The Thursday Report – 7.10.14 – Congress Quacks and Ludwig von Duck

Qualifying Longevity Annuity Contracts (QLAC)

What Estate Planning and Other Lawyers Need to Know About Bankruptcy, an article by Alberto F. Gomez and Alan S. Gassman – Part 1 of 3

“The IRS ‘Madoff’ with My Estate!”

Thoughtful Corner – How to Help a Client Express What They Want for Children Who May Have Mental, Addiction, or Similar Issues

Humor! (or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Qualifying Longevity Annuity Contracts (QLAC)

The $125,000 question:

Should your clients over age 70 ½ reduce their IRA minimum distributions by investing in specially designed annuity products?

Introduction:

The insurance industry received a July 4th gift from the Internal Revenue Service in the form of a new regulation released on July 1, 2014 that makes it possible to place IRA and pension plan investments into fixed annuities that will enable the IRA holder or plan participant to avoid the minimum distribution rules that apply after age 70 ½ to the extent that IRA or plan assets are held under such vehicles. The maximum amount that can be invested in such fixed annuities under an IRA or pension will be the lesser of $125,000 or 25% of the value of the pension or IRA account as of the time of the investment. Basically, the value of such contracts will not be considered to be assets of the IRA or pension for purposes of the minimum distribution rules until the owner is age 85.

None of the life insurance or annuity companies have released their products as of yet.

These rules will also allow QLAC’s to be held under 403(b), and 457(b) plans, but not under defined benefit plans or Roth IRA’s.

Under the regulations, these annuity contracts will not be variable or equity indexed annuities, even if they offer a guaranteed minimum rate of return, unless or until explicitly approved by the Internal Revenue Service. Instead, the products available will be ones with a fixed rate of return, life payment, or other similar contract that can be expected to guarantee a minimum rate of return, and to actually credit a slightly higher rate of return in the same manner that many whole life insurance products now offer. The preamble to the new regulations point out that variable and equity indexed annuities with contractual guarantees provide an unpredictable level of income to the holder, and they are inconsistent with the purpose of the new regulation.

A typical arrangement would be that a taxpayer would invest $125,000 (the maximum that can be invested is the lesser of 25% of the value of the qualified account at the time of the investment or $125,000) into a deferred income annuity contract that would pay-out upon the earlier of the death of the account holder or planned participant or ratably from ages 85-90.

One very knowledgeable advisor, Michael Morrissey of Vanguard’s annuity division, gave us the following example of how a hypothetical QLAC might perform.

If a 65 year old male wants to receive monthly income of $1,000 from his IRA after the age of 80, put $47,920 into an annuity contract under his IRA, and the value of the annuity contract would not be subject to the Required Minimum Distribution rules on the value of his IRA until reaching age 80. The contract could allow access to receive payments earlier, if and when needed, based upon the terms of the contract.

The new regulations require that payments from a QLAC must begin to be made by age 85. Therefore, if a 65 year old man wants to receive $1,000 a month for life beginning at age 85, he would only have to put $26,634 into a Vanguard life annuity contract, and would receive a guaranteed payment for life beginning at age 85.

In both of the above arrangements there is a death benefit, as is permitted under the new regulations, which will provide that if the account holder dies before receiving payments equal to the amount invested, then the deficit amount will be paid into the IRA (typically without interest) shortly after death, or payments might continue for the lifetime of a surviving spouse who could roll the annuity over to his or her own IRA and continue to have the benefit of payment rights.

There will doubtless be interaction and confusion between these rules and the “stretch trust” minimum distribution rules, which we will analyze and share in the near future.

For a copy of these new regulations, please email us at agassman@gassmanpa.com.

What Estate Planning and Other Lawyers Need to Know About Bankruptcy

Part 1 of 3

Bankruptcy lawyer Al Gomez and Alan Gassman have recently updated their article on bankruptcy for publication. We last published this in Trusts & Estates in October of 2007 under the title of “Avoid Catastrophe – Know the Bankruptcy Code to Ward Off Devastating Surprises to an Estate Plan.”

