervision standard. See Definition (12).

(7 ) Current Procedural Technology: Also known as CPT, this is a set of medical codes that are used to report medical, surgical, and diagnostic procedures and services provided by health care entities and is published by the American Medical Association. This is how physicians record and bill for medical services and procedures. Both CCM and Annual Wellness Visits have their own CPT codes.

(8) Qualified Health Care Professional: Also known as QHP, this is defined by the CPT as “an individual who is qualified by education, training, licensure/regulation (when applicable), and facility privileging (when applicable) who performs a professional service within his/her scope of practice and independently reports that professional service.” E&M Coding: Clear and Simple states that non-physician practitioners and QHPs are synonymous. It defines a non-physician practitioner as “a medical provider who is licensed to bill independently to some extent but is not a physician. Examples are an ARNP, PA, and CNM (synonymous with QHP).”

(9) Clinical Staff: Defined by the Current Procedural Technology as an individual “who works under the supervision of a physician or other qualified health care professional and who is allowed by law, regulation and facility policy to perform or assist in the performance of a specified professional service; but who does not individually report that professional service.”

These individuals are allowed to furnish CCM services under the general supervision of, and incident to the services of a physician or other qualified health care professional. This could allow for video supervision and communication from a physician in some states. As long as state law allows a certain individual to “perform or assist in the performance” of a physician or other qualified health care professional’s work, then they can serve as clinical staff, without the need for a license.

Although the CPT does not set qualifications high, third-party staff providers or physicians employing their own clinical staff need to beware of individuals who are excluded by law from participating in federally-funded health care programs. These individuals include those who have committed the following crimes: Medicare or Medicaid fraud, as well as any other offenses related to the delivery of items or services under Medicare, Medicaid, SCHIP, or other State health care programs; patient abuse or neglect; felony convictions for other health care-related fraud, theft, or other financial misconduct; and felony convictions relating to unlawful manufacture, distribution, prescription, or dispensing of controlled substances. See 42 U.S. Code § 1320a–7(a). Those are mandatory exclusions, but you can also check 42 U.S. Code § 1320a–7(b) for permissive exclusions that the Office of the Inspector General under the U.S. Department of Health and Human Services is allowed to exclude from federally-funded health care systems at any given time. The periods in which individuals are excluded vary, please refer to 42 U.S. Code § 1320a–7(c) for more information.

(10) Medical Professional: This is an individual who is permitted to perform an Annual Wellness Visit “working under the direct supervision of a physician.” Keep in mind that any “health professional,” as defined by the Code of Federal Regulations, can provide Annual Wellness Visits. See 42 C.F.R. § 410.15(a) Definition of Health Professional. However, medical professionals are the lowest-qualified tier of employees who can perform such a service. Medicare says this classification includes “health educators, registered dietitians, nutrition professionals, or other licensed practitioner.” Although this leaves quite a few possibilities open for who can serve such a role, Medicare has put an emphasis on these individuals being licensed and having significant medical/health knowledge.

(11) Billing Practitioner: For the purposes of this memorandum, this is a physician or other qualified health care professional who bills Medicare patients for either CCM services or Annual Wellness Visits.

(12) Incident To Service: This refers to any service that is “furnished incident to physician professional services” that are “part of your patient’s normal course of treatment, during which a physician personally performed an initial service and remains actively involved in the course of treatment.”

Pursuant to Medicare regulations, “incident to” services have a general rule that they be provided under direct supervision. Direct supervision of a physician means that those specialists are present in the same building. Medicare created an exception that allows CCM to be provided under a “general supervision” standard. The physical presence of the billing health care professional (physician or non-physician practitioner) is not needed at the time CCM services are being furnished.

Tune in to the next Thursday Report for Part 2.

Negotiating Leases for Your Business and Related Relationships

by Alan Gassman & Scotty Schenck

What do you need to protect yourself when you’re negotiating a lease? It can seem like a minefield at times, but luckily we have plenty of tips that should help you through the possible (and probable) confusion. These tips came from a webinar that Alan Gassman and Christopher J. Denicolo gave on Tuesday, June 27 as part of the Maui Mastermind lecture series. For a replay click here. The following article was drafted by Scotty Schenck.

When you’re considering buying real estate, or leasing property for your business, go over these steps, think them through and don’t get caught paying more than you have to. Your employees, customers, and wallet will thank you later.

(1) Ponder the financial decision of property as a whole

Often times, investing in real estate or a space for your business is one of the largest financial decisions of your life. It’s important to consider whether you want to select an opulent office space or reap more financial security from spending less on rent/a mortgage and on maintenance. Unless you’re a retailer that will benefit from ultra-prime locales on Main Street, the latter is typically superior.

And don’t be afraid to have a strategical mindset. Shop for less expensive leases from competing landlords and always keep a plan B in mind. Even if you can’t convince your dream location’s landlord to drop his rent, you can go with plan B and save money.

Make sure to check your bases, and involve plenty of professionals to make sure you are getting the agreement you want. Involve CPAs, financial advisors, insurance agents to review required coverages, contractors to assure the quality/condition of the building and fill you in on expected maintenance, and zoning specialists to make sure it’s approved for the type of business you will be doing. If you want to build-out on the property, know what you’re getting into. Be careful with advice from your leasing agent or any entity being paid via commission. Don’t forget to give your psychiatrist or psychotherapist a call while you’re at it.

