The Thursday Report – 3.16.17 – Corned Beef Hash

Re: Corned Beef Hash

Consider Charging Order Protection

Florida Automobile Liability and How to Protect Yourself, Your Business, and Your Family

Florida Medical Marijuana Act Introduced

Making Systems Part of Your Company Culture by David Finkel

Richard Connolly’s World – One Lawyer, 6,905 Hours Leads to $1.5 Million Bill in Sprint Suit

Humor! (or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Alan at agassman@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Quote of the Week

“Fight for the things that you care about, but do it in a way that will lead others to join you.”

– Ruth Bader Ginsburg

United States Supreme Court Justice, Ruth Bader Ginsburg celebrated her 84th birthday yesterday on March 15. In 1993 she was appointed to the Supreme Court by President Bill Clinton. Before she became a Supreme Court Justice, Ginsburg was a leading advocate for the fair treatment of women. She is generally viewed as belonging to the liberal wing of the Court, and her opinions often display caution, moderation and restraint. She was married to Martin Ginsburg, who was an internationally renowned tax law expert and professor at Georgetown Law.

Some of her most notable decisions include: National Federation of Independent Business v. Sebelius; Olmstead v. L.C.; Bush v. Gore (dissenting); and Obergefell v. Hodges.

Consider Charging Order Protection

by Alan Gassman, Michael Markham & Kacie Hohnadell

Generally, a creditor who has a judgment against a limited partner or a member of a multi-member limited liability company cannot seize ownership or control of the equity interest, but instead can only receive a charging order that entitles the creditor to court of equity oversight and a right to receive what the debtor member would receive if and when there is ever a distribution.

The following language is from a broadly written Colorado District Court charging order. This charging order required the partnership to obtain court approval before making capital acquisitions, selling, encumbering or modifying any partnership interests. Additionally, the creditor was entitled to receive periodic tax and financial information on the partnership:

The partnership is directed to pay to the [plaintiff’s] law firm, as for the petitioner’s receiver, present and future shares of any and all distributions, credits, drawings, or payments to said law firm until the judgment is satisfied in full, including interest and costs.

Until said judgment is satisfied in full, including interest and costs, the partnership shall make no loans to any partner or anyone else.

Until said judgment is satisfied in full, including interests and costs, the partnership shall make no capital acquisitions without either court approval or approval of the judgment creditor herein.

Until said judgment is satisfied in full, including interests and costs, neither the partnership nor its members shall undertake, enter into, or consummate any sale, encumbrance, hypothecation, or modification of any partnership interest without either Court approval or approval of the Judgment Creditors herein.

Within ten days of service of a certified copy of this Order upon the registered agent of the partnership, the partnership shall supply to the Judgment Creditors, a full, complete, and accurate copy of the Partnership Agreement, including any and all amendments or modifications thereto; true, complete and accurate copies of any and all federal and state income tax or informational income tax returns filed within the past three years; balance sheets and profit and loss statements for the past three years; and balance sheet and profit and loss statement for the most recent present period for which same has been completed. Further, upon 10-day notice from Petitioners to the partnership, all books and records shall be produced for inspection, copying, and examination in the Petitioner’s office.

Until said judgment is satisfied in full, including all costs and interest thereon, all future statements reflecting cash position, balance sheet position, and profit and loss shall be supplied to Petitioners within thirty days of the close of the respective accounting period for which said data is or may be generated.[1]

Florida Statute § 608.433 was amended in 2011 to provide charging order protection for multiple-member LLCs after the Florida Supreme Court surprised the legal community by concluding that the previous statute did not provide charging order protection, although it was clearly intended to do so. The revised statute applies retroactively and specifically indicates that “a charging order is the sole and exclusive remedy by which a judgment creditor of a member or member’s assignee may satisfy a judgment from the judgment debtor’s interest in a limited liability company or rights to distributions from the limited liability company.” (Emphasis added). Florida Statute § 608.433 also specifically provides for protection for multiple-member LLCs, stating that “in the case of a limited liability company having more than one member, the remedy of foreclosure on a judgment debtor’s interest in such limited liability company or against rights to distribution from such limited liability company is not available to a judgment creditor attempting to satisfy the judgment and may not be ordered by a court.” (Emphasis added).

