Отчет четверг – 16.2.17 – Русское издание

Re: Русское издание

Using an LLC with Pay on Death Features and a Joint Revocable Trust to Assure Tenancy by the Entireties Ownership of Valuable Assets

Car 65 Where Are You? A Refresher for Trustees and Tax Advisors

An Editorial on Remote Witnessing – Does the Legislature Have Even the Remotest Idea?

Portability Trivia

The Antifragile Medical Practice by Pariksith Singh, M.D.

8 Tips to Better Manage Your Company’s Debt and Financing Relationships by David Finkel

Richard Connolly’s World – Inform Clients of Reporting Requirements for Charitable Gifts

Humor! (or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Alan at agassman@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Quote of the Week

“Those who fight corruption should be clean themselves.”

– Vladimir Putin

Vladimir Putin was born in modern day St. Petersburg, Russia, on October 7, 1952. In 1975 he graduated from his hometown university with a law degree and began his career in the KGB as an intelligence officer, where he was stationed in East Germany until 1990. Over the next four years Putin quickly rose to political power and became Anatoly Sobchak’s first deputy mayor.

In 1998 he was appointed to deputy head of management under Boris Yeltsin’s presidential administration, and was tasked with overseeing the Kremlin’s relations with regional governments. In 1999, Yeltsin fired his then serving prime minister, Sergey Stapashin, along with his cabinet and promoted Putin. Four months later, Boris Yeltsin resigned as president and appointed Putin as acting president until official elections could be held.

Putin went on to win the next election and served for two terms as president until 2008. Term limits prevented him from running in 2008, but his understudy, Dmitry Medvedev was elected as president that year and immediately appointed Putin as Russia’s prime minister. In 2012 Putin was re-elected to his third term as president despite widespread protests and allegations of electoral fraud, and unsurprisingly appointed Medvedev as prime minister.

Using an LLC with Pay on Death Features and a Joint Revocable Trust to Assure Tenancy by the Entireties Ownership of Valuable Assets

by John Crugerrand Lawyercamp a.k.a. “Put the Money in Trust and Run”

Please remember that this will not work in El Paso,

They are a community property state, so you will have to find a different lasso

Jackie and Diane – The Ultimate TBE Estate Plan

This is the story of Jackie and Diane.

A Florida couple who want an appropriate estate plan.

They met with a lawyer who recommended a Joint Trust.

But they also know that TBE is a must (tenancy by the entireties—to protect from creditors of either spouse).

They read the trust they were given, but it was a great big hassle.

The lawyer who wrote it wore a professor’s hat and tassel.

They were given an alternative—of owning assets directly in TBE.

But some were hard to title, and they only heard about probate avoidance on TV.

How do,

They make sure to avoid probate?

And not have a creditor of one

Take the money and run.

They went to see their childhood friend, Perry Mason,

Who had just finished a jury trial defending an entertainer named Jackie Gleason (it was a hostile work environment place suit brought by a group of aquatic swimmers).

Perry Mason said, “Why not set up a simple LLC?”

Which under Florida law can clearly be owned as TBE.

Then put your investments under the company that is formed.

It will be clear that this is pure TBE ownership, for if one or more creditors have swarmed.

And we can provide in the LLC Operating Agreement,

That your Revocable Trust becomes owner after the second death, unless the surviving spouse otherwise deemeth.

Because of the Florida case of Blechman v. Estate of Blechman,

Which indicates that an Operating Agreement can act like a pay on death mechanism to direct ownership, so the judge we thank him.

We’ll use a Conditional Assignment of ownership signed by both spouses and held in escrow,

In case they both get hit by a rice truck while navigating hills in Fresco.

But be cautious that the IRS

Could consider the LLC to be taxed as a partnership, and cause a mess.

If the LLC owns assets that should not be held that way,

Like S corporation stock, which should be kept away.

And while the Form 1065 instructions say that the LLC would be taxed as a partnership,

Many authorities disagree.

Rev. Proc. 84-35 indicates that if the tax result is the same,

In the vast majority of situations, there would be no IRS blame.