And lastly, check your formalities. Did you know that a lease in Florida extending beyond a one-year period is not effective unless signed with two witnesses?

(2) Whenever you have a legal document before you, remember the two golden words

Read it! In lease agreements, we often see things that you wouldn’t expect or plan for. But this advice extends to any legal document you’re given to sign. If you can’t read the Lease and even if you do, have your lawyer (or at least a lawyer) read it for you. Make sure they have experience in lease reading/drafting. Read things that you hand others to sign, because you’ll often forget what was in it too. Nothing is worse then finding out there was an exception or clause that will cost you money in certain circumstances, or lose your business.

Never be afraid to ask for clarity; your financial future may depend on it.

(3) Who are you leasing with?

Don’t sign with bullies. Only contract with good people, whether you’re a landlord or a tenant. It’s a big demerit to have a landlord who is a shady person or a liar. Do a background check on the landlord or organization you’re leasing with.

(4) Do you know your options for limiting liability?

Limiting guarantees limit your liability to the landlord in case of unforeseen circumstances. Imagine your employee accidentally burns down your office building. Who’s going to pay for that? Unless you have limiting guarantees, it might be you as a business owner. It will be significantly simpler and less dreadful to limit your guarantees in some way. And here are three ways to do just that: (i) limit your liability to a percentage of excess liability, (ii) limit it to a specific dollar amount, or (iii) limit it to a specific amount of time—for example, “only for defaults occurring in the first X amount of years under the Lease, and thereafter not exceeding $50,000.”

You can also give yourself a safety valve in the Lease by creating a buy-out clause, where before a certain period, say 180 days, you can buy your way out of a lease by paying some percentage of the rent. Landlords might too want a buy-out clause to get rid of a tenant as well.

Yet another way to limit liability is to separate your business locations into their own companies to minimize the risk of liability spreading from one to another. If one store front goes under or is facing litigation, you won’t lose everything.

(5) Is location everything?

Remember the late-2000s and the recession. Business owners who had modest fixed expenses did not face as much damage as others. Business owners who went over their head with opulent business locations were often hit the hardest.

Location preference often butts its head with lower overhead and being able to move the money not spent on pricey rent towards advertising. Think about what you’re paying in rent. Is it better for you to buy the whole building? If you decide to close down early, you can sell the building and avoid paying 3-5 years of rent. It’s not the right decision for every business owner, but it is something to consider. Is it better for tax purposes for you to pay higher rent but let the landlord do build-outs? You could also put the build-out under a separate company.

(6) The Terms of the Arrangement

Would you rather have a two year lease with four, two-year options to extend or a five year lease with one, five-year option? To me, the answer is simple. I would rather have more options and be able to consider where I am every two years. But you do need to be careful about the changes that can occur. Will the Lease terms be identical? Will there be an allowance for refurbishing? And, will the rent be fixed, change with CPI, or be based on the market at the time?

Your financial destiny may very well depend on exercising your option to extend the Lease on time. Do not forget to exercise it! The option extends until the Landlord writes you a letter reminding you that you haven’t exercised your extension.

Further, ask for free rent. It will give you time to figure things out, to inspect, and to open your business. You can also ask for more free rent when you extend your options in the future.

(7) Negotiation with rent and common area maintenance, are you getting a good deal?

When trying to negotiate, common area maintenance is one of the easiest places to see landlords make concessions. It can also be a place for them to sting tenants. There have been some instances where we’ve seen landlords get a percentage of the common area maintenance just for maintaining it. They can also charge exorbitant prices, or even get you paying for costly repairs you never expected.

One way to combat this is by setting a dollar-amount ceiling for how much you are willing to pay for common area maintenance, or you could put into writing that you are not required to pay any more than the other tenants.

Also, ask for the right to reduce rent if other tenants pay less later in their leases.

Further, when calculating total square footage, and checking the square footage discussed in the Lease, make sure that it is the total usable space. You can also add a clause your rent will go down if the square footage is inaccurate.

(8) What can you do to lower liability on your lease?

You can lower the liability of your agreement to a specific dollar amount, such as no more than $50,000, or by month, such as $4,000 per month for each month left in the lease if there is an early termination. And don’t forget about catastrophic liability issues, such as fires.

Imagine a rancher is trying to limit his liability when he leases land to a tenant by leasing through a ranch operating company. You can put an 80 percent mortgage on that ranch company, owed to the rancher’s family limited partnership. If the rancher gets sued for any reason by the tenant, he can only lose 20 percent equity and not the whole value of the property. In conjunction, the lease could be triple net leased from the company to the operating company and then the operating company can sublease where the tenant will agree only to look to the ranch operating company if there is an injury. Such an arrangement will hold up in many states.

(9) What type of agreements is your landlord trying to get you to sign?

There are three types of agreements that we suggest you get. First is the memorandum of lease. In Florida, a memorandum of lease requires two witnesses and a notary public to be recorded. And that is, of course, in addition to the witnesses you need to draw up a lease of greater than one year. Second is the subordination/attornment agreements, where the bank mortgage is superior to the Lease and allows the bank to step in if the Landlord defaults. Non-Disturbance agreements will allow you to continue operating your business/occupying the property even if the bank has foreclosed it.