It is unclear whether charging order protection is available for multiple-member LLCs when all of the member interests are subject to charging orders and/or pledges that make it unlikely or impossible for any member to expect to receive any distributions from the entity. Florida Statute § 608.402(21) imposes a requirement that a “member” must have an “economic interest” in the LLC. If the judgment exceeds what would be reasonably expected to be derived from the member interest, does the member still have an “economic interest” if it is highly unlikely or even seems impossible that such member would ever receive a distribution from the entity? If the judgment creditor could receive all expected future distributions from the LLC, it seems that the individual members may no longer have an “economic interest” in the LLC. Thus, it is possible that the individuals would no longer meet the statutory definition of a “member” and could lose charging order protection if there is no reasonable expectation of ever receiving a distribution from the entity.

Single-member LLC ownership offers no substantive protection from a charging order standpoint under Florida law, but may help buy time where there is a judgment against the sole member. Under Florida Statute Section 608.433(6), a charging order is not the “sole and exclusive remedy” available to judgment creditors of a single-member LLC where the court of equity concludes that there are no other sources to satisfy the applicable judgment.

Many planners therefore advise clients who wish to use single-member LLCs to have a separate member, which may be an irrevocable trust that is disregarded for income tax purposes so that the LLC can remain disregarded as well. Some planners have single-member LLCs formed in Delaware, Nevada, or other states that have legislation that is favorable to single-member LLC charging order protection, but there are no direct cases on point as to whether the law of another state can apply in a situation where the debtor (and the use, possession, and management of the underlying assets) are situated in a state that does not offer single-member LLC charging order protection.

While many advisors believe that the creditor holding a charging order can be taxed on income attributable to the member interest under partnership tax law, this is probably not the case. Louis Mezzullo’s Family Limited Partnerships and Limited Liability Companies BNA Portfolio 812 correctly states as follows:

While some commentators, relying on a revenue ruling dealing with an assignee of a partnership interest, believe a creditor with a charging order will be taxed on the income allocable to the interest subject to the order, it is more likely that the creditor will not suffer unfavorable tax consequences. Because any distributions from the entity to the creditor should be treated as a reduction in the amount owed to the creditor by the owner of the interest, under general tax principles the owner of the interest would recognize the income.

The Florida statutes on charging order protection for both limited liability companies and limited partnerships can be viewed by clicking here for LLCs and here for LPs.

*************

[1] Rothwell v. Fertman, Order re Motion and Application to Charge Partnership Interest. Civil Action 92 Z 1881, District Ct Colo. 1994.

Florida Automobile Liability and How to Protect Yourself, Your Business, and Your Family

by Alan Gassman

Malpractice lawsuits are not the only source of concern for a physician, particularly one who is directly invested as a partner or owner in a physician group or practice. Many physicians and their families will have wealth-threatening automobile accidents (personal or business-related) because of insufficient insurance coverage, gaps in coverage, or incorrect vehicle ownership or use planning.

An individual or company can be responsible for injuries sustained by people in an automobile accident in several ways that are often not recognized or expected:

- The driver of an automobile is responsible for his or her own negligence, and negligence is in the eyes of a generous jury.

Having plenty of motor vehicle and umbrella liability insurance coverage is the best way to help assure that a person with significant assets can settle an automobile accident lawsuit within policy limits and without risk to personal assets.

Typically, the automobile liability insurance policy will cover $500,000 per accident, and then the separate umbrella liability policy may be purchased in increments of $1,000,000, not exceeding $5,000,000 with most carriers.

It is important that the policy cover both personal and business/professional driving if the automobile is a corporate vehicle or is used in the business.

- Don’t get surprised: The car owner is responsible for the negligence of any permitted driver.

If you let someone drive your car, you are generally responsible for their negligence. This may include inexperienced teenage drivers, employees who use your car, and your spouse.

In Florida, if a driver has an accident in Florida and at least $500,000 of liability insurance coverage, an individual car owner is only liable for up to $100,000 per person, up to $300,000 per incident for bodily injury, and up to $50,000 per incident for property damage stemming from the negligence of a separate driver. The driver must be driving a Florida registered vehicle in the state. This exception will not apply, however, if the owner was negligent in allowing the driver to operate the vehicle (FL Statue § 324.021).

