The Slim Pickens Report – Issue 338

|

|

|||||||||||||||||||||||||||||||||||||||||||||

|

The Thursday Report Presents:

Slim Pickens was born on this day in 1919. Louis Burton Lindley, Jr., better known by his stage name Slim Pickens, was an American actor and rodeo performer. |

|||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||

|

Thursday, June 29, 2023Issue #338Coming from the Law Offices of Gassman, Denicolo & Ketron, P.A. in Clearwater, FL. Edited By: Wesley Dickson Current Events Florida Bar Journal Article

We are pleased to share that the Florida Bar Journal printed the article entitled, Designing Trust systems for Florida Residents: Planning Strategies, Things You Should Know, and Traps for the Unwary, in the June edition of the Florida Bar Journal. You can read the article on the Florida Bar Journal website by clicking here. Special thanks to recent Stetson Law School graduates Brock Exline and Peter Farrell who are both joining our law firm and pursuing LLM tax degrees at the University of Florida. Some key concepts from the article are as follows:

Creditor Planning: A common misconception is that since a revocable trust avoids probate, it also protects the assets inside the trusts from the settlors’ debts and creditors. It is noteworthy that Florida Statute Section 736.0505(1)(a) specifically permits creditors of the settlor of a revocable trust to reach assets within a revocable trust during the settlor’s lifetime to the extent the property would not otherwise be exempt by law if owned directly by the settlor. Although not subject to probate administration, revocable trusts will typically be accessible to creditors to satisfy a judgment debt. It is well established that assets in a revocable trust are included in the settlor’s gross estate for federal estate tax purposes,[1] and Florida Statute Section 733.707 permits creditors to reach assets that pass through an individual’s estate.

Scrivener Provision: A scrivener provision is important to have in a trust because it gives our law firm or another law firm chosen by the client the power to correct clerical errors or other issues to ensure that the intentions of the Grantor are carried out. Typically, to protect from misuse, the provision indicates that the Scrivener Protector can only act with the consent of one or more individuals named in the provision.

Tenancy by the Entireties: Most readers know that Florida is one of the few states[2] that provide “pure protection” for all kinds of tenancy by the entireties assets. Tenancy by the entireties assets are those which possess the following six “unities:” (1) unity of possession; (2) unity of interest; (3) unity of title; (4) unity of time; (5) survivorship; and (6) unity of marriage. “Pure protection” of those assets means that creditors owed money by one spouse cannot reach tenancy by the entireties assets, which can include real estate, physical objects, and intangible assets such as bank accounts, brokerage accounts, and contracts. These six unities can be complicated and may present traps for the unaware. The authors believe that the best way to draft a tenancy by the entireties revocable trust is to provide that the beneficial ownership interest of the married couple as grantors and sole lifetime beneficiaries is itself a tenancy by the entireties asset that will be completely owned and controlled by the surviving spouse.

Moving from Community Property Jurisdiction to FL: Many Floridians have moved to Florida after living in community property states where they have accumulated assets from earnings. Many of these individuals are unaware of the advantages and disadvantages of leaving their assets in the community property mode. Individuals can leave assets in community property under applicable case law and synthetically under the Uniform Disposition of Community Property Rights at Death Act, adopted by Florida in 1992.[3] Additionally, Florida adopted the Florida Community Property Trust Act in 2021, which enables a married couple living anywhere in the world to establish a Florida community property trust that must have at least one Florida-based trustee and must benefit only the married couple during their joint lifetime. In simulating traditional community property, the Florida community property trust must provide that half of the assets will pass as if coming from the first dying spouse and that the other half will be considered owned by the surviving spouse. Unlike most community property jurisdictions, the creditors of one spouse, even on debts acquired during the marriage, may only reach that spouse’s half of the community property trust assets, making it less likely that a Florida community property trust will be respected as a mechanism to provide a full step-up of income tax basis on the death of the first dying spouse, according to one noted authority.[4]