Lastly, you should always ask for rights of first refusal. This will give you the ability to negotiate/refuse an extension on the Lease if there is no set option. With a right of first refusal to an adjacent space, the Landlord cannot sell or lease that adjacent space without offering it to you first. And you can also get a right of first refusal to purchase the entire building.

(10) What other amenities should I be concerned about?

When purchasing a place for business, parking and signage plays a huge role. The best option is to have reserved parking with the right to put up signs. We have seen people end up with zero parking spaces. You should also ask for as much signage as other tenants. However, be careful to know the limitations placed on signage by your municipality (such as banning lights on signs at night to prevent light pollution).

Other amenities can be just as important, such as handicap parking, medical waste pickup access, and antennas on your roof. Again, don’t be afraid to ask or get it in writing.

(11) Conditions and repairs

The opposite of the golden words, “read it,” are the two worst words, “as is.” This means there are no warranties as to the condition of the space or office. When you see these words it should send a red flag in your mind to get an inspector if you are seriously considering a property.

Like with common area maintenance, repair liability can also be minimized by adding provisions into a lease agreement. But remember when language is vague, ties usually go to the Landlord. Further, require your landlord to keep the common areas in first-class condition, as well as maintaining quiet enjoyment rights to prevent noxious uses of the building and its immediate surrounding. If a landlord owns the properties around your potential businesses space, get it in writing that other businesses like yours and that will detract from your business (think bars or a children’s play center) are not allowed.

******************************************************************************

Don’t forget that you should always ask to get what you agree on in writing, ask for more rights and liability reduction, and always read what you sign (or better, have a lawyer do it!)

Moral of the story: You can’t get what you don’t ask for!

Taxpayers Advocate Services

by Stephanie Mas

The Taxpayers Advocate Service (TAS) is an “independent organization within the IRS” that reports directly back to the National Taxpayer Advocate, and acts as, “Your Voice at the IRS.”[1] Their goal is to help taxpayers whose unresolved tax problems are causing financial difficulty by providing “free, confidential, and personalized services.”[2] The main categories of cases the TAS accepts are:

- “Time-sensitive matters.

- Issues involving multiple IRS units.

- Breakdowns in the IRS’s normal process.

- Situations in which a taxpayer has a unique circumstance[ ], but the IRS is applying a ‘one-size-fits-all’ rule.”[3]

TAS helps both the individual taxpayer through their IRS issues, and also helps the masses of taxpayers by identifying IRS procedural problems and recommending steps to correct the problem.[4] The National Taxpayer Advocate, in turn, presents Congress with an Annual Report identifying the most serious problems facing taxpayers.[5]

When preparing to speak with a TAS representative, you will need to have the following information readily available:

- “The Social Security Number (SSN) or Employer Identification Number (EIN).

- The tax year(s) and type(s) of tax returns involved.

- A detailed description of [the] dispute.

- Information about [the] previous attempts to resolve the problem.”[6]

Additionally, to receive tax help from TAS, participants must fill out and file an IRS Tax Form 911 (Request for Taxpayer Advocate Service Assistance, and Application for Taxpayer Assistance Order) by either going to the IRS website click here or having an IRS employee complete the 911 form for them.

TAS has offices in every state. To receive face-to-face assistance from TAS, a two-way video conference can be held in Tampa at the IRS Taxpayer Assistance Center between 8:30 a.m. – 4:00 p.m. at 3848 W Columbus Drive, Tampa, FL.[7]

Alternatively, TAS can be contacted in Florida by calling either 1-877-777-4778, or by contacting a specific office directly, as follows:[8]

- Ft. Lauderdale: Address- 7850 SW 6th CT., Room 265, Plantation, FL 33324

Phone- 954-423-7677 Fax- 855-822-2208 - Jacksonville: Address- 400 West Bay Street, Room 535A, MSTAS, Jacksonville, FL 32202

Phone-904-665-1000 Fax-855-822-3414 - St. Petersburg: Address- 9450 Koger Blvd, St Petersburg, FL 33702

Phone- 727-318-6178 Fax- 855-804-3430

*********************************

[1] The Taxpayer Advocate Service is Your Voice at the IRS, Taxpayer Advocate (Oct. 19, 2016), https://www.irs.gov/advocate/the-taxpayer-advocate-service-is-your-voice-at-the-irs.

[2] Taxpayer Advocate Service, Investopedia, http://www.investopedia.com/terms/t/taxpayer-advocate-service.asp.

[3] How can the Taxpayer Advocate Service Help Me?, TurboTax (2016), https://turbotax.intuit.com/tax-tools/tax-tips/Taxes-101/How-Can-the-Taxpayer-Advocate-Service-Help-Me-/INF28732.html.

[4] The Taxpayer Advocate Service is Your Voice at the IRS: Who We Are. Taxpayer Advocate (Oct. 19, 2016), https://www.irs.gov/about/who-we-are.

[5] Id.

[6] Resolving Tax Problems May Be Easier Than You Think. US Tax Center. https://www.irs.com/articles/resolving-tax-problems-may-be-easier-you-think.

[7] Contact Your Local Taxpayer Advocate, IRS.gov, https://www.irs.gov/advocate/local-taxpayer-advocate#Florida.

[8] Id.

The authors wish to thank Jerry Hesch for his comments and help in improving the following article which was first published in the last Thursday Report.