The Florida Statute described above does not specifically state what the insurance liability limits will be for a car owner where the driver has less than $500,000 of liability insurance. The law may limit the obligation of the vehicle owner to $500,000 for economic damages. If the driver has $250,000 of coverage, it is unclear whether the owner will be exposed for $250,000, or an entire $500,000.

With reference to the nullification of this Statute if the owner was negligent in allowing the driver to operate the vehicle, we had a client who was sued for allowing his honor student child to drive in the rain just a few months after receiving a driver’s license. The plaintiff lawyer alleged that out client was negligent for allowing an inexperienced driver to drive in the rain, and the client’s personal liability insurance carrier paid significant money to settle the claim. The client was lucky to have a separate policy, because his child resided with his ex-spouse, but drove a car that he had purchased.

- Statutory liability for the parent who signed the motor vehicle liability agreement for a minor driver.

The Florida Statutes require one of the parents of a driver who is under age 18 to sign on to responsibility for any negligence of the minor driver on the Florida roadways. In the past, we used to recommend to parents of minor drivers that their housekeeper or mother-in-law sign the consent form, but the Department of Motor Vehicles has been very strict in the past few years in requiring a parent’s signature.

Proper estate planning can make a physician client parent judgment proof and can sign the consent form without much concern, but other times the non-physician spouse has significant assets that may be exposed and is the parent with the time to go down to the DMV to sign for liability.

There is also a procedure for changing which parent has this responsibility.

Proper creditor protection planning recognized this significant liability and places assets and insurances in place to take these risks into consideration.

- An individual or business is responsible for the driving of an employee or hired agent.

Many clients have employees who run errands for the doctor personally or for the office, not realizing what kind of risk is involved each time an employee gets behind the wheel of the doctor’s or company car. If a nanny is driving at the request of the employer, the employer can be responsible for the accident caused by the nanny, even if the nanny is driving his or her own vehicle for the employer at the time.

It is important to have the nanny screened and explicitly listed on liability insurance policies for driving and homeowner events.

Corporations can obtain “unowned” automobile liability coverage, so that the insurance carrier will be responsible for liabilities incurred as the result of an employee or contractor accident.

- How about boats, wave runners, three wheelers, four wheelers and snowmobiles?

Many clients do not think through liability exposure resulting from recreational vehicles like boats, wave runners, ATVs, and snowmobiles. Often the best advice is to sell these vehicles and find other fun things to do, particularly if they are not used very often. Why not give these to your favorite niece or nephew, and then use them occasionally? The Florida laws on boat and airplane liabilities are slightly different than those for cars. The owner of a boat is only responsible for the negligence of his or her own piloting and the piloting of any person when the owner is on the boat with them. If you own a boat and someone else is driving, it is best that you not be on the boat. Even sleeping under the cabin will make the owner responsible for the negligence of the pilot! Many time clients do not realize their boats and other recreational vehicles are not covered under umbrella liability policies.

It is almost always best to have a large boat, airplane or other recreational vehicles owned under a limited liability company, for liability insulation and ease of transfer purposes. There is a 7% sales tax imposed upon the transfer of a car or boat in or out of a limited liability company or other entity, so properly planning ahead is important.

- Protection of the car itself: Who should own it?

An important question in vehicle planning is who should own or lease each car. Putting the car in the doctor’s name makes the car liable to be lost if the doctor is sued for malpractice. Florida law is not clear as to whether the above-referenced liability limitation applies where a car is jointly owned and one driver causes an accident.

Many times the non-physician spouse will own the car driven by the physician, as long as there is plenty of liability insurance.

Other times the car will be owned by the physicians who drives it, but subject to a 48 or 60 month car loan so that there would be little equity for a creditor to want.

Putting the car in a child’s name means the child will be unable to transfer the car until he/she reaches age 18.

Under Florida law, a car can be owned under tenants by the entireties if the Department of Motor Vehicles form is properly filled out, and the tenants by the entireties option is selected. Most often, however, we recommend having the car owned solely by the “less at risk” spouse as a result of the malpractice liability risk.

