The Thursday Report – 3.2.17 – Greetings From the Island of St. Maarten

Re: Greetings From the Island of St. Maarten

Father and Son to Buy a Duplex for Son to Live in and Rent Out – How to Own it and Other Considerations

Employer Retaliation – What Protections Do Whistleblowers Have?

The Next iOS? by Pariksith Singh, M.D.

Avoiding Service Business Burnout (Top 5 Leverage Points) by David Finkel

Richard Connolly’s World – IRS Issues Warning on New Scam Targeting Tax Professionals

Humor! (or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Alan at agassman@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Quote of the Week

“Many of us are more capable than some of us, but none of us is as capable as all of us.”

– Tom Wilson

The above stated quote was recommended by Jeff Howard, also known as, Ziggy Howard.

Tom Wilson was an American cartoonist who lived for artistic expression. From 1953 to 1955 he served in the United States Army where he also played bass in the Army band. He graduated from the Art Institute of Pittsburgh in 1955, and was an art instructor from 1961 to 1962. Other notable titles he held include: Creative Director at American Greetings, Vice President of Creative Development, and President of “Those Characters from Cleveland”, which was American Greetings character licensing subsidiary.

However, he is best known as the creator of the iconic comic strip, Ziggy, which he drew from 1971 to 1987. In 1987 he passed those duties on to his son, Tom Wilson Jr. who continues to write and draw the comic strip today. Ziggy is often depicted as a “clumsy, wide-eyed, teddy-bear-shaped ‘little guy in a big world.’” “One of the great appeals of the comic strip is how Ziggy himself deals with the endless stream of misfortunes which befall him on a daily basis.”

Father and Son to Buy a Duplex for Son to Live in and Rent Out – How to Own it and Other Considerations

by Alan Gassman

We recently wrote a letter to a father and son that summarizes limited liability, manager liability, Florida homestead implications, and tax planning for the purchase of a duplex.

We share this letter below to provide our readers with a checklist of considerations.

Please let us know what we left out.

Dear Father and Son:

It was a pleasure meeting with Son on Friday.

I thought that it would be helpful to reiterate some of what we discussed.

When someone gets hurt on a property they typically sue the landlord and anyone who was active in the management of the property if they can show that there was a defect or danger that should not have been there.

The first line of defense is liability insurance, but this is not always enough when there is a severe injury.

In addition, there could be other types of liability associated with this property, such as hazardous waste issues, which are typically not covered by insurance and can cause liability even though the underground waste is pre-existing and the land owner had no way of knowing that it was there.

We often place properties under LLC’s (Limited Liability Companies) to shield the owner of the property from liability, and also encourage clients to use well drafted lease agreements that explicitly make responsibility for the condition and maintenance of the property the tenant’s, to the extent possible. Son and I discussed, however, that people hurt on the property will often sue the manager of the LLC and any property manager while trying to show that they were somehow personally responsible for injuries that have occurred.

One possible solution would be to have the property owned by an LLC that would be owned 50% by each of you. This would provide a liability shield, but the LLC would be required to file a Form 1065 partnership tax return each year, which is extra paperwork.

It might be worthwhile to file a Form 1065 if there will be some fringe benefits paid for from the LLC that are less likely to be audited on a Form 1065 than on personal returns.

Most clients would each form an LLC and have each LLC owned 50% if the property is not going to be the homestead of either of you. Then, each LLC can be disregarded for income tax purposes, and there is no need to file a Form 1065. The income and deductions for the property would go one half on each of your personal tax returns.

We discussed that Son has limited assets and could file a bankruptcy to eliminate just about any kind of judgment that might exist as the result of ownership of this property.

We also discussed that Son will live on the property, and should therefore qualify for approximately $1,000 in tax savings based upon the homestead exemption, although this is actually normally based upon 2/10ths of 1% of the tax assessed value of the property multiplied by the percentage owned by the person homesteading it, which may be significantly less than $50,000.