And if Jackie and Diane want even better creditor protection,

They could set up an Irrevocable Trust for their descendants that would be disregarded for income tax purposes and own part of the LLC to have charging order rights be the sole remedy of a creditor under Florida law, without exception.

This was a story about Jackie and Diane

Navigating areas that they didn’t understand.

They went to a good lawyer who gave them a hand,

The unconventional approach, coupled with relative simplicity and a good sense of concrete benefits gave them confidence they can understand.

Go on, take this strategy and run –

Jack & Diane

by John Cougar Mellencamp

A little ditty ’bout Jack & Diane

Two American kids growing up in the heart land

Jack he’s gonna be a football star

Diane debutante in the back seat of Jacky’s car

Suckin’ on chilli dog outside the Tastee Freez

Diane sitting on Jacky’s lap

Got his hands between her knees

Jack he says:

“Hey, Diane, let’s run off behind a shady tree

Dribble off those Bobby Brooks

Let me do what I please”

Saying oh yeah

Life goes on, long after the thrill of living is gone

Sayin’ oh yeah

Life goes on, long after the thrill of living is gone

Now walk on

Jack he sits back, collects his thoughts for a moment

Scratches his head, and does his best James Dean

Well, now then, there, Diane, we ought to run off to the city

Diane says:

“Baby, you ain’t missing nothing”

But Jack he says:

“Oh yeah, life goes on, long after the thrill of living is gone”

Oh yeah

He says: “life goes on, long after the thrill of living is gone”

Oh, let it rock, let it roll

Let the bible belt come and save my soul

Holdin’ on to sixteen as long as you can

Change is coming ’round real soon

Make us woman and man

Oh yeah, life goes on

A little ditty ’bout Jack and Diane

Two American kids doin’ the best they can

Car 65 Where Are You? A Refresher for Trustees and Tax Advisors

by Ken Crotty

It is important that beneficiaries be aware of the potential tax savings that could result if an irrevocable trust has not distributed all of its income during 2016 and the trust makes distributions during the first 65 days of 2017.

On a client’s death, the client’s revocable trust becomes irrevocable. Most client’s trusts are drafted to provide discretionary distributions of income and principal to the beneficiaries of the trust. If the trust generates income and makes distributions to the beneficiary, the distributions will carry the income of the trust out to the beneficiary. As a result, the beneficiary will report the income on his or her personal tax return instead of having the income reported on the trust’s income tax return.

There can be a significant tax benefit to having the income distributed out to the beneficiary rather than having it reported by the trust and having the trust pay the tax on the income because the tax brackets for trusts are very compressed compared to individuals. A trust will reach the highest tax bracket of 39.6% if the trust has more than $12,400 worth of income for 2016.

For irrevocable trusts, the trustee can make a distribution within the first 65 days of 2017 and deem such distribution to have occurred in 2016. As a result, even if a trust did not distribute all of its income in 2016, if the Trustee makes distributions during the 65 day period after the end of the year, such distributions will carry the income out to the beneficiary reducing taxable income of the trust. This tax planning opportunity is something that clients need to be aware of and should discuss with their tax advisors before the 65 day period ends. The tax savings can be significant.

By means of example, assume that the trust had $36,000 worth of taxable income during 2016, did not make any distributions to the beneficiary during 2016, and no distributions are made to the beneficiary during the first 65 days of 2017. Further assume that the beneficiary is single and had $60,000 worth of taxable income during 2016. The beneficiary will pay $10,778 of tax on the beneficiary’s $60,000 of income. The trust will pay $12,552 of tax on the trust’s $36,000 of income. As a result, the total amount of tax paid by the beneficiary and the trust would be $23,330 ($10,778 + $12,552 = $23,330).

If the income is distributed from the trust to the beneficiary in the first 65 days of 2017, then the beneficiary will have taxable income of $96,000. A single taxpayer will pay $19,924 of tax on this income. Because the trust distributed all of the trust’s income to the beneficiary, the trust will not pay any tax on its income. As a result, the total amount of tax paid by the beneficiary and trust will result in a tax savings of $3,406 ($23,330 – $19,924 = $3,406).