Separate Revocable Trust for Each Spouse: It is common in wealthy Florida estate plans to have separate revocable trusts for each spouse. Each trust becomes irrevocable on the death of the grantor spouse and becomes or empties assets into a credit shelter trust that can provide benefits for the surviving spouse without being subject to federal estate tax. This method also offers creditor protection, protection from divorce of a subsequent spouse, and the ability to leave assets into trusts that can benefit descendants without being subject to federal estate tax upon the subsequent death of such descendants, also known as “generation skipping trusts.” [1] I.R.C. § 2038(a) [2] Florida is joined by Alaska, Arkansas, Delaware, District of Columbia, Hawaii, Maryland, Massachusetts, Mississippi, Missouri, New Jersey, Oklahoma, Pennsylvania, Rhode Island, Tennessee, Vermont, Virginia, and Wyoming. Thakur, Prashant. “List of States Having Tenancy by the Entirety.” Internal Revenue Code Simplified, 11 Oct. 2019, https://www.irstaxapp.com/list-of-states-having-tenancy-by-the-entirety/. [3] PROBATE, TRUSTS AND GUARDIANSHIPS—GENERAL AMENDMENTS, 1992 Fla. Sess. Law Serv. Ch. 92-200 (H.B. 1901) (WEST) [4] See Alan Gassman & Chris Denicolo – The Florida Community Property Trust: Rethinking Client Trrust Logistics with a New Powerful Catalyst, Leimberg Information Services, Inc., July 8, 2021. See also, Jonathan G. Blattmachr, Howard M. Zaritsky, and Mark L. Ascher, Tax Planning with Consensual Community Property: Alaska’s New Community Property Law. Are joint trusts better? For many clients a joint revocable trust will be a better solution than separate revocable trusts, but this needs to be looked at very carefully due to multiple considerations that are covered in the article. A Joint Exempt Step-Up Trust (JEST) can provide a full new fair market value income tax basis on the first death and full funding of a credit shelter trust for estate tax purposes from all trust assets up to the estate tax exemption limit. A Community Property Trust can also provide a step up in basis, as described above.

10% Cap Appellate court rules that the Florida 10% cap is lost when transfers are made to identically owned LLCs. Florida Property Tax Law provides that non-homestead property values cannot be increased by more that 10% a year for the non school board portion of Florida real estate for property tax purposes. The litigation in Dade County that we have reported on in the past was appealed. The appellate court agreed with the circuit court that a transfer to an LLC will trigger the tax. This may not be the case if there is a Nominee Agreement in place at the time of the transfer. We will write more about this later and invite question, comments and suggestions on the 10% cap.

|

|||||||||||||||||||||||||||||||||||||||||||||

|

Article 1Precious Metals Are Personal PropertyWritten By: P. Jill Ashley, Juris Doctorate Candidate, Stetson Law School Article 2Recent Developments in Real Estate Taxation?Written By: Kenneth J. Crotty, JD, LL.M. Article 3The Walton GRATWritten By: P. Jill Ashley, Juris Doctorate Candidate, Stetson Law School For Finkel’s FollowersThe Difference Between Doing a Task and Owning a TaskWritten By: David Finkel Free Upcoming WebinarsEuropean Investing Accounts & StructuresPresented by: Alan Gassman, JD, LL.M. (Taxation), AEP (Distinguished) and Remo Tiefenauer, BA, Executive MBA HSG Hot Topics & Recent Developments in Estate Tax PlanningPresented By: Alan Gassman, JD, LL.M. (Taxation), AEP (Distinguished) More Upcoming EventsYouTube LibraryHumor |

|||||||||||||||||||||||||||||||||||||||||||||

|

Article 1Precious Metals Are Personal Property – Under FL Probate Code (But Not FL Trust Code)