We therefore discussed having 50% of the property owned by Fathers’s real estate LLC (2007 ABC, LLC), or a new LLC that could be formed for Father if Father does not want the risk from this duplex to cause possible loss of the equity in the property at 2007 ABC Street, My City, Florida.

Father presently has 2 LLCs, 2007 ABC, LLC which owns the property at that address, subject to a small mortgage.

This LLC could own half of the duplex. It would make sense to let Son be the manager of the LLC that owns part of the duplex. Father is presently the manager, but would not want to have the management responsibility for the duplex, or the blame that might come along with being listed as the manager of an LLC that owns half of the duplex.

It would be safer to set up a separate LLC for Father that would own his half of the duplex, but probably not worthwhile if you will have plenty of liability insurance.

I welcome your questions, comments and suggestions on the above.

It also occurs to me that Son should give a financial and health care power of attorney to someone and also should sign a living Will and possibly a Last Will and Testament. Son should probably have the same.

Employer Retaliation – What Protections Do Whistleblowers Have?

by Seaver Brown and Ken Crotty

An IRS Form SS-8 is typically filed so that the IRS can determine whether an individual worker is an employee or independent contractor for purposes of federal employment taxes and income tax withholding. What protections are available to these individuals when he or she files a Form SS-8, and their employer then fires them as a result of the IRS’ evaluation of their status as an independent contractor or employee?

Fair Labor Standards Act

The federal prohibition of retaliation by employers is found under Section 15(a)(3) of the Fair Labor Standards Act (“FLSA”). It states that it is unlawful for any person to discharge an employee because he or she filed a complaint, instituted a proceeding under or related to the FLSA, or testified in any such proceeding.

According to the Department of Labor Wage and Hour Division, employees are protected regardless of whether the complaint is made orally or in writing. Complaints made to the Wage and Hour Division are protected, and most courts have ruled that internal complaints to an employer are also protected as well.

Further, an employee who has been wrongfully discharged because they filed a complaint or cooperated in an investigation, may file a retaliation complaint with the Wage and Hour Division, or a private cause of action seeking remedies such as employment, reinstatement, lost wages and liquidated damages.

Florida Whistle-Blower Laws

Florida has a similar whistle-blower protection statute under Florida Statute § 448.102, which provides:

“An employer may not take any retaliatory personnel action against an employee because the employee has:

- Disclosed, or threatened to disclose, to any appropriate governmental agency, under oath, in writing, an activity, policy, or practice of the employer that is in violation of a law, rule, or regulation. However, this subsection does not apply unless the employee has, in writing, brought the activity, policy, or practice to the attention of a supervisor or the employer and has afforded the employer a reasonable opportunity to correct the activity, policy, or practice.

- Provided information to, or testified before, any appropriate governmental agency, person, or entity conducting an investigation, hearing, or inquiry into an alleged violation of a law, rule, or regulation by the employer.

- Objected to, or refused to participate in, any activity, policy, or practice of the employer which is in violation of a law, rule, or regulation.”

Importantly, Section 448.102(1) provides that the employee must give the employer both written notice of the unlawful activity and a reasonable opportunity to correct the activity. However, in the 2000 Florida Supreme Court case of Golf Channel v. Jenkins, the Court held that the “requirement of the Whistle-Blower Act that employees give their employers written notice as a prerequisite to maintaining a cause of action based on retaliatory personnel action does not apply to claims based on retaliation for employee’s assistance in ongoing investigation [Subsection (2)] or to claims based on employee’s objection to unlawful activity of employer [Subsection (3)].”

Thus, if an individual files an action under the Whitsle-Blower Act, he or she must only provide written notice and reasonable time to correct when they disclose the employer’s illegal activity to a governmental agency. The same requirements do not apply when the employee is providing information during an ongoing investigation or when they object to participate in an illegal activity. I would argue that the act of filing a Form SS-8 with the IRS could be construed as a “disclosure to a governmental agency,” and would therefore fall under the purview of Florida Statute § 448.102(1).