We bring this now to Thursday Report readers as a three part piece, beginning as follows:

EXECUTIVE SUMMARY – Essential Knowledge for Estate Planning Lawyers and Advisors:

While many estate planners are familiar with asset protection mechanisms, even a great many lawyers who regularly provide asset protection advice have limited knowledge of the U.S. Bankruptcy Code and laws and practices associated therewith, notwithstanding that these rules can have a catastrophic effect upon an estate plan or corporate structure. Indeed, many estate tax- and income tax-oriented planning structures risk being dismantled by a bankruptcy judge, even though the plan’s primary purpose had nothing to do with creditor protection.

That is why it is critical to not only know the basics, but also to recognize certain rules that apply in the bankruptcy forum and the need to consult with a bankruptcy lawyer in certain situations. The following information will provide an update, review, or excellent introduction to this most important segment of financial services.

FACTS:

CRUCIAL BASICS

Any estate planning client could end up in a bankruptcy proceeding, whether voluntarily or involuntarily. In many cases, it is unlikely that a client would choose to file a voluntary bankruptcy petition. Often, a client may be forced into a bankruptcy proceeding on an involuntary basis.1 And since the implementation of the 2005 Bankruptcy Abuse Prevention and Creditor Protection Act (2005 Bankruptcy Act), there are more stringent requirements imposed on consumer debtors that must be met for them to be eligible to file a petition.

In general, there are three types of bankruptcy:

Chapter 7 is essentially a liquidation mechanism.

Chapters 11 and 13 contemplate a repayment plan.

A Chapter 7 debtor must meet a “means test.” Upon filing a petition to implement an automatic stay against creditor actions, a Chapter 7 trustee is appointed and the assets become property of the bankruptcy estate, many of which may qualify as exempt. In Chapter 7, the court essentially takes a snapshot of the debtor’s assets and liabilities as of the date of filing.

This is significant because the debtor’s post-petition earnings are not property of the estate. For example, if a debtor won the lottery post-petition, the lottery winnings would not be property of the estate. Typically, 90 days from filing, the debtor obtains a discharge from responsibility for pre-bankruptcy debt. The debtor is afforded a fresh start. However, there are some exceptions to the discharge rule. For instance, only individuals receive a discharge, not corporations. Other debts excluded from discharge include claims not listed by the debtor on the schedules, taxes, and domestic support obligations.

Chapter 13 is only available to individuals (not corporate or other business entities). To be eligible to file a Chapter 13, an individual must have unsecured debts of less than $383,175 and secured debts of less than $1,149,525.2 Chapter 13 repayment plans are for three to five years and are funded by the debtor’s disposable income. In exchange for paying under a Chapter 13 plan, a debtor keeps his or her assets. Chapter 13 is prospective as opposed to the snapshot concept of Chapter 7. The Chapter 13 trustee administers payments under a plan once a court confirms the plan. At the conclusion of the plan, after payments are made, the debtor obtains a discharge.

Chapter 11 is used primarily for business entities, but individuals with significant assets or who do not meet the debt limits for Chapter 13, may file a Chapter 11. Instead of a trustee, the debtor becomes the debtor-in-possession (DIP) and is afforded an opportunity to propose a plan. The DIP remains in possession and control of her assets. Chapter 11 requires the debtor to obtain the vote of creditors in order to confirm the plan, unless the debtor is able to “cramdown” the plan as authorized by the Code. The cramdown rules allow the bankruptcy judge to approve the debtor’s plan over the objections of dissenting creditors. The cramdown is only permitted if the plan does not discriminate unfairly, and is fair and equitable to the dissenting classes.

Estate planners should become well-versed in the nuances of these three types of bankruptcies, because significantly different results could occur depending on what chapter applies. For instance, in the case of the lottery winnings, if the winnings were obtained post-petition in a Chapter 7, the debtor would keep the winnings. On the other hand, if the winnings occurred while in a Chapter 13 or Chapter 11, the winnings are property of the estate.

Moreover, the application of the attorney/client privilege differs depending on whether a client files for Chapter 7, 11, or 13. When a Chapter 7 bankruptcy petition is filed, the Chapter 7 trustee may become the owner of the attorney/client privilege, as well as all client files for purposes of asserting or waiving the privilege. There is a split of authority on this point.3

Therefore, correspondence to the client that may reveal significant risks or adverse issues with respect to potential creditor planning might cause irreparable damage to the client, and the estate planner, if and when a bankruptcy petition is filed. However, the above privilege issue would not arise in the context of a Chapter 13 or Chapter 11 bankruptcy.