Where a car is going to be owned jointly as tenants by the entireties between spouses to protect the car’s value from creditors of either spouse, the word “and” needs to appear on the title instead of the word “or”, in order to assure tenancy by the entireties status. Typically we discourage married couples from owning cars jointly, because of the risk that an accident could cause exposure of all joint assets.

Cars might be placed under limited liability companies or other creditor protection vehicles, but this can cause extra expense and less coverage depending upon the insurance carrier(s), and their rules and pricing associated with business and personal vehicle ownership.

When a company owns a car, it does not have the benefit of the Florida $500,000 liability law described above. This is one disadvantage of titling a car or leased vehicle under a corporate entity, although there may be income tax deduction incentives to do so.

If you tell the IRS a car is used for business and you tell the insurance company it is used personally and there is an accident while the car is being used for business, will the insurance company pay?

To transfer ownership of a car, simply go to the tag and title office with the title and sign the back. Expect to pay sales tax if the transfer is to or from a corporation, and make sure insurance agencies have the right information on ownership. If there is a loan on the car, permission of the lender will be needed to make the transfer.

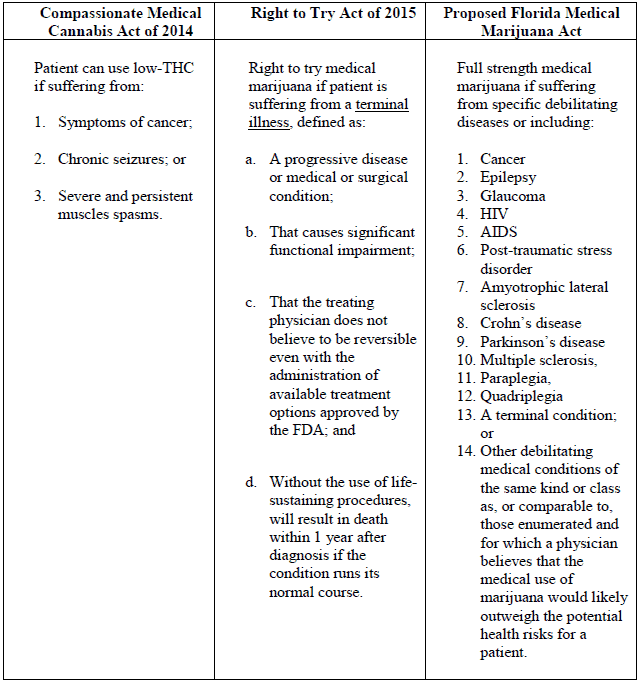

Florida Medical Marijuana Act Introduced

by Alan Gassman & Seaver Brown

On November 8, 2016, Florida voters overwhelmingly approved the Florida Medical Marijuana Legalization Initiative, also known as Amendment 2, with nearly 71 percent of them in support of the Amendment. Amendment 2 will expand the use and availability of medical marijuana for those with specific debilitating diseases or medical conditions as determined by a licensed state physician.[1]

Nevertheless, the Florida Legislature and Department of Health have yet to provide any indication of when they will roll out the final rules and regulations for medical marijuana, leaving doctors, patients, and other caregivers without a solution to these chronic issues. The legislature must hash out the rules that will regulate if and when medical marijuana can be prescribed for those medical conditions set forth in Footnote 1, but before doing so should take a deep breath in order to decide exactly how they are going to what they are going to do. Lawmakers are acutely aware that many issues will stem from these new rules.

On March 7, representatives Jeff Brandes of Pinellas, Darryl Ervin Rouson of Pinellas and Hillsborough Counties, and Greg Steube of Sarasota and Charlotte Counties introduced Senate Bill No. 614, known as the Florida Medical Marijuana Act (“FMMA”).

In a press release accompanying the Act, Senator Brandes stated that the FMMA would effectively repeal Florida’s current medical marijuana laws and “replace them entirely with a broader set of regulations designed to encourage more participation from medical marijuana providers.” Senator Brandes believes that Florida’s current medical marijuana laws “promote a state-sanctioned cartel system that limits competition, inhibits access, and results in higher prices for patients. Florida should focus on what is best for patients.” The authors could not agree with him more, and applaud his efforts to bring new heights of medical treatment to deserving Floridians and investment opportunities for a budding industry.