Important Case Law

In the 2010 United States District Court case for the Middle District of Tennessee, the court allowed a couple who worked as independent contractor drivers to go forward into discovery, based on a claim that the company had wrongly classified them as independent contractors to avoid FICA taxes, and then faced retaliation from the company and its owners when they learned the husband driver filed a Form SS-8. The IRS determined that the drivers were employees, not independent contractors.

The couple then brought a Fair Labor Standards Act cause of action, claiming that they were discharged for filing a Form SS-8, and also, state law claims under the Tennessee Whistleblower Act, and damages under the common law of retaliatory discharge. The Court determined that the complaint set forth sufficient facts to state a plausible claim for relief to allow the plaintiffs to proceed to take discovery.

The Florida cases I reviewed that cited Section 448.102 appeared to only address Subsection (3), in which the individuals object to committing an unlawful act on behalf of the company. The Tennessee case at least shows that courts are willing to allow a cause of action if someone is apparently discharged because they filed a Form SS-8.

The Next iOS?

by Pariksith Singh, M.D.

Is it possible to have a foundational multi-sided platform in health care? Something like Windows 95 or iOS? Such an infrastructure would surely be revolutionary.

The key for such a platform, in my opinion, would be end-use. The problem with most information technology companies in health care is they lack deep subject matter expertise in various aspects of medicine. Lacking this knowledge, the pain points for providers are seldom addressed. For example, electronic medical records (EMRs) remain slow and clunky, making providers spend more time entering data than addressing patient’s needs. Most EMRs are not managed care savvy and cannot handle issues like Medicare Risk Adjustment, HEDIS, or diagnosis validation, never mind following utilization and wellness or health outcome patterns.

What can be done in this fractionated industry to have data flow seamlessly from one source to another so that the end-point, the patient’s engagement with the provider, is enhanced? At present the various softwares are seldom interoperable. Thus, much time is wasted pulling and addressing data requirements manually in this information-enabled age.

Business revenue cycle is not one single interconnected data flow but different formats of information that is not timely, accessible, available or actionable. How can all these modules and various aspects of medicine be interconnected seamlessly?

To my mind, a simple answer is to create a core platform that is stable and modular which can have end-to-end linkages. On this unvarying structure can rest extremely nimble applications that can adapt swiftly to the rapidly evolving needs of health care. Such a platform needs to have a transactional face for providers which is extremely easy to use, intuitive and fast and a background structure where data is stored in a data warehouse. A multi-layered, multi-tenanted, cloud-based, mobile-enabled, socially-connected anti-fragile platform is possible in health care.

In ancient Indian thought, the Universe is borne by the Brahman that is eternally still and unmoving, “agnostic” to all fluctuations and infra-structures, formless and unlimited, nirvikaara. It supports the Shakti principle that is infinitely and endlessly mobile and variable. The Universe thus, would be the ultimate platform supporting “all in one and one in all”, the macroscopic and the vast simultaneously with the most granular and minute. The Brahman is the core on which rests the Shakti that is flexible and constantly new.

This platform needs to be able to connect with provider communities, or patient communities, which may be closed or open. It also needs to be integrated with a Learning Management System so that any errors by providers can be corrected on a real-time basis by a system that is able to perform rapid analytics, and can compute cognitively. Artificial Intelligence is much touted these days but perhaps we first need to awaken our Native Intelligence and create a simple structure that can perform elementary tasks.

Such a universal health care platform would be able to support provider, payer and patient side on one architecture. One entry in a doctor’s office about a patient having had a colonoscopy should address quality requirements on the payer side, check off the item on a list of measures at the patient’s portal and automatically update meaningful use and HEDIS measures from the provider side, while pulling the report or diagnostic that supports the measure into the medical record from wherever it exists. Similarly, one click from the patient side should have instant updating of records on the provider and payer ends. All these three parties could send the best and accurate data to the Center for Medicare and Medicaid Services if needed for managed care contracts and for those Medicare patients whose providers are participants in an ACO model, thus making it four-pronged. Similar requirements of integration of all three entities would be needed for commercial or Medicaid insurances.