Written By: P. Jill Ashley, Juris Doctorate Canidate, Stetson Law School

Within the 2020 amendment of the Florida Probate Code, §731.1065 clarified that precious metals (including gold, silver, or platinum bullion or coins) which are held for their collectible, historical, artistic, or investment purposes, rather than as legal tender, are defined as tangible personal property. However, the Florida Trust Code (governing trusts) has not adopted this definition set forth under the Florida Probate Code (governing wills and intestate estates). This conflicting treatment between wills and trusts may lead to surprising results when a unintended residual beneficiary of tangible personal property (previously thought to consist of family photos, clothing, and similar personal items of minimal value) is now entitled under a decedent’s will to receive gold bars and silver coins from the estate. If you are domiciled in Florida and you own precious metals, you might want to specifically designate a beneficiary on those assets in both your trust and will documents, or otherwise include a provision in your trust document indicating that you want to exclude precious metals from the definition of tangible personal property in your estate. On a related side note, the owners of David Reynolds Jewelry & Coins in St. Petersburg, Florida led a grassroots effort to remove restrictions on dealers in precious metals by having gold, silver, platinum bullion excluded from the statutory definition of “secondhand goods.” Florida Governor Ron DeSantis recently signed House Bill 737 taking effect on July 1, 2023. Under the new law, licensed dealers are no longer required to put a 30-day hold on assayed and properly marked bullion products before offering them for resale.

|

|||||||||||||||||||||||||||||||||||||||||||||

Recent Developments in Real Estate Taxation Written By: Kenneth J. Crotty, JD, LL.M.