The results are even more significant for a taxpayer who is married filing a joint return. Based on the same assumptions, the married taxpayer would pay $8,076 of tax on the beneficiary’s joint personal return, resulting in a combined total of tax of $20,628 if the trust retained the $36,000 worth of income ($8,076 + $12,552 = $20,628). If the $36,000 of income is distributed to the beneficiary, the trust would not pay any tax and the beneficiary would pay $15,549 of tax on the $96,000 of income. This would result in a tax savings of $5,079 ($20,628 – $15,549 = $5,079).

An Editorial on Remote Witnessing – Does the Legislature Have Even the Remotest Idea?

by Alan Gassman

In the previous edition of the Thursday Report we featured an article on Florida’s newly proposed House Bill 206, which allows for the remote video witnessing and authorization of wills and trusts. On February 9, Alan spoke at the All Children’s Hospital Conference and had this to say about House Bill 206:

“From what I understand, the fix is on. “Big business” has contributed generously to campaign coffers in the Florida legislature. We are going to be one of the first states to adopt a new format that will enable us to witness and notarize a document that we see signed by video. I believe this is going to cause a lot of abuse. The statute calls somebody the “Qualified Custodian” who will follow all the rules in the statute. The trust mills that illegally draft documents are now going to advertise that they are Florida Statutory Compliant Qualified Custodians, so somebody can march grandma up in front of a camera, stand to the side and say, “grandma, you need to smile and sign this.” Now the non-lawyer is watching on video and observes the signing. Grandma could just click a button on her iPad and then it is a done deal.

We suggest that you call your legislature, call your governor, whatever you can do, but as I understand it, the fix is on.”

Portability Trivia

by Brandon Ketron & Alan Gassman

(Portability refers to the rules that allow the estate tax exemption of one spouse to be used by the surviving spouse under some circumstances. If you are not a tax professional skip to humor).

A review of the Portability Rules at the Heckerling Institute gives rise to the following trivia, which estate tax planning lawyers should perhaps be memorizing:

True or False:

- Under Section 20.2010-2(a), the portability election can only be made on a timely filed and complete estate tax return Form 706.

- Estates that are required to file the Form 706 ( i.e. estates that exceed the basic exclusion amount), will lose the portability allowance if the return is filed after the filing deadline (which is 9 months from date of death, or within 6 months after the filing deadline if a valid extension is filed). There is no way whatsoever around this if a return is not filed. A return is not considered to be filed unless it is a valid Form 706 that is actually signed by the fiduciary.

- The return may not be perfect, but if it is signed and filed, then it can be updated to save the election under some circumstances. There is no Form 706-EZ.

WHAT ASSETS NEED TO BE VALUED?

- If the estate tax return is required to be filed because of the value of the estate, then only assets increasing estate tax have to be valued with appropriate appraisals. Assets passing to a surviving spouse or charity do not have to be valued because those assets do not increase estate tax.

- Small estates will need appraisals where the value of the marital or charitable devise or devises will determine the value of the non-marital charitable assets, such as where the trust says “give my spouse $2,000,000 worth of assets and the rest will go to my children.”

WHEN CAN YOU GET 9100 RELIEF FOR A LATE FILED ESTATE TAX RETURN-OOPS

- 9100 relief will apply under Revenue Procedure 2014-18, if the estate is below the filing threshold (gross assets are less than the exemption amount) or a return was timely filed and the Portability Allowance was inadvertently elected out of.

- Typically, 9100 relief in most areas of the tax code will only be available if the taxpayer consulted with an advisor who gave wrong or insufficient advice. This is not being mentioned in the Private Letter Rulings being issued, and is an example of IRS leniency.