A Jerry Heschified Version of Our Evolving Article on Why All Appreciated Assets May be Best Owned by Partnership Taxed Entities and Why to Keep Partnerships Owning Securities Separate and Apart From Anything that Would be Identified as a “Trade or Business”

by Alan Gassman & Brandon Ketron

We thank Jerry Hesch for the important reminder shown below with underlined language.

Recent white papers and presentations in the tax and estate planning community have brought to light that the partnership tax law may allow for basis in one partnership asset to be shifted to another partnership asset before sale in order to defer or avoid capital gains taxes, depreciation recapture and other types of income that must normally be realized on sale or disposition of an asset.

Readers who are not familiar with this concept, or who have not understood its basic application, can benefit from reading the following example, which is also illustrated by exhibits available from the authors.

Grandpa owns 45% of a partnership and has a $5,000 basis in his partnership interest, Son 1 owns 45% of the partnership with a $1,000,000 basis, and Son 2 owns 10% of the partnership with a $222,222 basis. The partnership owns a building that Grandpa put in after it was almost fully depreciated worth $1,000,000, bonds that Son 1 put in worth $1,000,000 with a $1,000,000 basis, and $222,222 of cash that Son 2 put in. The partnership has made what is called a 754 election to cause basis adjustments as below described, and the property has been in the partnership for at least 7 years.

Assume that the partnership has a contract to sell the building for $1,000,000 and first distributes the building to Son 1 in liquidation of his 45% of his ownership interest. When Son 1, with a $1,000,000 outside basis in the partnership, receives an asset in exchange for his partnership interest, Son 1’s basis in the exchanged asset is equal to his 1,000,000 outside basis in the partnership. As a result, Son 1 receives a $1,000,000 basis in the building and can sell it and pay no capital gains tax.

As a result of the above basis shift the bond portfolio basis of the partnership moves from 1,000,000 to $5,000 and Grandpa owns 81.82% of the partnership and Son 2 owns 18.18% of the partnership.

When Grandpa dies his partnership interest basis goes to fair market value and this also increases the partnership’s basis in the bonds.

This has saved income tax on depreciation recapture and capital gains on $1,000,000!

It is important to note that unless the partnership is considered an investment partnership, as discussed in more detail below, IRC §731(c) treats marketable securities as cash when distributed from the partnership, triggering capital gains to the extent the distribution exceeds the partner’s outside basis in the partnership. An investment partnership is a partnership that has never been engaged in a trade or business and 90% or more of the partnership’s assets consist of investment type assets (i.e. stocks, bonds, cash, foreign currencies, commodities, etc.). Therefore, assuming that the partnership in the above example is not an investment partnership the distribution of bonds to a partner would trigger capital gains to the extent that the distribution exceeded the partner’s basis. For example, if bonds worth $100,000 were distributed to Grandpa prior to his death, Grandpa would have a capital gain of $95,000 ($100,000 – $5,000).

What if instead of the above there is a partnership owning only the building and cash, with Grandpa owning 90% and an S corporation owning 10%. Grandpa’s basis is still only $5,000. The partnership has made a 754 election and has owned the building for over 7years.

Grandpa asks his tax advisor what to do when he wants to sell the building, and wants to use the above technique. How can he get another asset into the partnership and another partner with a high basis to facilitate the planning described above?

If Son 1 happens to have $1,000,000 of bonds that cost him $1,000,000 then he can contribute the bonds to the partnership and after waiting for at least two years in order to avoid the disguised sale rules of IRC Section 707, Son 1 may receive the building in the same manner as described above with the same result.

What if Son 1 doesn’t have these bonds but has good credit? Son 1 may arrange to guarantee a loan to borrow $1,000,000 from a bank to buy $1,000,000 of bonds in the name of the partnership, and Son 1 will agree to be responsible for the $1,000,000 loan. As a result of this, Son 1 has a $1,000,000 basis in the partnership and the partnership has a $1,000,000 basis in the assets.

After waiting two years, Son 1 can receive the building in liquidation of his partnership interest with a $1,000,000 basis, sell it for $1,000,000 and recognize no gain. Son 1 can then pay off the loan, and Grandpa can own 90% of the partnership and his estate and the partnership will receive a stepped up basis when he dies.

As the result of the above, and also for the reasons described below, it is arguable that almost any appreciated asset owned by a family member should be owned by an entity that can be taxed as a partnership so that this type of planning can be implemented.

For example, if Grandpa has stocks worth $1,000,000 with a basis of $5,000 and needs to sell these over time to pay for living expenses, the same technique can be used if Son 1 can contribute $1,000,000 worth of assets to the partnership with a basis of $1,000,000.

In addition to the above benefits, it may be necessary in the future to recommend that senior family members own high basis assets, so as to not be subject to tax on death if the US adopts a “deemed sale on death” capital gains tax like Canada has. Until then Grandpa would want to own the low basis assets or partnership interests to get a step up on death.

By keeping both low and high basis assets in partnerships like the one described above, the family can shift basis to Grandpa or away from Grandpa based upon what the tax law and preferred family planning situation is in the future.

By putting the assets into partnerships now, the family enhances the chances of being grandfathered if the tax laws ever change to prevent this type of planning. Presently no known IRS initiative or effort exists to prevent this type of planning.