Part A: All Married Persons Are Exempt From Documentary Stamp Taxes on Transfers of Homestead Property. Congratulations to the newlyweds and oldlyweds alike! All married persons are exempt from documentary stamp taxes for deeds or other instruments that transfer encumbered homestead property between married spouses. Prior to the 2019 Amendment, this exemption applied only to spouses within their first year of marriage. After the 2019 Amendment, the exemption is available for all married persons. Generally, documentary stamp taxes are taxes imposed on deeds and other documents that transfer an interest in real property in Florida. Transfers or conveyances subject to documentary stamp taxes are governed by §201.02 of the Florida Statutes. Except in Miami-Dade County, documentary stamps are taxable in Florida counties at a rate of $0.70 for every $100 of consideration. Consideration may include the amount paid for the property, the discharge of an obligation, and/or the unpaid balance of an underlying mortgage. The tax is paid to the clerk of court if the document evidencing the transfer of title is recorded, or the Florida Department of Revenue if the document is not recorded. There are limited exemptions to the tax, which are laid out in the statute. In 2018, an Amendment created a new exemption for transfers or encumbered homestead property between newlywed spouses within the first year of marriage. This was known as the Newlywed Exemption. Under §201.02(7)(b) of the 2018 Amendment, a deed between spouses is not subject to documentary stamp taxes if the transferred real property is homestead property, the only consideration for the transfer is the balance of an underlying mortgage or other lien encumbering the homestead property, and the deed is recorded within one year after the date of marriage. The transfers or conveyances may be from one spouse to the other spouse, from one spouse to both spouses, or from both spouses to one spouse. The 2019 Amendment removed the language requiring that the deed be recorded within one year after the date of marriage. Thus, married couples can take as much time as they need to transfer real property among themselves. Part B: Homestead Tax Exemptions For Landlords Only Apply to Portions of the Property Considered to be the Landlord’s Residence. With respect to landlords renting portions of the property they are living on and claiming as homestead, the Florida Supreme Court held in Furst v. Rebholz that the homestead tax exemption only applies to the portion of the property that is considered to be the landlord’s residence (not the portion that is being rented). In Furst v. Rebholz, the landlord was renting out a portion of his property. The property appraiser concluded the rented portion was at least fifteen percent of the total property, and that the rest of the property was the landlord’s residence. The Court held that the landlord may only be granted the homestead tax exemption for the portion of the property that is being used as the landlord’s residence, and that the rented out portion of the property is not eligible for the homestead tax exemption. The implications of this ruling limit the homestead tax exemption for landlords who live on the property and rent out certain portions of it. Rather than being able to claim the homestead tax exemption on the entire property, the exemption only applies to the portion of the property that is deemed to be the landlord’s residence. If the landlord gives a tenant exclusive use of a portion of the property and reserves himself to only the access rights of a landlord, these portions of the house are not part of the landlord’s residence, and are therefore not eligible for the homestead tax exemption. For example, assume a landlord rents out one room of the house the landlord resides in. The kitchen, bathrooms, and shared areas of the house are all still considered to be the landlord’s residence. However, the tenant’s room is a portion of the house which the landlord has no access to. Therefore, the percentage of the property that is made up of the tenant’s room is not eligible for the homestead tax exemption. This ruling will affect all landlords who rent out portions of their homesteads. The homestead tax exemptions for such landlords will be reduced by the percentage of the property that is not their residence, which is the portion of the property that the tenant has exclusive rights to. Part C: Properties Are Subject to Reassessment upon Transfer to Disregarded Entities. When a property owner transfers the property to a disregarded entity that they also own, such as a wholly owned LLC, the property is subject to reassessment upon the transfer to the disregarded entity, In S and A Property Investment Services, LLC, v. Pedro J. Garcia, etc., et. al., a married couple transferred their non-homestead property to a disregarded LLC that they owned 100% of. The property was then reassessed and did not receive the 10% Assessment Limitation because it had been transferred. As a result, the value of the property drastically increased, increasing the couple’s property tax liability. The Third District Court of Appeals for the State of Florida held that the transfer of the property to the disregarded LLC constituted a change of ownership and, therefore, the 10% Assessment Limitation was not required and the new, significantly higher property value was correctly assessed. Assessment of non-homestead residential properties under §193.1554 has four exceptions for transfers of property which are stated in §193.1554(5). Pursuant to the statute, there is no change of ownership if: (a) The transfer of title is to correct an error; Unless the non-homestead property transfer falls under one of these four exceptions, the property will be reassessed and not benefit from the 10% Assessment Limitation. For example, in the case above, the property was bought in 2000, and benefitted from the 10% Assessment Limitation through 2019, when it was valued at just over $100,000. The following year, it was reassessed without the 10% Assessment Limitation, and was valued at nearly $275,000. To continue receiving the benefits of the 10% Assessment Limitation, it is imperative that the transfer of the property falls under one of the four exceptions to §193.1554. Otherwise, the land will be reassessed without the 10% Assessment Limitation and the value of the property may drastically increase, subsequently increasing the property taxes associated with the property.