However, until the FMMA is adopted, doctors are still permitted to prescribe medical marijuana and low-THC products to patients suffering from diseases or medical conditions under the very restrictive Compassionate Medical Cannabis Act of 2014 (CMCA) and Right to Try Act of 2015 (RTTA).

The 2014 CMCA allows individuals suffering from cancer, chronic seizures, or severe muscles spasms to use low-THC, which contains less than 0.8 percent of tetrahydrocannabinol (the psychoactive compound found in marijuana). Allegedly, this provides all the medical benefits of medical marijuana without the euphoric feeling one obtains from ingesting normal marijuana plant leaves by smoking or eating, which contain an average of 20 percent THC.

The 2015 RTTA allows patients with a terminal illness[2] to use medical cannabis, which is derived from the whole plant and includes the psychoactive compound, THC. THC apparently induces an altered state of consciousness that allows many patients to escape the conscious feeling of pain, and apparently enhances the living experience in many ways for those who have used and encouraged it.

**************

[1] These diseases include: cancer, epilepsy, glaucoma, HIV, AIDS, post-traumatic stress disorder, amyotrophic lateral sclerosis, Crohn’s disease, Parkinson’s disease, multiple sclerosis, paraplegia, quadriplegia, a terminal condition, or other debilitating medical conditions of the same kind or class as, or comparable to, those enumerated and for which a physician believes that the medical use of marijuana would likely outweigh the potential health risks for a patient.

[2] Defined as, “a progressive disease or medical or surgical condition that cause significant functional impairment, is not considered by a treating physician to be reversible even with the administration of available treatment options currently approved by the FDA, and, without the administration of life-sustaining procedures, will result in death within 1 year after diagnosis if the condition runs its normal course.” Florida Statue § 499.0295.

Making Systems Part of Your Company Culture

by David Finkel

David Finkel is the Wall Street Journal bestselling author of SCALE: Seven Proven Principles to Grow Your Business and Get Your Life Back, which can be viewed by clicking here. As the CEO of Maui Mastermind, he has worked with 100,000+ businesses coaching clients and community members to buy, build, and sell over $5 billion worth of businesses.

Today I want to share with you what I think are the core concepts you need to make systems thinking (both creating and using them) an integral part of your company culture.

First, let’s be clear: Building systems can’t be a one-person, one-time effort. It’s got to be an ongoing company-wide culture of creating, using, organizing, refining, and if need be, deleting your business systems.

Likely this will mean you’ll need to train your team to participate in the systematization of your business since many of your new team members will have little or no training in the importance, creation, and refinement of systems. In fact, some will instead see systems as a hassle or an impediment.

It’s your job to help them recognize how useful systems can be to get their jobs done—and how critical they are to the long-term success of the business.

One of your key leadership responsibilities is to establish the discipline and culture of creating and using systems in your organization.

Click here to read the full article.

Follow David on Twitter: @DavidFinkel.

Richard Connolly’s World

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature some of Richard’s recommendations with links to the articles.

This week, the article of interest is “One Lawyer, 6,905 Hours Leads to $1.5 Million Bill in Sprint Suit” by Joe Palazzolo and Sara Randazzo. This article was featured WSJ.com on March 13, 2017.

Richard’s description is as follows:

Alexander Silow, a contract lawyer for a Pennsylvania plaintiffs’ firm, clocked 6,905 hours of work on a shareholder lawsuit against former executives and directors of Sprint Corp. related to its 2005 merger with Nextel. Averaging about 13 hours a day, Mr. Silow reviewed 48,443 documents and alone accounted for $1.5 million, more than a quarter of the requested legal fees, according to court documents.

“Unbelievable!” is how Judge James Vano in Kansas described the billing records. And he meant it.

“It seems that the vast amount of work performed on this case was illusory, perhaps done for the purpose of inflating billable hours,” Judge Vano, who sits in Olathe, Kan., wrote in a Nov. 22 opinion.

Judge Vano’s ruling might have gone unnoticed but for a recent disclosure about Mr. Silow by the law firm where he worked: He was disbarred in 1987 and practiced law illegally for decades.