In addition to the above, LLC’s and Limited Partnerships provide many other benefits, including creditor protection, management opportunities, and valuation discounts to avoid estate tax if needed. Where valuation discounts are not needed for estate tax purposes it can be important to give each partner a “put right” so that on death the valuation of the partnership interest held can be the value of the underlying assets multiplied by the percentage of ownership.

Where different classifications of assets are owned by a family, it will often be advisable to have separate assets in separate partnerships for both tax and state law planning purposes.

As the result of the above, advisors should consider looking at assets and the basis thereof and determining how to be sure that appreciated or hopefully appreciating assets will be under a partnership for at least 7 years when the time may come to sell them.

The above strategy can also work for partnerships that own appreciated stocks and/or mutual funds. It is very important that any partnership owning stocks not be engaged in an active trade or business to avoid what is known as the 731(c) rule. This rule treats marketable securities as cash and requires gain recognition on distributions in which the fair market value of the distributed asset(s) exceed the partner’s outside basis in the partnership. This rule does not apply if the partnership is considered an investment partnership under 731(c)(3)(C). This is why there will normally be separate partnerships for buildings and other active assets and stocks and other passive assets. 731(c)(3)(c) will also apply to the ownership of stock in non S corporations.

Even if the partnership distribution did not meet one of the exceptions to 731(c) the result of the above examples would not change and no gain would be recognized due to the fact that the partner did not receive marketable securities or cash in excess of his outside basis in the partnership.

Unfortunately S corporation stock cannot be owned by an entity taxed as a partnership, so this technique will not work for S corporation stock.

The authors thank Paul Lee of Northern Trust and Jerry Hesch for their thorough and skillful analysis, white papers and lectures on this topic, and on other topics in the estate and tax area.

Special Notre Dame Announcement

Please click here to see the amazing Notre Dame Tax and Estate Planning Institute schedule for the dates in 2017 in South Bend, Indiana. This starts with a late Wednesday 2-hour presentation on what you need to know about bankruptcy law, and wraps up late Friday, followed by the Fighting Irish of Notre Dame vs. NC State on Saturday the 28th.

The DoubleTree hotel adjoins the convention center, and the Thursday evening cocktail reception that is held there should not be missed. We’ll buy drinks after the Wednesday presentation for anyone who mentions the Thursday Report at the DoubleTree bar

The 2704 Regulations Are One Step Closer to Being Dead

Pirated from Howard Zaritsky, without permission, but with due credit and gratitude.

Notice 2017-38, the IRS classified the proposed § 2704 Regulations promulgated under the Obama Administration as overly burdensome. Howard Zaritsky provided the following thoughts on the effect of this Notice in a blog post on the Interactive Legal Website. Some highlights are paraphrased below, and the full blog post can be found by clicking here, but it is not clear whether he was talking about the IRS or his mother-in-law.

Recently, the Internal Revenue Service issued Notice 2017-38, which identifies certain tax regulations that either impose an undue financial burden on taxpayers, and/or add excessive complexity to the tax system.

One section of particular interest for estate planners is IRC § 2704 and its proposed regulations concerning estate and gift taxes. We are likely to see an expansion of the scope of these rules as they apply to transfers of limited partnership interests, non-managing membership interests, and non-voting stock.

We will have to wait for the Treasury to determine how they will make these proposed regulations less burdensome, but as Howard suggests, “it seems reasonable to expect that the regulations will be finalized, but in a form that will be far less problematic for estate planners.”

The 3 Questions Every Business Owner Must Ask

by David Finkel

David Finkel, Wall Street Journal bestselling author of, Scale:

Seven Proven Principles to Grow Your Business and Get Your Life

Have you ever found yourself wanting to grow your business, but holding yourself back because you were afraid you’d have to sacrifice your life to do it?

Feeling as if your only two choices were to grow the business by working harder, longer hours, or to settle for less but at least get some of your time back?

I know I used to feel that way.

In fact, I can remember journaling back in 2001 about how hard it felt like I was working, and how close I was to burning out.

At that time I was working 70 hours a week, and on the road teaching workshops 10 days a month. I loved the way the business was succeeding, but I hating feeling like if I ever stopped running on the treadmill the whole thing would come crashing down.

Plus, as we grew, it felt like I was just adding to my overhead and responsibilities, all of which just increased the pressure I felt.

It was right at this time in my life that one of my business mentors asked me three questions that changed my business perspective forever. I want to share these three questions with you in the hopes that they jar you into seeing your choices fresh.

Question One: “David, what is it that you really want?”

I told him that I really wanted the business to continue growing, but not to feel like it was all up to me to drive that growth. I shared that I felt proud of the impact our company was having on the lives of our clients and their families, but that the pressure was smothering me.

To read the rest of this article click here.

Richard Connolly’s World

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature some of Richard’s recommendations with links to the articles.

This week, the article of interest is “Estate of Powell: Is Its Bark Worse than Its Bite for Family Limited Partnerships?” by Greenberg Traurig. This article was featured on July 13, 2017 in The WRMarketplace.

Richard’s description is as follows:

“The recent decision in the U.S. Tax Court case of Estate of Powell v. Commissioner, reviewed by 17 Tax Court judges, involved “deathbed” tax planning using an FLP, and resulted in inclusion of the FLP’s value in the decedent’s estate.

Advisors should take note of Powell and understand its lessons for avoiding overly-aggressive, poorly-structured FLP plans. But how much should the decision really change the best practices for FLP planning? Perhaps not as much as one may think.”