|

|||||||||||||||||||||||||||||||||||||||||||||

Article 3The Walton GRAT

Written By: P. Jill Ashley, Juris Doctorate Canidate, Stetson Law School

The billionaire Walton family is known in legal circles for more than founding Walmart stores. The Walton GRAT is an estate planning strategy named after Audrey Walton who transferred large positions of her Walmart stock into two Grantor Retained Annuity Trusts (GRATs) in 1993 in exchange for an annuity stream payable back to her for the two-year terms of each trust (the “Retained Term”). Walton named a daughter as the remainder beneficiary on each trust. Typically, the mechanics of a properly structured GRAT suggest that the assets transferred to the irrevocable GRAT can avoid estate inclusion if the Grantor survives the Retained Term of the GRAT, so that any remaining balance at the end of the Retained Term can pass estate tax free to the named beneficiaries. Furthermore, the assets transferred to the irrevocable GRAT would not be deemed taxable gifts, and therefore would not use the Grantor’s lifetime Gift Tax exemption if the assets funding the trust are set to equal the actuarial present value of the Grantor’s retained annuity interest. (Though some advisors suggest structuring the transaction to trigger a small taxable gift and filing a Gift Tax Return to trigger the three-year Statute of Limitations to manage IRS valuation challenges). In theory, using the IRS mortality tables and applying the appropriate Sec. 7520 interest rate to the trust’s annuity payouts can zero-out a remainder gift value to beneficiaries. In reality, when the assets held in the trust (here, Walmart stock) appreciate in excess of the required Sec. 7520 rate, there is a possibility of significant assets passing to the beneficiaries free of gift tax at the end of the retained term. On the flip side, when the trust assets underperform the Sec. 7520 rate, then all of the assets are pulled back into the Grantor’s estate. Pre-Walton, if the Grantor died before the end of the GRAT’s retained term, then the remainder interest in the annuity would have been included in the Grantor’s estate under I.R.C. Sec. 2039. But in 2000 the tax court held in favor of Walton[1] averring that Walton’s asset transfers were properly valued upon creation of the GRATs, properly structured as irrevocable trusts prohibiting additional contributions or commutation of her interest, and specified that annuity payments could only be made to Walton or to her estate for the duration of the retained term. A key provision in the trust and Walton’s corresponding estate documents indicated that any remaining annuity payments after her death would be payable to her estate instead of passing to beneficiaries before the retained term ended. The tax court averred the retained annuity was valid for the specified term of years, rather than passing to beneficiaries in a shorter period upon Walton’s death. In 2020, a U.S. Appellate Court affirmed in favor of the IRS to include the full value of a GRAT in the estate of Grantor, Patricia Yoder, when she died shortly before the end of a 15-year GRAT term.[2] As distinguished from Walton, however, this case involved bad facts, where Yoder was both the grantor and trustee of the GRAT which could make additional distributions to her upon request. More importantly, because the trust’s sole asset consisted of a partnership interest for making the annuity payments, Yoder’s interest was construed to provide her with continued enjoyment over the property though it was technically held by the irrevocable trust until her death. The court indicated that Yoder had not made a complete divestiture of her partnership interest. The court explained that under I.R.C. Sec. 2036(a)(1), Congress established three “strings” that tie a Grantor to a property interest for estate tax inclusion purposes: possession, enjoyment, or a right to income from the property. The executor of the Yoder estate failed to put forward any compelling arguments other than stipulations that Yoder sometimes received principal in addition to income in the annuity payments, and the executor failed to cite any legal authorities in the assertions. |

|||||||||||||||||||||||||||||||||||||||||||||

|

For Finkel’s FollowersThe Differnce Between Doing a Task and Owning a Task |

|||||||||||||||||||||||||||||||||||||||||||||

Free Saturday WebinarPROTECTING YOUR BUSINESS AND YOUR FAMILY: ESTATE PLANNING, CREDITOR PROTECTION AND ESTATE TAX PLANNING FOR BUSINESS PROFESSIONALSDate: Saturday, July 1, 2023 Time: 11:00 AM to 12:00 PM EST (60 minutes) Presented by: Alan Gassman, JD, LL.M. (Taxation), AEP (Distinguished)

REGISTER HERE FOR 1.0 CPA CPE CREDIT REGISTER HERE FOR NON-CPE CREDIT REGISTER HERE FOR FLORIDA CLE CREDIT

Please Note: After registering, you will receive a confirmation email containing information about joining the webinar. Approximately 3-5 hours after the program concludes, the recording and materials will be sent to the email address you registered with. Important: If you are already on the “Register For All Upcoming Free Webinars” list, you will be auto-registered on Friday for non-CPE credit. If you would like 1.0 free CPE Credit for this webinar, please also register above through CPA Academy. If you would like Florida CLE Credit, please register above through the provided link above. Please email registration questions to info@gassmanpa.com. |

|||||||||||||||||||||||||||||||||||||||||||||

|

Free Upcoming Webinars

EUROPEAN INVESTING ACCOUNTS & STRUCTURESDate: Saturday, July 15, 2023 Time: 11:00 AM to 12:00 PM EST (60 minutes) Presented by: Alan Gassman, JD, LL.M. (Taxation), AEP (Distinguished) and Remo Tiefenauer, BA, Executive MBA HSG