INVOLUNTARY BANKRUPTCY

It only takes one creditor to force a debtor into involuntary bankruptcy when the debtor has fewer than 12 creditors. Under 11 U.S.C. Section 303, when a debtor has 12 or more creditors, an involuntary bankruptcy can be commenced only when 3 or more creditors file a petition, with each creditor holding a claim that is (1) not contingent as to liability, and (2) not subject to a bona fide dispute as to liability or amount.

A creditor cannot be counted in the three-or-more-creditor requirement if it holds a lien on the debtor’s property, unless its claim exceeds the value of the property liened by at least $12,300. Generally, employees and “insiders” are not counted as creditors in determining whether 12 creditors exist. Because of the stricter bankruptcy rules, which are now applicable, more clients with large judgments against them will be rendered insolvent, yet will attempt to avoid or delay bankruptcy while maintaining their creditor exempt assets. Creditors may respond by utilizing the involuntary option.

Next week, we will provide further discussion of the 12 creditor requirements and cover a number of other important bankruptcy principles that estate planners need to be aware of.

———————————————————————————————————–

111 U.S.C. Section 303 (2007).

211 U.S.C. Section 109(e) (2010).

3Community Futures Trading Comm’n v. Weintraud, 471 U.S. 343 (1985), held that a trustee may waive the attorney client privilege for a corporate Chapter 7 debtor, but it did not extend its holding to individual debtors. See Miller v. Miller, 247 B.R. 704 (Bankr. D. Ohio 2000), discussing the split of authority.

“The IRS ‘Madoff’ with My Estate!”

In Estate of Kessel, the IRS argued that the value of the decedent’s estate should include the date-of-death value of the decedent’s pension account managed by Bernie Madoff. The decedent died in July of 2006 and, at the time of his death, he purportedly held more than $4.8 million of appraised assets in his Madoff investment account. The decedent’s federal estate tax return included the value of the Madoff account, and the estate paid the tax liability, which included value of the Madoff account in the tax determination. Following the realization of Bernie Madoff’s Ponzi scheme, the estate determined that the decedent’s Madoff investment account had zero value. The estate, therefore, filed a supplemental federal estate tax return seeking a $1.9 million refund based on the worthlessness of the decedent’s Madoff account. The IRS denied the refund and, instead, IRS determined that the estate had a $339,143 deficiency in the initial federal estate tax return.

The IRS maintained that the estate was not entitled to the refund because it measured the Madoff’s account value at the time of decedent’s death as what a willing buyer would pay to a willing seller for such account. The IRS argued since the account was purportedly valued at $4.8 million, a willing buyer would likely pay that amount for the account because at the time of the decedent’s death, a willing buyer would neither reasonably know nor foresee that Bernie Madoff was operating a Ponzi scheme. The IRS moved for summary judgment on these grounds. The Tax Court, however, denied the IRS’s motion because the court found that whether a willing buyer had a reason to believe that Bernie Madoff was operating a Ponzi scheme was a question of material fact. While the Tax Court denied this motion, the case is still pending. Stay tuned.

Thoughtful Corner

How to Help a Client Express What They Want for Children Who May Have Mental, Addiction, or Similar Issues:

Give Discretion to Trustees But Have an Explicit Letter of Wishes in the File

Clients often have children or others in the family that they would like to benefit in restrictive ways without embarrassing the person in trust documents.

One solution is to provide that one or more beneficiaries will be able to take over trusteeship of trusts at certain ages, while others will not. This does not have to be so obviously drafted so as to embarrass the beneficiary of concern.

The following Letter of Wishes can be used to express the client’s instructions to fiduciaries. This particular one also goes into some detail about coordinating efforts with an ex-spouse who will also be on the scene if the client dies.

To my Trustees:

As I design my estate plan I am mindful that my daughter, [NAME], has been a “straight-A kid” in all ways. I have every confidence that she will succeed without the need for much assistance, and will be able to handle her own financial decision making upon reaching proper ages, as is or will be reflected in my estate planning documents.

I have significant admiration for how well my son, [NAME], has done in the face of challenges beyond his control. I am very proud that he has developed into a resourceful, caring, and admirable adult, but I also would like to make sure that he is completely protected for his entire lifetime to the extent that this is made possible by whatever legacy and wealth I am able to leave for him.