Apple has recently tried to create a platform on the consumer side with iWatch, trying to integrate it with IBM’s Watson that works on the provider side. Similarly, IBM has tried to move into provider space by the use of analytics and protocols and work with accountable organizations. Athena too has tried to move from electronic medical records which is provider side to consumer side by opening patient portals. Yet, all these measures are incomplete, lacking in width and depth of scope, and only increase the fractionation of health care space at least for now. They may evolve eventually to a universal platform but that intent or knowhow does not seem to be influencing their development plans at the moment.

Such a platform would create a basis for rapid learning of the system by repeated iterations, help health care administrators, providers and patients. It could help focus each medical health care provider to his or her respective specialty and reduce wastage of resources. It would also build on the expertise of provider and information technology (IT) developers by creating a model where interactions can be open and mutually beneficial. The biggest roadblock in creating a platform is the wide chasm between IT and health care. If this distance can be bridged by developing strong teams and mutually beneficial relationships with common stake-holding, this fundamental challenge of health IT can be addressed.

Design thinking or end-use approach will be critical to create a space where quality of health care, evidence-based care management, health care outcomes, patient engagement and education and compliance to regulations would be at a premium. The ability to audit and test various entries and learn from them would be an important enhancement. This would help in establishing effective portals for patients and providers, help with accountable care and patient centered medical homes and remove the static that is at present creating a dissonance in medicine.

Data with intelligence and a human face is needed. Security with effectiveness that re-engineers operations and systems is possible with such an approach. Scalability with robustness would come from an approach that is user-based and user-driven. A platform that supports the entire ecosystem of medicine and is able to integrate with other platforms to ensure continuity of care and minimize medical errors is critical. It should use the latest technology and advancement in operations and organizations, using interfaces and dashboards and algorithms to enhance the human touch. Such a global platform, I believe, is within reach.

Avoiding Service Business Burnout (Top 5 Leverage Points)

by David Finkel

David Finkel is the Wall Street Journal bestselling author of SCALE: Seven Proven Principles to Grow Your Business and Get Your Life Back, which can be viewed by clicking here. As the CEO of Maui Mastermind, he has worked with 100,000+ businesses coaching clients and community members to buy, build, and sell over $5 billion worth of businesses.

Over the years my company, Maui Mastermind, has coached thousands of service businesses, helping them to overcome the typical obstacles that keep so many of these labor intensive companies small.

This is such a common challenge that we even have a name for it. We call it the “Self-Employment Trap.”

This is where the owner of the business is so consumed by his or her day-to-day management of the business that they don’t have the time or space to step back and focus on building a service business as a business. In essence they have built a self-employment job, not a business.

Is it any wonder that so many of these service business owners end up 5, 10, 20 years later totally burned out—hating the very business they once loved. They feel trapped. The business generated the income they need to support their family and their lifestyle. But because of how they have gone about building it, they can never really leave their business.

Whether you’re working business-to-business or business-to-consumer, service business owners have one of the highest incidents in getting caught in the Self Employment Trap of any category of business owner.

Why? Because of the high expectations of your clients combined with the difficulties in finding and managing your workforce to deliver up to your high standards.

This is a recipe for you the business owner forced into a role of catching many last minute mistakes or “fires” that you have to rush in and fix—often at a high price to your family and personal life.

Click here to read the full article.

Follow David on Twitter: @DavidFinkel.

Richard Connolly’s World

IRS Issues Warning on New Scam Targeting Tax Professionals

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature some of Richard’s recommendations with links to the articles.

This week, the article of interest is “IRS Issues Warning on New Scam Targeting Tax Professionals” by Kelly Phillips Erb. This article was featured Forbes.com on January 11, 2017.

Richard’s description is as follows:

The key to stopping scammers is staying one step ahead of the bad guys. That’s why the Internal Revenue Service, together with state tax agencies and tax industry partners, are warning tax professionals about a new scam this tax season. As part of the scam, cybercriminals are posing as clients soliciting services from tax professionals.