REGISTER HERE FOR 1.0 CPA CPE CREDIT REGISTER HERE FOR NON-CPE CREDIT REGISTER HERE FOR FLORIDA CLE CREDIT

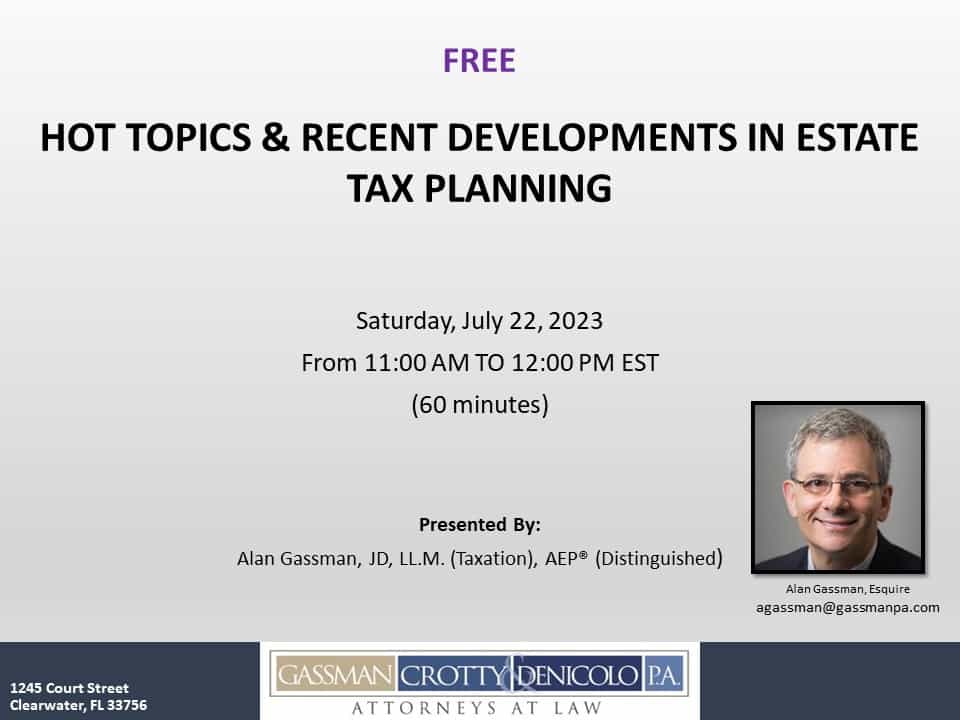

Please Note: After registering, you will receive a confirmation email containing information about joining the webinar. Approximately 3-5 hours after the program concludes, the recording and materials will be sent to the email address you registered with. Important: If you are already on the “Register For All Upcoming Free Webinars” list, you will be auto-registered on Friday for non-CPE credit. If you would like 1.0 free CPE Credit for this webinar, please also register above through CPA Academy. If you would like Florida CLE Credit, please register above through the provided link above. Please email registration questions to info@gassmanpa.com. HOT TOPICS & RECENT DEVELOPMENTS IN ESTATE TAX PLANNINGDate: Saturday, July 22, 2023 Time: 11:00 AM to 12:00 PM EST (60 minutes) Presented by: Alan Gassman, JD, LL.M. (Taxation), AEP (Distinguished)

REGISTER HERE FOR NON-CPE CREDIT REGISTER HERE FOR FLORIDA CLE CREDIT

Please Note: After registering, you will receive a confirmation email containing information about joining the webinar. Approximately 3-5 hours after the program concludes, the recording and materials will be sent to the email address you registered with. Important: If you are already on the “Register For All Upcoming Free Webinars” list, you will be auto-registered on Friday for non-CPE credit. If you would like 1.0 free CPE Credit for this webinar, please also register above through CPA Academy. If you would like Florida CLE Credit, please register above through the provided link above. Please email registration questions to info@gassmanpa.com.