I would strongly prefer that he support himself to the maximum extent possible, and I have been very impressed with his ability to economize and not waste money or financial opportunities, and am pleased that he is not materialistic or in need of “showing off” what he has or has access to.

I am hopeful that in decades to come there will be improved medications and treatments for individuals who have challenging circumstances, but I am mindful that my future grandchildren may carry genes that would give them similar challenges.

I have therefore requested special provisions for my trust documents that will give professional trustees or trust companies the ability to maintain lifetime control over trusts for my son and his descendants as they deem fit, and for my daughter’s descendants if she is no longer living, has descendants, and has not herself otherwise designated.

I also would be remiss to not point out that my children’s mother, [NAME], is presently well off financially, and should be able to provide assistance and support, as well as input and encouragement, for our descendants.

[EX-SPOUSE] and I had some wonderful years together, and both of us dedicated significant efforts to raising these two much loved children. I request that my fiduciaries work with her as best as possible to help assure that overall well being, opportunity, and personal achievement are maximized for our common descendants.

Although I do not consider this document to be part of my trust agreement, I request that ____________ and _____________, as Trust Protectors under the Agreement, take such actions as they deem appropriate, but only after careful consideration and extensive testing and interviewing by well-respected, independent professionals who advise on mental health issues, special needs planning, financial budgeting, and investment managers.

Seminar Announcement

To register for the 12 P.M. webinar, please click here.

To register for the 7 P.M. webinar, please click here.

Humor! (Or Lack Thereof!)

The Duck and the Pharmacist

A duck walks into a pharmacy and says, “Do you have any chapstick?”

When the pharmacist hands it to him, the duck replies, “Thanks, just put it on my bill.”

Kentucky Fried Duck

a poem by Colonel Sanders

Kentucky Fried Duck

We tried, but it wouldn’t cluck

Ludwig and Donald tried to buy in

And offered us Daffy again and again

But the wings were too large

To fit in our buckets

At first we tried boxes

But later said chuck it!

Upcoming Seminars and Webinars

NEW PORT RICHEY SEMINAR:

Alan S. Gassman and Kenneth J. Crotty will be speaking at the North FICPA Monthly meeting on two topics:

- Planning for Same Gender Couples and Laws that Apply to All Couples

- A CPAs Guide to Trust, Tax Law and Compliance

Date: Wednesday, July 16, 2014 | 4:30 p.m.

Location: Chili’s 9600 US Highway 19, Port Richey, FL.

Additional Information: If you would like to attend this seminar please contact Ron Cohen at 352-257-9518 or email agassman@gassmanpa.com

********************************************************

FREE LIVE WEBINAR:

STEP-UP YOUR EFFORTS TO STEP-UP CLIENTS’ BASIS – STRATEGIC ESTATE PLANNING AND STEPPED-UP BASIS CONSIDERATIONS

Date: Wednesday, July 23, 2014 |12:30 p.m. (30 Minute Webinar)

Speakers: Edwin P. Morrow, III, Alan S. Gassman

Location: Online webinar

Additional Information: To register for the webinar please click here.

********************************************************

FREE LIVE WEBINAR:

GAUGING AND HANDLING ENTITLEMENT TENDENCIES OF BENEFICIARIES, EMPLOYEES AND OTHERS – A FASCINATING AND EXTREMELY PRACTICAL GUIDE ON SOCIETY’S NEWEST ISSUE

Date: Tuesday, July 29, 2014 | 12:30 p.m. (30 Minute Webinar)

Speakers: Stephanie Thomason, Ph.D. and Alan S. Gassman, Esq.

Location: Online webinar

Additional Information: To register for the webinar please click here.

********************************************************

FREE LIVE WEBINAR:

HIPPA MEDICAL OFFICE DISASTER AVOIDANCE CHECKLIST

This 20-25 minute webinar includes valuable forms and important strategies that every medical office should know about. Join us for an interactive and innovative discussion of how medical practices can be decimated by HIPPA, including a number of survival techniques, tips, and tools.

Date: Tuesday, August 5, 2014 | 12:00 p.m. and 7:00 p.m.