Please click here to read this article in its entirety.

Humor! (Or Lack Thereof!)

Marcia and I are now in St Maarten,

A Dutch and French Island,

Drinking rum by the Carton,

Hanging here with our Dutch and French Friends,

Walking the beaches, climbing up windmills,

The good food never ends

And while we’re away,

Our brave team in Clearwater did stay (including Maribeth@gassmanpa.com, who is always calm).

Where service is job one,

For you and everyone,

Our cruise departs Friday, to islands we will mention,

Assuming I’m not put in the brig on detention,

The pirates had it good,

Relatively speaking,

They made the most, of French toast,

While often drunk and streaking,

Parlaview for your understanding,

Of this away poem,

We’ll toast you with a herring and Heinken,

And if the boat runs out of gas they will tow’em.

We invite your poems back,

Even if finesse you lack,

But guard your retort,

We need fodder for the Thursday Report.

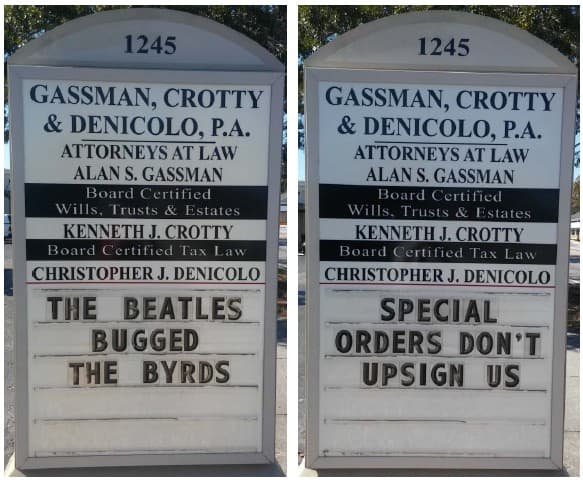

Sign Sayings of the Week

**********************************************************

In the News

by Ron Ross

Best acting award goes to producer of “La La Land” who graciously gives up best picture award.

The Big Winner: Steve Harvey, whose similar screw up at the Miss Universe Pageant now seems irrelevant.

**********************************************************

**********************************************************

Upcoming Seminars and Webinars

Calendar of Events

**********************************************************

LIVE DISNEY WORLD PRESENTATION (HOW MICKEY MOUSE CAN YOU GET?):

2017 MER CONTINUING EDUCATION PROGRAM TALKS FOR PHYSICIANS

Alan will be speaking at the Medical Education Resources (MER) Internal Medicine and Country Bear Jamboree for primary care physicians and other characters. We thank MER for this wonderful opportunity and Walt Disney for having paved all of Osceola County. His topics will include:

- The 10 Biggest Mistakes Physicians Make in Their Investments and Business Planning

- Lawsuits 101

- 50 Ways to Leave Your Overhead

- Essential Creditor Protection and Retirement Planning Considerations

Date: Wednesday, March 15, 2017 and Thursday, March 16, 2017

Location: Walt Disney World BoardWalk Inn | 2101 Epcot Resorts Blvd, Kissimmee, FL 34747

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE ESTATE PLANNING COUNCIL OF NORTHEAST FLORIDA PRESENTATION:

Alan will be speaking for the Estate Planning Council of Northeast Florida on March 20, 2018 on the topic of DYNAMIC PLANNING STRATEGIES FOR THE SUCCESSFUL CLIENT. This will be Alan’s third visit to Pensacola, and a welcome treat. Watch this space, as more details will be forthcoming!

Date: Tuesday, March 20, 2018

Location: To Be Determined

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE ESTATE PLANNING DISCUSSION AT FLORIDA STATE UNIVERSITY SCHOOL OF LAW

Alan will appear via Skype with professors Steven Hogan and Bob Pierce to give his views, by interview style, for their estate planning course at Florida State University School of Law on Thursday, March 23, 2017.