Please click here to read this article in its entirety.

Humor! (Or Lack Thereof!)

The Facts in the Case of the Great Beef Contract

by Mark Twain

John Wilson MacKenzie entered into a contract with the General Government to supply thirty barrels of beef to General Sherman. After eight failed attempts to fulfill the contract with General Sherman, MacKenzie was tomahawked and scalped by Native Americans, who took all but one barrel of his beef. Over the coming years, several people inherited the contract but all died before they could receive the payment due to MacKenzie. Eventually, it landed in the hands of a man who, after many failed attempts to collect the payment owed, learns that the Government will likely pay for only the one barrel of beef General Sherman received, and not the other 29 the Native Americans ate. Exhausted, he gives up bequeathing the contract to a young clerk in the Corn-Beef Bureau who also dies before he can collect payment.

Click here to read the entire story of the Great Beef Contract by Mark Twain.

**********************************************************

Thank you for your e-mail.

I’m at the Magic Kingdom today.

Debbie, Shelley and the others got to stay.

If you need assistance, just send them an email

(Debbie@gassmanpa.com and Shelley@gassmanpa.com)

They are here to help and always prevail.

I’m speaking to doctors for CME.

We’re talking about finances, taxes, lawsuits, and other things they have to see.

I reflect periodically,

On our national oddity.

Hoping that legislative change

Will treat doctors in a way not deranged.

The contribution they make, let’s please not forsake.

Their skills for decades were rehearsed.

And keep us from riding around in a hearse.

Paperwork requirements have come in like a rash.

Of red tape that only the Red Sea might cure in much less than a flash.

So let’s toast the dedication of physicians old and new.

And I’ll try to help them from catching any financial or legal flu.

Thanks to MER, the Bahamas, and New York.

If you’d like to see these presentations there in October or November, let’s talk.

**********************************************************

Sign Sayings of the Week

**********************************************************

In the News

by Ron Ross

The White House Press Secretary will have his own cooking show—“Spicier with Sean Spicer”. Watch as Sean refuses to accept the premise of the food pyramid and starts an argument with a ham salad

After studying the Republican Health Plan, the CBO projects 20,000,000 people will lose coverage. Trump Administration responds with a temporary ban on Arabic numerals.

**********************************************************

**********************************************************

Upcoming Seminars and Webinars

Calendar of Events

**********************************************************

Just Announced!

FREE LIVE WEBINAR FOR THE AAA-CPA STUDY GROUP

Alan and Marty Shenkman will present a free one and one-half hour webinar concerning a practical model for rendering asset protection planning services to more clients, more efficiently and more effectively using a construct called the “Asset Protection Planning Continuum.”

The program is intended for practitioners with moderate asset protection planning knowledge so that they can expand that knowledge in a practical way that will assist them to better help their clients, whatever the nature and focus of their practice may be.

Date: Thursday, June 22, 2017 | 2:00 – 3:30 p.m. (Eastern)

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE NAPLES PRESENTATION:

Alan will be speaking at the STEP Chapter Meeting in Naples, Florida. His topic for this event is FLORIDA CREDITOR EXEMPTION LAW PLANNING UPDATE. He will speak on April 19 from 12:00 to 12:45 p.m.

STEP is a global professional association for practitioners who specialize in family inheritance and succession planning. STEP members help families plan for their futures, from drafting a will to advising on issues concerning international families, protection of the vulnerable, family businesses and philanthropic giving.

Date: Wednesday, April 19, 2017 | 12:00 – 12:45 p.m. (Eastern)

Location: McCormick & Schmick’s Restaurant in Naples, Florida

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE ESTATE PLANNING DISCUSSION AT FLORIDA STATE UNIVERSITY SCHOOL OF LAW

Alan will appear via Skype with professors Steven Hogan and Bob Pierce to give his views, by interview style, for their estate planning course at Florida State University School of Law on Thursday, March 23, 2017.