- For estates of descendants dying after January 1, 2014, the IRS may grant discretionary 9100 relief for estates with gross assets less than the exemption amount, which are not otherwise required to file a return, however no private letter ruling is required.

| Decedent who died prior to January 1, 2014 | Decedent who died on or after January 1, 2014 | |

|

Estates with Gross Assets under the Estate Tax Exclusion Amount ($5,490,000)

|

Relief may be granted under Revenue Procedure 2014-18 | Must file for 9100 relief |

|

Estates with Gross Assets over the Estate Tax Exclusion Amount, but no tax owed due to Marital Deduction or Charitable Deduction

|

No relief available | No relief available |

|

Estates Owing Estate Tax

|

No relief available | No relief available |

OTHER IMPORTANT PORTABILITY POINTS

- A) Where previous gifts by the decedent exceeded his or her exemption, the DSUE is reduced only by the previous exemption usage, and not by the excess gift that tax was paid upon. So if the decedent made a $5,600,000 gift in 2016 and paid gift tax on $150,000, the DSUE for a death in 2017 will be $40,000 ($5,490,000 minus $5,450,000)B) You can only use your first spouse’s DSUE, not the DSUE from subsequent spouses.

Planners should consider funding a hybrid asset protection trust to make use of the DSUE while having the assets available for the surviving spouse if needed – Under a hybrid asset protection trust the spouse is not named as a beneficiary but may be added by Trust Protectors if certain events occur.

Answers:

- True

- True

- True

- False – ALL ASSETS must be valued, even if there is no estate tax due.

- True

- False – This Revenue Procedure only applies for estates of decedents who died PRIOR to January 1, 2014.

- True

- False – PLR is required and as of now there are no provisions for permanent relief in the final regulations. The cost is $9,800 if received prior to February 2, 2017 and $10,000 thereafter. Speakers at the Heckerling Institute thought it was $27,500.

- A) True

B) False – You can only use your last deceased’s spouse’s DSUE, not the spouse before that. The surviving spouse should therefore consider gifting without delay or at least before remarrying and having a new spouse die. The black widow serial killer could keep marrying and making gifts by killing multiple husbands.

The Antifragile Medical Practice

by Pariksith Singh, M.D.

Nassim Taleb in his brilliant book Antifragile shows how some entities only get stronger with volatility, uncertainty, fluctuations in the market and rapid shifts in business climate. He calls these entities “antifragile,” as opposed to fragile, i.e., the ones that get weaker or are destroyed by ‘black swan’ events.

The question for us then is: how do we make our medical practice antifragile? How do we get stronger while others are decimated? To my mind, an antifragile medical practice, or any other business needs a multi-pronged approach. Some of these essential elements include the following:

- Compliance: This is perhaps the key. A practice that adheres to the law, fulfils all regulations and requirements by being proactive and self-critical will thrive in demanding conditions. Over the last twenty years, I have seen several physicians indicted, several insurances shut down and several independent physician associations (IPAs) go bankrupt because they missed this crucial element of business. All medical concerns are under the microscope. Whether it is for coding and billing, marketing, Stark issues, OSHA guidelines, HIPAA, labor laws or equal opportunity employment laws. Strict compliance programs that are followed, measured, refined and disseminated inside the organization make it stronger on the spectrum of antifragility. Such compliance would not only be regulatory, but also clinical, and include proper staff training, testing, certification and auditing along with inventory management.

- Personal: I think this is the second most critical aspect of creating an antifragile medical practice or business. If one is wasteful, ostentatious, and heedless that makes one very vulnerable to market shocks. Over the last two decades, I have seen countless examples of successful physicians who became enamored with material possessions and displaying them boastfully. There are providers who are so proud that they pay their accountant to write personal checks for them (not numbering more than a dozen a month). Still, others have multiple Corvettes, Lamborghinis and BMWs for which they have to build multi-storey garages. Or then there are those who build 20,000 square feet homes that are difficult to maintain and sell. A simple personal life that is humble and content is the most sensible and fulfilling way to ensure your life and business remain antifragile.