Date: Thursday, March 23, 2017 | 1:15 – 3:00 p.m. (EASTERN)

Location: Florida State University School of Law

Additional Information: To receive a live call in code or videotape of this presentation, which we will qualify for continuing legal education credit, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE FLORIDA BAR CLE SEMINAR

Alan will be speaking at the 2017 Annual Wealth Protection Program presented by the Florida Bar and the Continuing Legal Education Committee. Alan will discuss EXEMPTION AND FLORIDA PLANNING 2016 – MORE THAN WHAT YOU THOUGHT, AND LESS THAT WHAT YOU WISH FOR.

Additional topics and speakers include:

- Key Asset Protection Strategies Integrations & Estate Planning Techniques and Wealth Management Products – Denis Kleinfeld

- Important Recent Developments and trends in Debtor Creditor Law – Including Discussion of the Uniform Voidable Transfers Act – Michael Markham & Arthur Neiwirth

- The Secrets to Avoiding the Tricks and Traps in Partnership Tax Planning – Jerry Hesch

- Critical Factors Every Florida Planner Must Know in Using Offshore Asset Protection Strategies – Les Share

- Trends in Practice – The Growing Oppurtunties for Skilled Wealth Protection Professionals Important Wealth Protection Cases, Law and Trends of Practice – What Happened and Where Are We Going?

Date: Friday, April 7, 2017 | 8 a.m. to 5 p.m.

Location: Hyatt Regency Downtown Miami – 400 SE Second Avenue, Miami, FL 33131

Additional Information: For more information, please email Alan at agassman@gassmanpa.com. To register, visit www.floridabar.org/CLE and use the Course Number: 2332R. A webcast will be available by clicking here.

**********************************************************

LIVE NAPLES PRESENTATION:

Please put Friday, April 28th, 2017 on your calendar to enjoy the 4th Annual Ave Maria School of Law Estate Planning Conference and the weekend that follows in Naples.

Alan will be speaking at this conference on the topic of THE ETHICS OF AVOIDING TRUSTS AND ESTATE LITIGATION.

Alan will also appear on a panel of speakers with Jerry Hesch and Lester Law on the topic of TAX PLANNING WITH LIFE INSURANCE PRODUCTS, RECENT LITIGATIONS, AND OTHER HOT TOPICS.

Other speakers and topics include the following:

- Stacy Eastland – Comparing Freeze Techniques

- Jonathan Gopman – Asset Protection Trusts: An Update and Discussion of Planning

- Joan Crain – Challenges for Trustees in Dealing with Millennial Beneficiaries

- Jerry Hesch – Passing a closely-held business on to junior family members or key employees or co-owners: An analysis of the income tax, estate tax and financial impact of business succession planning techniques.

- Jerry Hesch & Alan Gassman – Life Insurance Planning Panel – Techniques, Tax Planning and The Good, the Bad, and the Ugly

- Tae Kelley Bronner – Homestead Planning and Update

- Lester Law – Basis Consistency for Estate and Income Tax Planning Purposes, and Multiple Implications Thereof.

- Marve Ann Alaimo & Dixon Miller – International Estate Planning Rules and Planning Opportunities

- Susan Cassidy, M.D. – What You Need to Know for Your Client’s Medical Issues: Competency, Great Care Versus the Mainstream, What Medicare Recipients Should Seek Outside of the Medicare System, End of Life Communications and Planning and How Will the Above be

- Alan Gassman – Ethical Considerations to Avoid Estate and Trust Litigation and Family Disputes, and the 10 or so Avoidance Techniques You Should Be Actively Using

- Suzy Walsh – Special Needs Trusts Essentials and Well Beyond

Date: Friday, April 28, 2017

Location: The Ritz-Carlton Golf Resort | 2600 Tiburon Drive, Naples, FL, 34109

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE LAS VEGAS PRESENTATION:

AICPA ADVANCED PERSONAL FINANCIAL PLANNING CONFERENCE

Alan will be speaking at the Advanced Personal Financial Planning Conference, sponsored by The American Institute of CPAs. His topic for this event is LIFE INSURANCE TIPS FOR THE FINANCIAL PLANNING PROFESSIONAL. He will speak on June 14 from 10:50 to 11:40 a.m.