Date: Thursday, March 23, 2017 | 1:15 – 3:00 p.m. (EASTERN)

Location: Florida State University School of Law

Additional Information: To receive a live call in code or videotape of this presentation, which we will qualify for continuing legal education credit, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE FLORIDA BAR CLE SEMINAR

Alan will be speaking at the 2017 Annual Wealth Protection Program presented by the Florida Bar and the Continuing Legal Education Committee. Alan will discuss EXEMPTION AND FLORIDA PLANNING 2016 – MORE THAN WHAT YOU THOUGHT, AND LESS THAT WHAT YOU WISH FOR.

Additional topics and speakers include:

- Key Asset Protection Strategies Integrations & Estate Planning Techniques and Wealth Management Products – Denis Kleinfeld

- Important Recent Developments and trends in Debtor Creditor Law – Including Discussion of the Uniform Voidable Transfers Act – Michael Markham & Arthur Neiwirth

- The Secrets to Avoiding the Tricks and Traps in Partnership Tax Planning – Jerry Hesch

- Critical Factors Every Florida Planner Must Know in Using Offshore Asset Protection Strategies – Les Share

- Trends in Practice – The Growing Oppurtunties for Skilled Wealth Protection Professionals Important Wealth Protection Cases, Law and Trends of Practice – What Happened and Where Are We Going?

Date: Friday, April 7, 2017 | 8 a.m. to 5 p.m.

Location: Hyatt Regency Downtown Miami – 400 SE Second Avenue, Miami, FL 33131

Additional Information: For more information, please email Alan at agassman@gassmanpa.com. To register, visit www.floridabar.org/CLE and use the Course Number: 2332R. A webcast will be available by clicking here.

**********************************************************

LIVE NAPLES PRESENTATION:

Please put Friday, April 28th, 2017 on your calendar to enjoy the 4th Annual Ave Maria School of Law Estate Planning Conference and the weekend that follows in Naples.

Alan will be speaking at this conference on the topic of THE ETHICS OF AVOIDING TRUSTS AND ESTATE LITIGATION.

Alan will also appear on a panel of speakers with Jerry Hesch and Lester Law on the topic of TAX PLANNING WITH LIFE INSURANCE PRODUCTS, RECENT LITIGATIONS, AND OTHER HOT TOPICS.

Other speakers and topics include the following:

- Stacy Eastland – Comparing Freeze Techniques

- Jonathan Gopman – Asset Protection Trusts: An Update and Discussion of Planning

- Joan Crain – Challenges for Trustees in Dealing with Millennial Beneficiaries

- Jerry Hesch – Passing a closely-held business on to junior family members or key employees or co-owners: An analysis of the income tax, estate tax and financial impact of business succession planning techniques.

- Jerry Hesch & Alan Gassman – Life Insurance Planning Panel – Techniques, Tax Planning and The Good, the Bad, and the Ugly

- Tae Kelley Bronner – Homestead Planning and Update

- Lester Law – Basis Consistency for Estate and Income Tax Planning Purposes, and Multiple Implications Thereof.

- Marve Ann Alaimo & Dixon Miller – International Estate Planning Rules and Planning Opportunities

- Susan Cassidy, M.D. – What You Need to Know for Your Client’s Medical Issues: Competency, Great Care Versus the Mainstream, What Medicare Recipients Should Seek Outside of the Medicare System, End of Life Communications and Planning and How Will the Above be

- Alan Gassman – Ethical Considerations to Avoid Estate and Trust Litigation and Family Disputes, and the 10 or so Avoidance Techniques You Should Be Actively Using

- Suzy Walsh – Special Needs Trusts Essentials and Well Beyond

Date: Friday, April 28, 2017

Location: The Ritz-Carlton Golf Resort | 2600 Tiburon Drive, Naples, FL, 34109

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE LAS VEGAS PRESENTATION:

AICPA ADVANCED PERSONAL FINANCIAL PLANNING CONFERENCE

Alan will be speaking at the Advanced Personal Financial Planning Conference, sponsored by The American Institute of CPAs. His topic for this event is LIFE INSURANCE TIPS FOR THE FINANCIAL PLANNING PROFESSIONAL. He will speak on June 14 from 10:50 to 11:40 a.m.