Speakers: Alan S. Gassman, Lester Perling, and Jeff Howard

Location: Online Webinar

Additional Information: To register for the 12 p.m. webinar, please click here. To register for the 7 p.m. webinar, please click here.

*******************************************************

FREE LIVE WEBINAR:

A POWERFUL 40 MINUTE DOUBLE HEADER WITH JONATHAN BLATTMACHR

Topics:

- Foreign vs. Domestic Asset Protection Trusts: More Than Just Creditor Protection Considerations

- Empowering Your Powers of Appointment: Don’t Leave Out Important Tax and Practical Provisions or Ignore Important Considerations. With Sample Provisions

Date: Tuesday, August 12, 2014 | 12:00 p.m.

Location: Online webinar

Additional Information: To register for the webinar please click here.

********************************************************

LIVE ISLE OF MAN PRESENTATION:

Alan S. Gassman will be speaking on US TRUST AND TAX LAWS FOR INTERNATIONAL INVESTORS at Cayman National Bank and Trust Company on the Isle of Man

Sign up now and you will receive a free lunch! Transportation not included.

“Half-way between England

And Ireland in the Irish Sea.”

Is a great place to discuss trusts with glee.”

Date: Wednesday, September 3, 2014

Additional Information: If you would like to receive a copy of the materials that will be presented please email Janine Gunyan at janine@gassmanpa.com and we will send them to you once they are ready.

********************************************************

LIVE FT. LAUDERDALE PRESENTATION:

FICPA ANNUAL ACCOUNTING SHOW

Alan S. Gassman will be speaking at the FICPA Annual Accounting Show on Thursday, September 18, 2014 on the topic of ESSENTIAL GUIDE TO BASIC TRUST PLANNING for 50 minutes.

This presentation will introduce basic and intermediate trust planning background and provide attendees with an orderly list of the most commonly used trusts, practical features and traps for the unwary, including revocable, irrevocable and hybrid. The discussion will include tax, creditor protection and probate and guardian considerations.

Date: Wednesday, September 17 through Friday, September 19, 2014

Location: Fort Lauderdale, Florida

Additional Information: For more information about this program please contact Stephanie Thomas at ThomasS@ficpa.org

********************************************************

LIVE CLEARWATER PRESENTATION:

Board Certified Tax Attorney Michael O’Leary from the Trenam Kemker firm in Tampa, Florida and Christopher Denicolo from Gassman Law Associates will be speaking at the Ruth Eckerd Hall Planned Giving Advisory Council event on Tuesday, September 23, 2014.

Mr. O’Leary’s topic is HOT TOPICS IN CHARITABLE PLANNING AND MORE.

Mr. Denicolo’s topic is PLANNING FOR INHERITED IRAs.

Date: Tuesday, September 23, 2014 | 5:00 p.m.

This presentation is free to members of the Ruth Eckerd Hall Planned Giving Advisory Council, Ruth Eckerd Hall members, and professionals who are attending a Ruth Eckerd Hall Planned Giving Advisory Council event for the first time.

Additional Information: You can contact Suzanne Ruley at sruley@rutheckerdhall.net or via phone at 727-791-7400, David Abelson at david.abelson@morganstanley.com or via phone at 727-773-4626, Alan S. Gassman at agassman@gassmanpa.com or via phone at 727-442-1200 or the Kentucky Fried Chicken located at 1960 Gulf to Bay Blvd, which is close in proximity to this location and available to provide you with crisp, spicy or even crispier chicken, mashed potatoes and gravy, rolls, and slaw! Bring your 32 oz. Kentucky Fried Chicken drink container to the presentation and we will fill it with your choice of club soda or seltzer water, but no sharing permitted.

********************************************

LIVE NEW JERSEY PRESENTATION – WHAT NEW JERSEY LAWYERS NEED TO KNOW ABOUT FLORIDA LAW TO REPRESENT SNOWBIRDS AND FLORIDA BASED BUSINESSES:

NEW JERSEY INSTITUTE FOR CONTINUING LEGAL EDUCATION (ICLE)_SPECIAL 3 HOUR SESSION

New Jersey song trivia: What song includes the words “Counting the cars on the New Jersey Turnpike, they’ve all gone to look for America”? What year was it recorded and who wrote it?