This conference is part of the AICPA ENGAGE event, which brings together five well-known AICPA conferences with the Association for Accounting Marketing Summit for one, four-day event. The conferences included in ENGAGE are Advanced Personal Financial Planning, Advanced Estate Planning, Tax Strategies for the High-Income Individual, the Practitioners Symposium/TECH+ Conference, the National Advanced Accounting and Auditing Technical Symposium, and the Association for Accounting Marketing Summit.

Date: June 12th – June 15th, 2017 | Alan’s speaks on June 14 from 10:50 to 11:40 a.m.

Location: MGM Grand | 3799 S. Las Vegas Blvd., Las Vegas, NV, 89109

Additional Information: For more information, please email Alan at agassman@gassmanpa.com or click here.

**********************************************************

LIVE NAPLES PROFESSIONAL ACCELERATION WORKSHOP

Alan will present a Professional Acceleration Workshop at Ave Maria School of Law.

Date: Friday, August 25, 2017 | 10:00 a.m. Eastern

Location: Ave Maria School of Law, Naples, FL.

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com. More details will be provided in the future, but please plan to attend.

**********************************************************

LIVE NEW PORT RICHEY PRESENTATION:

Alan will present AN ESTATE PLANNER’S UPDATE AND HOT TOPICS for the Charitable Consortium.

Date: Thursday, September 14, 2017 | 12:00 p.m. Eastern

Location: TBD

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com.

**********************************************************

LIVE PRESENTATION:

ESTATE PLANNING COUNCIL OF NORTHEAST FLORIDA

Please put Tuesday, September 19, 2017 on your calendar to enjoy a dinner conference for the Estate Planning Council of Northeast Florida.

Date: Tuesday, September 19, 2017

Location: TBA

**********************************************************

LIVE PRESENTATIONS:

2017 MER CONTINUING EDUCATION PROGRAM TALKS FOR PHYSICIANS

Alan will be speaking at the following Medical Education Resources (MER) events:

- October 20th – October 22nd, 2017 in New York, New York

- November 30th – December 3rd, 2017 in Nassau, Bahamas

His tentative topics for these events include the 10 Biggest Mistakes Physicians Make in Their Investments and Business Planning, Lawsuits 101, 50 Ways to Leave Your Overhead, and Essential Creditor Protection and Retirement Planning Considerations.

Date: New York: October 20th – 22nd, 2017Nassau: November 30th – December 3rd, 2017

Location: New York: To be determined.

Nassau: Atlantis Hotel | Paradise Beach Drive, Paradise Island, Bahamas

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

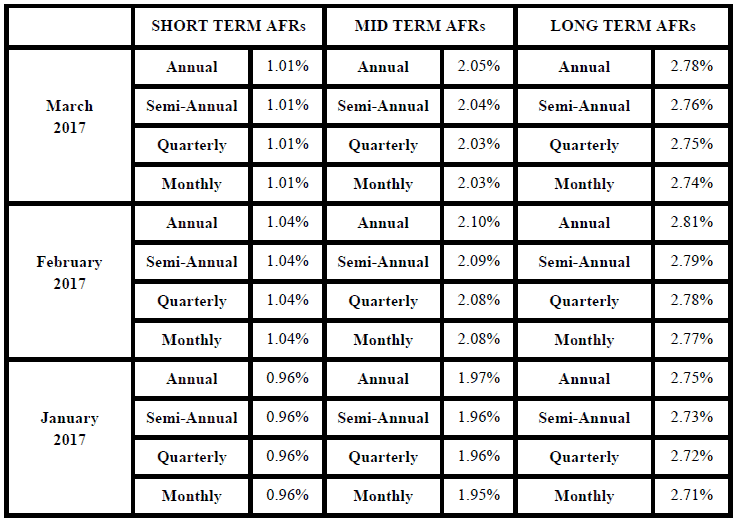

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.