This conference is part of the AICPA ENGAGE event, which brings together five well-known AICPA conferences with the Association for Accounting Marketing Summit for one, four-day event. The conferences included in ENGAGE are Advanced Personal Financial Planning, Advanced Estate Planning, Tax Strategies for the High-Income Individual, the Practitioners Symposium/TECH+ Conference, the National Advanced Accounting and Auditing Technical Symposium, and the Association for Accounting Marketing Summit.

Date: June 12th – June 15th, 2017 | Alan’s speaks on June 14 from 10:50 to 11:40 a.m.

Location: MGM Grand | 3799 S. Las Vegas Blvd., Las Vegas, NV, 89109

Additional Information: For more information, please email Alan at agassman@gassmanpa.com or click here.

**********************************************************

LIVE NAPLES PROFESSIONAL ACCELERATION WORKSHOP

Alan will present a Professional Acceleration Workshop at Ave Maria School of Law.

Date: Friday, August 25, 2017 | 10:00 a.m. Eastern

Location: Ave Maria School of Law, Naples, FL.

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com. More details will be provided in the future, but please plan to attend.

**********************************************************

LIVE NEW PORT RICHEY PRESENTATION:

Alan will present AN ESTATE PLANNER’S UPDATE AND HOT TOPICS for the Charitable Consortium.

Date: Thursday, September 14, 2017 | 12:00 p.m. Eastern

Location: TBD

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com.

**********************************************************

LIVE PRESENTATION:

ESTATE PLANNING COUNCIL OF NORTHEAST FLORIDA

Please put Tuesday, September 19, 2017 on your calendar to enjoy a dinner conference for the Estate Planning Council of Northeast Florida.

Date: Tuesday, September 19, 2017

Location: TBA

**********************************************************

LIVE PRESENTATIONS:

2017 MER CONTINUING EDUCATION PROGRAM TALKS FOR PHYSICIANS

Alan will be speaking at the following Medical Education Resources (MER) events:

- October 20th – October 22nd, 2017 in New York, New York

- November 30th – December 3rd, 2017 in Nassau, Bahamas

His tentative topics for these events include the 10 Biggest Mistakes Physicians Make in Their Investments and Business Planning, Lawsuits 101, 50 Ways to Leave Your Overhead, and Essential Creditor Protection and Retirement Planning Considerations.

Date: New York: October 20th – 22nd, 2017Nassau: November 30th – December 3rd, 2017

Location: New York: To be determined.

Nassau: Atlantis Hotel | Paradise Beach Drive, Paradise Island, Bahamas

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE ESTATE PLANNING COUNCIL OF NORTHEAST FLORIDA PRESENTATION:

Alan will be speaking for the Estate Planning Council of Northeast Florida on March 20, 2018 on the topic of DYNAMIC PLANNING STRATEGIES FOR THE SUCCESSFUL CLIENT. This will be Alan’s third visit to Pensacola, and a welcome treat. Watch this space, as more details will be forthcoming!

Date: Tuesday, March 20, 2018

Location: To Be Determined

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

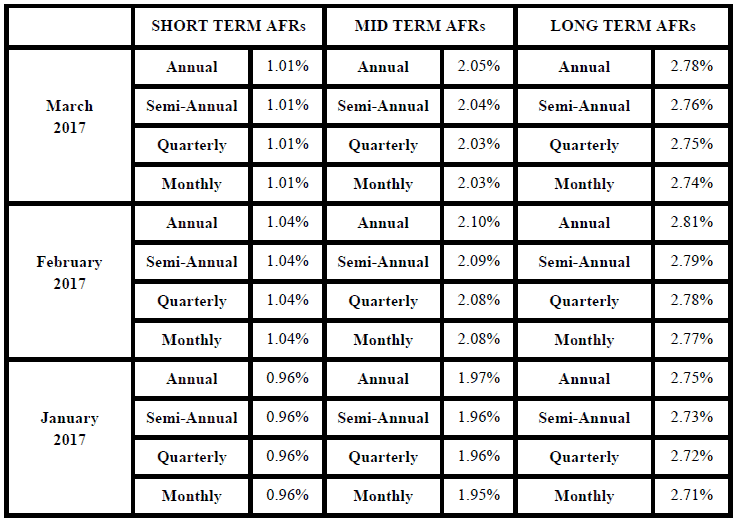

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.