- Risk Management: Sound business planning and asset management would mitigate several risks that providers are most vulnerable to. These range from holding assets under limited liability companies, or creating trusts and ensuring the proper use of tenancy by entireties laws in Florida. Strong insurance policies which cover personal liability, personal injury, malpractice, business coverage and umbrella policies need to be maintained.

- Financial: A well diversified portfolio that minimizes risk to downturns in the market and is able to take advantage of upturns is the best investment strategy. Beware of brokers who are willing to sell you all kinds of options. Be careful of 409s and 419s, even if they are blessed by attorneys. The best way to eliminate fragility is to become debt-free. Do not buy beyond your means, whether these are homes or boats or airplanes or vehicles. Having six months of the business’ operating expenses in a liquid account is also an approach that is antifragile. A good financial management system that is operated by conscientious financial staff will prevent stealing and pilferage. Paying taxes on time and not being delinquent is a must.

- Professional: How one treats patients, clients, vendors or employees is of great significance. How one’s employees treat patients and vendors also affects risk. Customer engagement can be measured, and listening to their feedback is an easy way to identify weaknesses. A proper review of contracts before signing them, use of great counsel and avoidance of unnecessary litigation preserves time and valuable resources. Developing a practice in niche or specialized markets might be helpful, along with the ability to scale over a wider geographical area with more providers also makes one risk-averse. Taleb recommends that we take small risks and spread them over time. Add new specialties to the repertoire one by one and build flexibility by responding to the market. A knowledge organization that shares information and best practices eliminates dependence on key employees or teams.

- Operations: Lean approaches work best in a non-hierarchical manner. Create quality checks and controls especially since physicians are busy seeing patients and have little time to directly supervise staff. Hiring and training needs to be invested with a lot of thought, time and energy. A good team that is loyal and efficient in a Learning Organization would make the practice immune to outside forces.

- Information Technology: The growth of digitalization brings its own dangers of ransomware attacks, loss of patient health information to hackers, and viruses. These can be addressed by creating strong infrastructure management services and training programs for employees so that they do not create vulnerabilities in the organization by mistake. A disaster recovery program with live contingency and real-time data backup is essential in this day and age. Service organization control (SOC) certifications should be maintained to ensure advanced protection and efficiency. Similarly, software maintenance has to be equally secure and deliberate.

My father always believed in having back-ups for any contingency. Taleb refers to this as building redundancy within the system. A culture that is never complacent and is constantly improving, iterating, testing and experimenting within the framework of compliance might be the best defense against hidden dangers. Being antifragile is an approach and state of mind that is more important than any single variable. This, perhaps, is the message to take home from Taleb.

8 Tips to Better Manage Your Company’s Debt and Financing Relationships

by David Finkel

David Finkel is the Wall Street Journal bestselling author of SCALE: Seven Proven Principles to Grow Your Business and Get Your Life Back, which can be viewed by clicking here. As the CEO of Maui Mastermind, he has worked with 100,000+ businesses coaching clients and community members to buy, build, and sell over $5 billion worth of businesses.

Whether you have a line of credit, a term loan, or some other bank credit facility, here are eight suggestions to more intelligently manage your debt as you scale your business.

- Negotiate better interest rates with your lenders. The best tool to help you do this is to get your lenders competing for your business. It’s a critical shift, but one that takes you out of the “applicant” and transform them into the sales person working to earn your business.The conversation sounds something like, “Mark, we’re in the process of interviewing banks to see who we want to select to refinance our equipment loans with. Is this a good time for me to ask you some questions to see if your bank might be a good fit for us to work with?”

- Click here to read the full article.

Follow David on Twitter: @DavidFinkel.

Input Request

We request input on medical marijuana patient informed consent forms and agreements to arbitrate. We are preparing these for the Spring Edition of the Florida Bar Health Law Section Newsletter.

If you would like to contribute to this please let us know and we can share our draft forms and agreements with you, and provide credit for assisting us.

“Candy is dandy, but liquor is quicker.”

Pot is not.

– by Ogden Nash

(Obviously, Ogden Nash never tried liquor)

Richard Connolly’s World

Inform Clients of Reporting Requirements for Charitable Gifts

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature some of Richard’s recommendations with links to the articles.