To View the Full Article Click Here.

Humor! (Or lack thereof!)

Ron Ross In the News

ACTOR WHO DID VOICE OF KERMIT FIRED FROM SESAME STREET FOR “MAKING THE FROG BITTER”. HIS RESPONSE: “I added arugula and turmeric. I got tired of people saying it tasted like chicken.”

…………………………………………………………………………………………..

DONALD TRUMP JR. FORCED TO ADMIT HE MET WITH HANK WILLIAMS JR., DALE EARNHART JR., AND CARLS JR. “It’s just a support group for people making futile attempts to get Dad’s attention.”

…………………………………………………………………………………………..

THE NEW “DR. WHO” WILL BE PLAYED BY A WOMAN. THE ACTRESS, JODIE WHITTAKER, WILL NOT BE ALLOWED TO USE BATHROOMS IN NORTH CAROLINA.

…………………………………………………………………………………………..

Upcoming Seminars and Webinars

Calendar of Events

| EVENT | DATE/TIME | LOCATION | DESCRIPTION | REGISTRATION | FLYER |

| Newly scheduled talks appear in red | |||||

| Monthly Business Law Webinar with Alan Gassman and Friends | Tuesday, July 25th, 2017 at 12:30 P.M. | Gotowebinar.com | Creditor Protection Planning for the Professional Practice or Operating Business | Click Here | |

| Panel Discussion | Wednesday, August 9th, 2017 | Panel Discussion on where estate planning is headed with Jonathan Blattmachr, Marty Shenkman, Alan Gassman, and others | Contact:

Jason@gassmanpa.com |

||

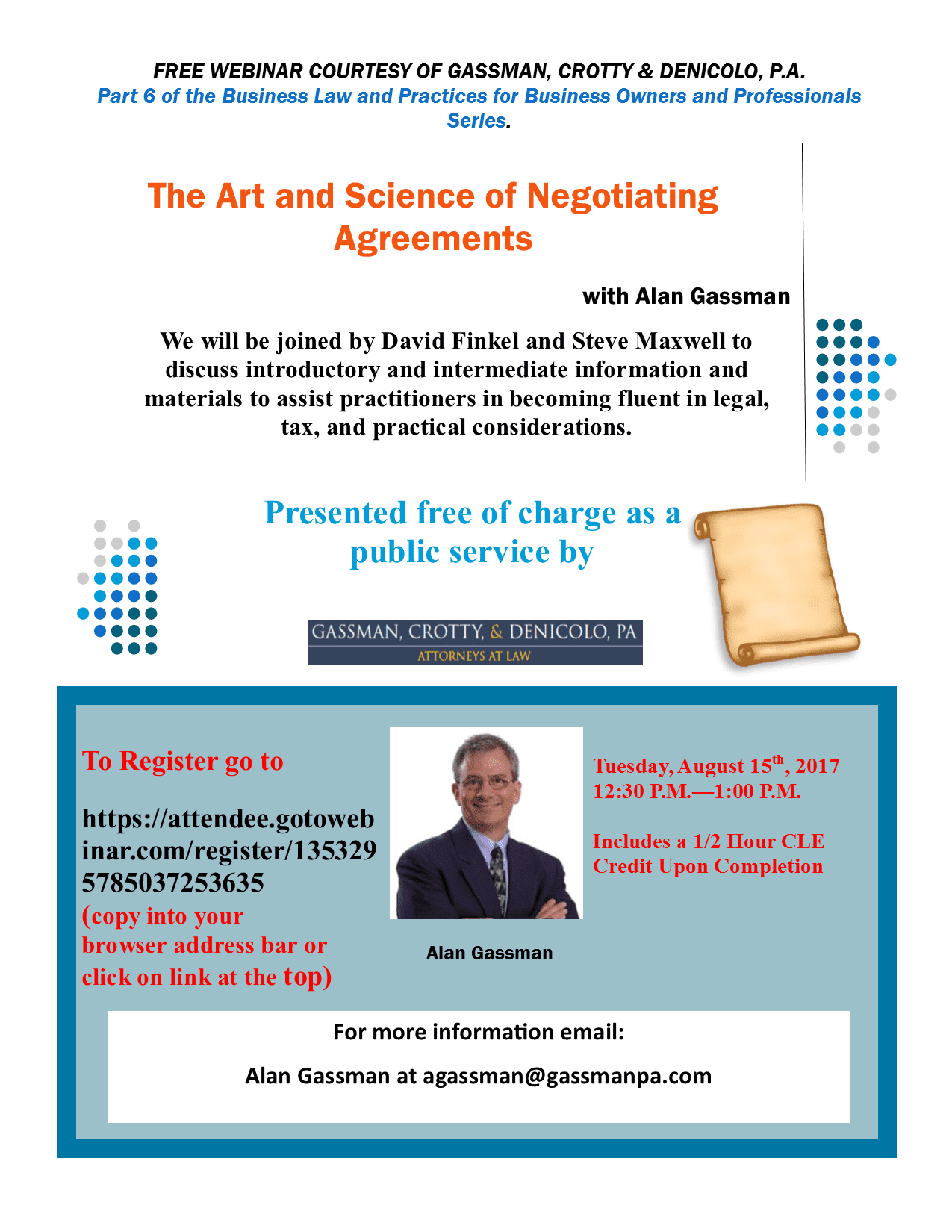

| Monthly Business Law Webinar with Alan Gassman and Friends | Tuesday, August 15th, 2017 at 12:30 P.M. | Gotowebinar.com | The Art and Science of Negotiating Agreements with David Finkel and Steve Maxwell | Click Here | Click Here |

| Marty Shenkman and Alan Gassman on the Asset Protection Continuum | Monday, August 21, 2017 at 4:00 P.M. | Johns Hopkins All Children’s Education & Conference Center-701 4th St S, St. Petersburg, FL 33701 | Hot Topics in Asset Protection