Alan S. Gassman will be the sole speaker for this informative 3 hour program entitled WHAT NEW JERSEY LAWYERS NEED TO KNOW ABOUT FLORIDA LAW

Here is some of what the New Jersey Bar Invitation for this program provides:

New Jersey residents have always had a strong connection to Florida. We vacation there (it=s our second shore), own Florida property (or have favored relatives that do) and have family and friends living there. Sometimes our wealthiest clients move to Florida and need guidance, and you need background in order to continue representation.

There are real and significant differences between the two states that every lawyer should be cognizant of. For example, holographic wills are perfectly legitimate in New Jersey and anyone can serve as an executor of an estate, which is not the case in Florida. Also, Florida=s new rules regarding LLCs are different, and if you are handling estates of New Jersey decedents who owned Florida property, there are Florida law issues that must be addressed. Asset protection differs significantly in Florida too.

Gain the knowledge you need to assist your clients with Florida matters including:

- Florida specific laws involving businesses, trusts, and estates

- Florida tax planning

- Elective share and homestead rules

- Liability Insulation and Planning

- Creditor Protection and Strategies

- Medical Practice Laws

- Staying within Florida Bar Guidelines that allow representation of Florida clients

Comments from past attendees of this program:

- Excellent seminar and materials!!!

- This was one of the best ICLE seminars yet!

- One of the best seminars I have attended.

- Better than mashed potatoes and gravy. Glad he didn’t serve grits!

Date: Saturday, October 4, 2014

Location: TBD

Additional Information: This is a repeat of the same program that we gave last year, but our book is now updated for the new Florida LLC law and changes in estate and trust law. Please tell all of your friends, neighbors, and enemies in New Jersey to come out to support this important presentation for the New Jersey Bar Association. We will include discussions of airboats, how to get an alligator off of your driveway, how to peel a navel orange and what collard greens and grits are. For additional information, please email agassman@gassmanpa.com

********************************************************

LIVE PASCO COUNTY COCKTAIL HOUR AND PRESENTATION:

Alan S. Gassman and Christopher J. Denicolo will be speaking at the Pasco-Hernando State College’s Planned Giving Consortium Luncheon on Planning for Inherited IRA’s in View of the Recent Supreme Court Case – and Demystifing the “Stretch in Trust” Ira and Pension Rules

Date: Thursday, October 23, 2014 | 4:30 p.m.

Location: Spartan Manor, 6121 Massachusetts Avenue, Port Richey, Florida

Additional Information: For more information, please contact Maria Hixon at hixonm@phsc.edu

**********************************************************

LIVE UNIVERSITY OF NOTRE DAME PRESENTATION:

40th ANNUAL NOTRE DAME TAX & ESTATE PLANNING INSTITUTE

Please send us your questions, comments and suggestions for Alan Gassman’s talk on Planning with Variable Annuities and Analyzing Reverse Mortgages.

This presentation will cover the unique income tax and financial planning characteristics of fixed and variable annuities.

Topic #2: THE MATHEMATICS OF ESTATE AND ESTATE TAX PLANNING

Christopher J. Denicolo, Kenneth J. Crotty and Alan S. Gassman will also be presenting a special Wednesday late p.m. two hour dive into math concepts that are used or sometimes missed by estate and estate tax planners. This will be an A to Z review of important concepts, intended for estate planners of all levels, sizes and ages. Donald Duck has rated this program A+.

Date:November 13 and 14, 2014

Location: Century Center, South Bend, Indiana

We welcome questions, comments and suggestions on variable annuities, which will be Alan Gassman’s topic for this conference.

Additional Information: The focus of this year’s institute will be on “Business Succession Planning: An Income Tax, Estate Tax and Financial Analysis.” As in past years, several sessions are designed to evaluate certain financial products and tax planning techniques so that the audience can better understand and evaluate these proposals in determining not only the tax and financial advantages they offer, but also evaluate limitations and problems they may cause in the future. Given that fewer clients will need high-end estate tax planning with the $5 million exemptions, other sessions will address concerns that all clients have. For example, a session will describe scams that target elderly individuals and how to protect the elderly from these scams. As part of the objective on refreshing or introducing the audience to areas that can expand their practice, other sessions will review the income tax consequences of debt cancellation, foreclosures, short sales, the special concerns that arise in bankruptcy and various planning available to eliminate the cancellation of debt income or at least defer it with a possible step-up basis at death. The Institute will also continue to have sessions devoted to income tax planning techniques that clients can use immediately instead of waiting to save estate taxes far in the future.