This week, the article of interest is “Inform Clients of Reporting Requirements for Charitable Gifts” by Conrad Teitell. This article was featured on WealthManagement.com on January 4, 2017.

Richard’s description is as follows:

Now’s a good time to tell your clients how to substantiate their charitable gifts on their 2016 federal income tax returns—due by April 18, 2017.

Strict, detailed and overlapping substantiation requirements must be met for charitable deductions to be allowed. And generally, there’s no second chance if deadlines are missed or requirements aren’t satisfied.

The following sample letter informs clients of the reporting requirements and deadlines. Readers of this article have permission to adopt (or adapt) the letter.

Please click here to read this article and the sample letter in its entirety.

Humor! (Or Lack Thereof!)

Sign Sayings of the Week

**********************************************************

Upcoming Seminars and Webinars

Calendar of Events

**********************************************************

FREE LIVE WEBINAR

Alan and Martin Shenkman will present a one hour webinar on Asset Protection Planning Continuum – Practical Steps for Estate Planning Lawyers and Other Professionals.

Join Alan and Martin for a very useful, sixty minute talk that will provide you with techniques, checklists, and important knowledge to increase and improve your skills and tools for protecting clients and their business and professional entities from creditors and other threats to wealth.

Date: Tuesday, February 21, 2017 | 12:30 p.m. Eastern

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com.

CLICK HERE to Register for this FREE Webinar.

**********************************************************

LIVE TRINITY PRESENTATION

Ken Crotty and Chris Denicolo will present RECENT DEVELOPMENTS AND STRATEGIES FOR ESTATE PLANNERS for the North Suncoast Estate Planning Council.

Date: Tuesday, February 21, 2017 | 5:00 p.m. EASTERN

Location: Fox Hollow Golf Club | 10050 Robert Trent Jones Pkwy, Trinity, FL 34655

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com.

**********************************************************

LIVE DISNEY WORLD PRESENTATION (HOW MICKEY MOUSE CAN YOU GET?):

2017 MER CONTINUING EDUCATION PROGRAM TALKS FOR PHYSICIANS

Alan will be speaking at the Medical Education Resources (MER) Internal Medicine and Country Bear Jamboree for primary care physicians and other characters. We thank MER for this wonderful opportunity and Walt Disney for having paved all of Osceola County. His topics will include:

- The 10 Biggest Mistakes Physicians Make in Their Investments and Business Planning

- Lawsuits 101

- 50 Ways to Leave Your Overhead

- Essential Creditor Protection and Retirement Planning Considerations

Date: Wednesday, March 15, 2017 and Thursday, March 16, 2017

Location: Walt Disney World BoardWalk Inn | 2101 Epcot Resorts Blvd, Kissimmee, FL 34747

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE ESTATE PLANNING DISCUSSION AT FLORIDA STATE UNIVERSITY SCHOOL OF LAW

Alan will appear via Skype with professors Steven Hogan and Bob Pierce to give his views, by interview style, for their estate planning course at Florida State University School of Law on Thursday, March 23, 2017.

Date: Thursday, March 23, 2017 | 1:15 – 3:00 p.m. (EASTERN)

Location: Florida State University School of Law

Additional Information: To receive a live call in code or videotape of this presentation, which we will qualify for continuing legal education credit, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE ESTATE PLANNING COUNCIL OF NORTHEAST FLORIDA PRESENTATION:

Alan will be speaking for the Estate Planning Council of Northeast Florida on March 20, 2018 on the topic of DYNAMIC PLANNING STRATEGIES FOR THE SUCCESSFUL CLIENT. This will be Alan’s third visit to Pensacola, and a welcome treat. Watch this space, as more details will be forthcoming!