|

|||||||||||||||||||||||||||||||||||||||||||||

|

|

|||||||||||||||||||||||||||||||||||||||||||||

|

ALL UPCOMING EVENTS

|

|||||||||||||||||||||||||||||||||||||||||||||

|

YouTube Library

Visit Alan Gassman’s YouTube Channel for complimentary webinars and more! The PowerPoint materials can be found in the description box located at the bottom of the YouTube recording. Click here or on the image of the playlists below to go to Alan Gassman’s YouTube Library.

|

|

HUMOR

Born on this Day: Slim Pickens

Introduction: In the realm of entertainment, there are certain individuals whose unique talents and larger-than-life personalities leave an indelible mark on the industry. One such unforgettable entertainer is none other than Slim Pickens. Known for his cowboy roles, infectious charm, and unmistakable Texan drawl, Slim Pickens captured the hearts of audiences around the world with his memorable performances. Let’s take a closer look at the life and career of this remarkable entertainer. The Early Days: Slim Pickens, born Louis Burton Lindley Jr. on June 29, 1919, in Kingsburg, California, began his journey in the entertainment world with a passion for rodeo and horsemanship. As a young man, he traveled the rodeo circuit, showcasing his skills as a trick rider and roper. These early experiences not only honed his abilities but also served as the foundation for his future success in Hollywood. Breakthrough in Film: Pickens’ big break came when he was discovered by legendary director Howard Hawks, who cast him in the 1950 western film “Rocky Mountain.” From there, Pickens’ career took off, and he became a sought-after character actor in the western genre. His rugged looks, undeniable charisma, and knack for comedic timing made him a fan favorite. Memorable Roles: Slim Pickens’ name became synonymous with memorable performances in notable films. One of his most iconic roles came in Stanley Kubrick’s satirical masterpiece, “Dr. Strangelove or: How I Learned to Stop Worrying and Love the Bomb” (1964). His portrayal of Major “King” Kong, a B-52 bomber pilot, remains one of cinema’s most unforgettable characters. Who could forget his iconic ride on a nuclear bomb, waving his cowboy hat in the air? It solidified his place in cinematic history. Pickens’ career spanned over four decades, and he appeared in numerous Western films, including “One-Eyed Jacks” (1961), “Blazing Saddles” (1974), and “The Apple Dumpling Gang” (1975), among others. His ability to effortlessly switch between comedic and dramatic roles showcased his versatility as an actor. Beyond Acting: Slim Pickens’ talents extended beyond the silver screen. He was a beloved guest on various television shows, entertaining audiences with his infectious personality. Additionally, he lent his distinctive voice to animated characters, leaving an imprint on popular cartoons, such as “The Hound” in Disney’s “The Fox and the Hound” (1981). Legacy and Impact: Slim Pickens’ impact on the entertainment industry cannot be overstated. He brought a unique blend of rugged charm, authenticity, and humor to each role he played. His memorable performances continue to inspire and entertain audiences, and his name is forever etched in Hollywood history. Conclusion: Slim Pickens, with his unmistakable presence and memorable performances, left an indelible mark on the entertainment world. From his cowboy roles in classic Western films to his iconic performance in “Dr. Strangelove,” Pickens captivated audiences with his undeniable talent, infectious personality, and genuine Texan spirit. Though he has left this earthly stage, his legacy lives on, reminding us of the joy and laughter he brought to millions. Slim Pickens will forever be cherished as a true entertainer who knew how to make audiences smile, laugh, and appreciate the magic of the silver screen.

|

|

|

Gassman, Denicolo & Ketron, P.A. 1245 Court Street Clearwater, FL 33756 (727) 442-1200 Copyright © 2023 Gassman, Crotty & Denicolo, P.A |

|

|

|