********************************************************

LIVE FORT LAUDERDALE PRESENTATION:

Alan Gassman will be speaking at the 2015 Representing the Physician Seminar on the topic of DISASTER AVOIDANCE FOR THE DOCTOR’S ESTATE PLAN.

Date: January 16, 2015

Location: TBD – Fort Lauderdale, Florida

Additional Information:For more information, please email Alan Gassman at agassman@gassmanpa.com

********************************************************

LIVE NAPLES PRESENTATION:

2nd ANNUAL AVE MARIA SCHOOL OF LAW ESTATE PLANNING CONFERENCE

Date: Friday, May 1, 2015

Location: Ave Maria School of Law, 1025 Commons Circle, Naples, Florida

Additional Information: Jerry Hesch and Alan Gassman will present The Mathematics of Estate Planning. If you liked Donald Duck in Mathematics Land, you will love The Mathematics of Estate Planning. This will not be a Mickey Mouse presentation.

Other speakers include Jonathan Gopman, Bill Snyder, Elizabeth Morgan, Greg Holtz, and others.

Please let us know any questions, comments, or suggestions you might have for this amazing conference, which features dual session selection opportunities in one of the most beautiful conference facilities that we have ever seen.

And don’t forget to have a great weekend in Naples with your significant other or anyone who your significant other doesn’t know! Domino’s Pizza is extra.

NOTABLE SEMINARS BY OTHERS

(We were not invited, but will attend and are still excited!)

LIVE ORLANDO PRESENTATION

49th ANNUAL HECKERLING INSTITUTE ON ESTATE PLANNING

Date: January 12 – 16, 2015

Location: Orlando World Center Marriott 8701 World Center Drive, Orlando, Florida

Additional Information: For more information please visit: https://www.law.miami.edu/heckerling/?op=0

********************************************************

LIVE ST. PETERSBURG PRESENTATION:

ALL CHILDREN’S HOSPITAL FOUNDATION

Date: Thursday, February 12, 2015

Location: St. Petersburg, FL

Additional Information: Please contact Lydia Bennett Bailey at Lydia.Bailey@allkids.org for more information.

********************************************************

LIVE PRESENTATION:

2015 FLORIDA TAX INSTITUTE

Date: Wednesday through Friday, April 22 – 24, 2015

Location: TBD

Additional Information: Please contact Bruce Bokor at bruceb@jpfirm.com for more information.

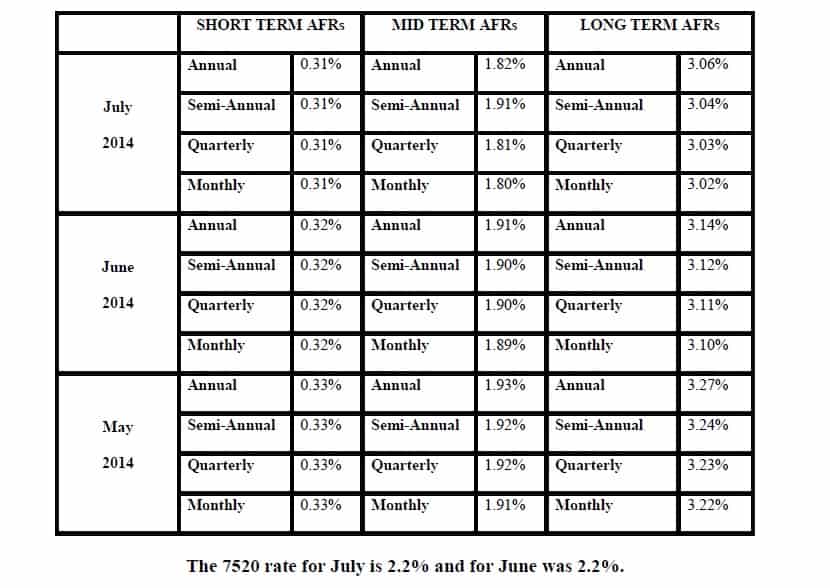

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.