Date: Tuesday, March 20, 2018

Location: To Be Determined

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE FLORIDA BAR CLE SEMINAR

Alan will be speaking at the 2017 Annual Wealth Protection Program presented by the Florida Bar and the Continuing Legal Education Committee. Alan will discuss EXEMPTION AND FLORIDA PLANNING 2016 – MORE THAN WHAT YOU THOUGHT, AND LESS THAT WHAT YOU WISH FOR.

Additional topics and speakers include:

- Key Asset Protection Strategies Integrations & Estate Planning Techniques and Wealth Management Products – Denis Kleinfeld

- Important Recent Developments and trends in Debtor Creditor Law – Including Discussion of the Uniform Voidable Transfers Act – Michael Markham & Arthur Neiwirth

- The Secrets to Avoiding the Tricks and Traps in Partnership Tax Planning – Jerry Hesch

- Critical Factors Every Florida Planner Must Know in Using Offshore Asset Protection Strategies – Les Share

- Trends in Practice – The Growing Oppurtunties for Skilled Wealth Protection Professionals Important Wealth Protection Cases, Law and Trends of Practice – What Happened and Where Are We Going?

Date: Friday, April 7, 2017 | 8 a.m. to 5 p.m.

Location: Hyatt Regency Downtown Miami – 400 SE Second Avenue, Miami, FL 33131

Additional Information: For more information, please email Alan at agassman@gassmanpa.com. To register, visit www.floridabar.org/CLE and use the Course Number: 2332R. A webcast will be available by clicking here.

LIVE NAPLES PRESENTATION:

Please put Friday, April 28th, 2017 on your calendar to enjoy the 4th Annual Ave Maria School of Law Estate Planning Conference and the weekend that follows in Naples.

Alan will be speaking at this conference on the topic of THE ETHICS OF AVOIDING TRUSTS AND ESTATE LITIGATION.

Alan will also appear on a panel of speakers with Jerry Hesch and Lester Law on the topic of TAX PLANNING WITH LIFE INSURANCE PRODUCTS, RECENT LITIGATIONS, AND OTHER HOT TOPICS.

Other speakers and topics include the following:

- Stacy Eastland – Comparing Freeze Techniques

- Jonathan Gopman – Asset Protection Trusts: An Update and Discussion of Planning

- Joan Crain – Challenges for Trustees in Dealing with Millennial Beneficiaries

- Jerry Hesch – Passing a closely-held business on to junior family members or key employees or co-owners: An analysis of the income tax, estate tax and financial impact of business succession planning techniques.

- Jerry Hesch & Alan Gassman – Life Insurance Planning Panel – Techniques, Tax Planning and The Good, the Bad, and the Ugly

- Tae Kelley Bronner – Homestead Planning and Update

- Lester Law – Basis Consistency for Estate and Income Tax Planning Purposes, and Multiple Implications Thereof.

- Marve Ann Alaimo & Dixon Miller – International Estate Planning Rules and Planning Opportunities

- Susan Cassidy, M.D. – What You Need to Know for Your Client’s Medical Issues: Competency, Great Care Versus the Mainstream, What Medicare Recipients Should Seek Outside of the Medicare System, End of Life Communications and Planning and How Will the Above be

- Alan Gassman – Ethical Considerations to Avoid Estate and Trust Litigation and Family Disputes, and the 10 or so Avoidance Techniques You Should Be Actively Using

- Suzy Walsh – Special Needs Trusts Essentials and Well Beyond

Date: Friday, April 28, 2017

Location: The Ritz-Carlton Golf Resort | 2600 Tiburon Drive, Naples, FL, 34109

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

**********************************************************

LIVE LAS VEGAS PRESENTATION:

AICPA ADVANCED PERSONAL FINANCIAL PLANNING CONFERENCE

Alan will be speaking at the Advanced Personal Financial Planning Conference, sponsored by The American Institute of CPAs. His topic for this event is LIFE INSURANCE TIPS FOR THE FINANCIAL PLANNING PROFESSIONAL. He will speak on June 14 from 10:50 to 11:40 a.m.