Financial & Estate Planning for Chronic Illness |

Contact:

Jason@gassmanpa.com |

Click Here |

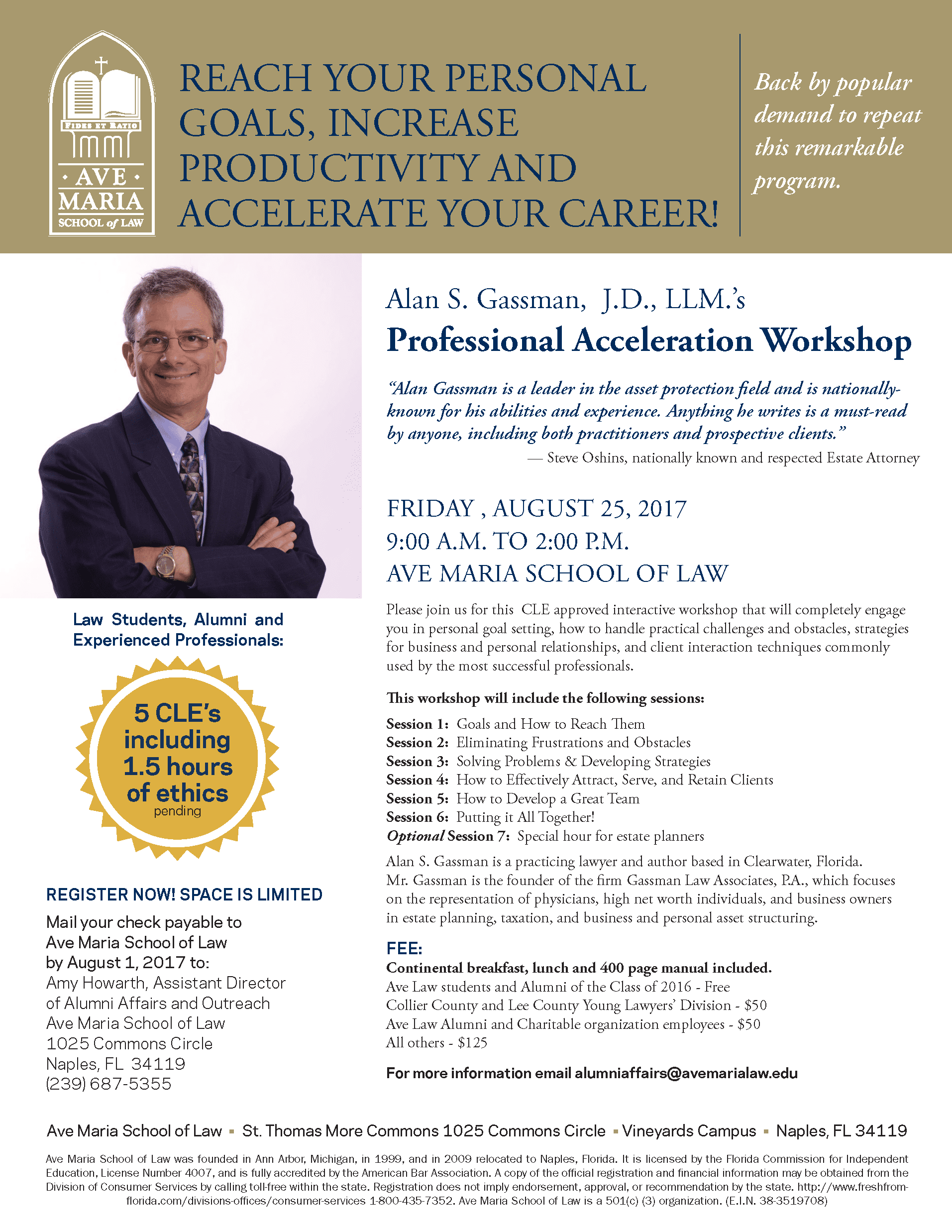

| Professional Acceleration Workshop at Ave Maria School of Law | Friday, August 25, 2017 | 9AM – 2PM | Ave Maria School of Law – St. Thomas More Commons – 1025 Commons Circle-Vineyards Campus, Naples, FL 34119 | Be even more successful with this constructive workshop for professionals. | Contact:

Jason@gassmanpa.com |

Click Here |

| Nebraska Medical Association’s Annual Meeting | Friday, September 8, 2017 | 1:30 p.m. & 4:30 p.m. | Lincoln, Nebraska-Exact Location TBD | Top 10 Mistakes Physicians Make with Investments/Business & Lawsuits 101 | Contact:

Jason@gassmanpa.com |

Click Here |

| New Port Richey Charitable Consortium | Thursday, September 14, 2017 | 12:00 p.m. | Spartan Manor 6121 Massachusetts Avenue, New Port Richey, FL 34653 | Dynamic Estate Planning and Asset Protection Strategies for the Conscientious Planner, with Discussion of Recent Events | Contact:

Jason@gassmanpa.com |

|

| Estate Planning Council of Northeast Florida | Tuesday, September 19, 2017 | Epping Forest Yacht Club, Jacksonville, FL | Enjoy a dinner conference for the Estate Planning Council of Northeast Florida | Contact:

Jason@gassmanpa.com |

|

| Maui Mastermind Hot Seat Session-Moderated by David Finkel | Thursday, September 21st from 1 P.M – 2 P.M. | Gotowebinar.com | Business Law Hot Seat Sessions: A Moderated Q&A Session to Get help on Your Most Pressing Business Law Questions |

To submit questions for the Hot Seat sessions, please send to lawquestions@mauimastermind.com at least 2-3 days ahead of time |

|

| Monthly Business Law Webinar with Alan Gassman and Friends | Tuesday, September 26th, 2017 at 12:30 P.M. | Gotowebinar.com | Negotiating the Purchase and Sale of a Business with John McDonald of Hyde Park Capital | Click Here | |

| FICPA – Fort Lauderdale | Wednesday, September 27, 2017 1 – 3 PM | Ft. Lauderdale – Exact Location TBD | Tax and Associated Planning for Asset Protection Situations

Dynamic Trust Planning

|

Contact:

Jason@gassmanpa.com |

Click Here |

| Naples Estate Planning Council | Friday, October 13th, 2017 – 8 A.M. – 5 P.M. | Naples-Exact Location TBD | IRA Planning with Trusts, Minimum Distributions, and Associated Topics – How to Learn the Rules and Use Them Expeditiously | Contact:

Jason@gassmanpa.com |

|

| The Jewish Federation of Sarasota-Manatee Luncheon with Prof. Jerry Hesch | Friday, October 17th, 2017 – 12PM – 1 PM | Klingenstein Jewish Center – 580 McIntosh Rd, Sarasota, FL 34232 | Innovative Charitable Giving Techniques for the Well-Tuned Estate Planner

Jerry Hesch as sole speaker |

Contact:

Jason@gassmanpa.com |

|

| The Jewish Federation of Sarasota-Manatee with Prof. Jerry Hesch | Friday, October 17th, 2017 – 4 PM – 6 PM | Klingenstein Jewish Center – 580 McIntosh Rd, Sarasota, FL 34232 | Alan will be presenting on Asset Protection Planning & Hot Topics

Jerry will be presenting on Charitable Planning |

Contact:

Jason@gassmanpa.com |

Click Here |

| 2017 MER Continuing Education Program Talks For Physicians | October 20th – October 22nd, 2017 | New York, New York | The 10 Biggest Mistakes Physicians Make in Their Investments and Business Planning,

Lawsuits 101, 50 Ways to Leave Your Overhead, Essential Creditor Protection and Retirement Planning Considerations |

Contact:

Jason@gassmanpa.com |

Click Here |

| 42nd Annual Notre Dame Tax & Estate Planning Institute | Wednesday, October 26th, 2017 3PM – 5PM | University of Notre Dame | What Estate Planners Need to Know About Bankruptcy (2 Hour Presentation) | Contact:

Jason@gassmanpa.com |

|

| Monthly Business Law Webinar with Alan Gassman and Friends | Tuesday, October 31st, 2017 at 12:30 P.M. | Gotowebinar.com | Choice of Entity and Multiple Entity Structures | Click Here | |

| Monthly Business Law Webinar with Alan Gassman and Friends | Tuesday, November 21st, 2017 at 12:30 P.M. | Gotowebinar.com | Uses and Abuses of Independent Contractor Agreements | Click Here | Click Here |

| Monthly Business Law Webinar with Alan Gassman and Friends | Tuesday, December 19th, 2017 at 12:30 P.M. | Gotowebinar.com | Income Tax Strategies and Compliance Aspects of Business Planning | Click Here | Click Here |

| 5th Annual Estate Planning Symposium | Tuesday, February 6th, 2018 | University of Miami | Sponsored by The Estate Planning Council of Greater Miami

Asset Protection for Business Owners and Their Entities |

Contact:

Jason@gassmanpa.com |

Click Here |

| Estate Planning Council of Northeast Florida | Tuesday, March 20, 2018 | Jacksonville, FL | Dynamic Planning Strategies For The Successful Client | Contact:

Jason@gassmanpa.com |

|

| 2017 MER Continuing Education Program Talks For Physicians | November 30th – December 3rd, 2017 | Nassau, Bahamas- Atlantis Hotel | Paradise Beach Drive, Paradise Island, Bahamas | The 10 Biggest Mistakes Physicians Make in Their Investments and Business Planning,

Lawsuits 101, 50 Ways to Leave Your Overhead, Essential Creditor Protection and Retirement Planning Considerations |

Contact:

Jason@gassmanpa.com |

|

| 2018 MER Continuing Education Program Talks For Physicians | Thursday, May 17 – 20, 2018 | Nassau, Bahamas – Atlantis Paradise Island Resort | Alan will be speaking at the Medical Education Resources (MER) event | Contact:

Jason@gassmanpa.com |

|

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}