This conference is part of the AICPA ENGAGE event, which brings together five well-known AICPA conferences with the Association for Accounting Marketing Summit for one, four-day event. The conferences included in ENGAGE are Advanced Personal Financial Planning, Advanced Estate Planning, Tax Strategies for the High-Income Individual, the Practitioners Symposium/TECH+ Conference, the National Advanced Accounting and Auditing Technical Symposium, and the Association for Accounting Marketing Summit.

Date: June 12th – June 15th, 2017 | Alan’s speaks on June 14 from 10:50 to 11:40 a.m.

Location: MGM Grand | 3799 S. Las Vegas Blvd., Las Vegas, NV, 89109

Additional Information: For more information, please email Alan at agassman@gassmanpa.com or click here.

**********************************************************

LIVE NAPLES PROFESSIONAL ACCELERATION WORKSHOP

Alan will present a Professional Acceleration Workshop at Ave Maria School of Law.

Date: Friday, August 25, 2017 | 10:00 a.m. Eastern

Location: Ave Maria School of Law, Naples, FL.

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com. More details will be provided in the future, but please plan to attend.

**********************************************************

LIVE NEW PORT RICHEY PRESENTATION:

Alan will present AN ESTATE PLANNER’S UPDATE AND HOT TOPICS for the Charitable Consortium.

Date: Thursday, September 14, 2017 | 12:00 p.m. Eastern

Location: TBD

Additional Information: For more information, please contact Alan at agassman@gassmanpa.com.

**********************************************************

LIVE PRESENTATION:

ESTATE PLANNING COUNCIL OF NORTHEAST FLORIDA

Please put Tuesday, September 19, 2017 on your calendar to enjoy a dinner conference for the Estate Planning Council of Northeast Florida.

Date: Tuesday, September 19, 2017

Location: TBA

**********************************************************

LIVE PRESENTATIONS:

2017 MER CONTINUING EDUCATION PROGRAM TALKS FOR PHYSICIANS

Alan will be speaking at the following Medical Education Resources (MER) events:

- October 20th – October 22nd, 2017 in New York, New York

- November 30th – December 3rd, 2017 in Nassau, Bahamas

His tentative topics for these events include the 10 Biggest Mistakes Physicians Make in Their Investments and Business Planning, Lawsuits 101, 50 Ways to Leave Your Overhead, and Essential Creditor Protection and Retirement Planning Considerations.

Date: New York: October 20th – 22nd, 2017Nassau: November 30th – December 3rd, 2017

Location: New York: To be determined.

Nassau: Atlantis Hotel | Paradise Beach Drive, Paradise Island, Bahamas

Additional Information: For more information, please email Alan at agassman@gassmanpa.com.

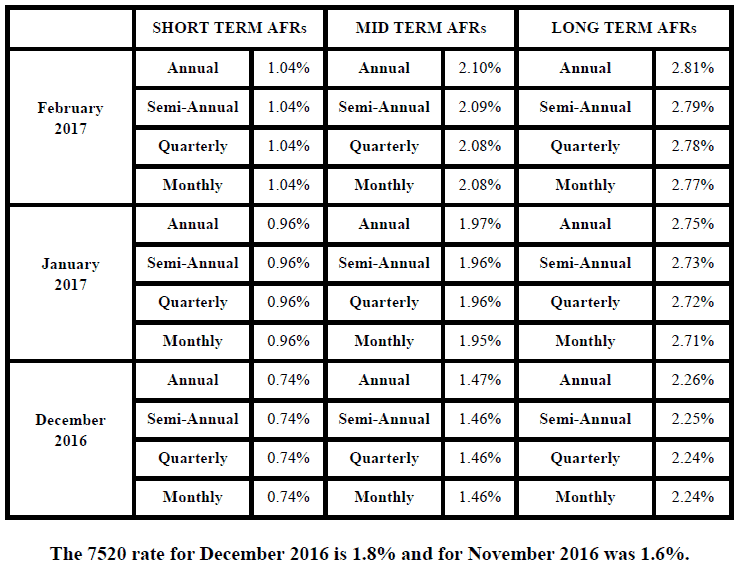

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.