The Thursday Report – 9.18.14 – Reverse Mortgage Information, Worker Classification, and Mr. Ed

Common Trust Errors

Reverse Mortgages Explained, Part 1

Worker Classification Issues in Professional Practices, an Article by William P. Prescott, Mark P. Altieri, and Kelly A. VanDenHaute, Part 1

Thoughtful Corner – Robert Chapman’s Ted Talk on Dedication to Employee Welfare

Who Said What Joke Contest Answers

Humor! (Or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

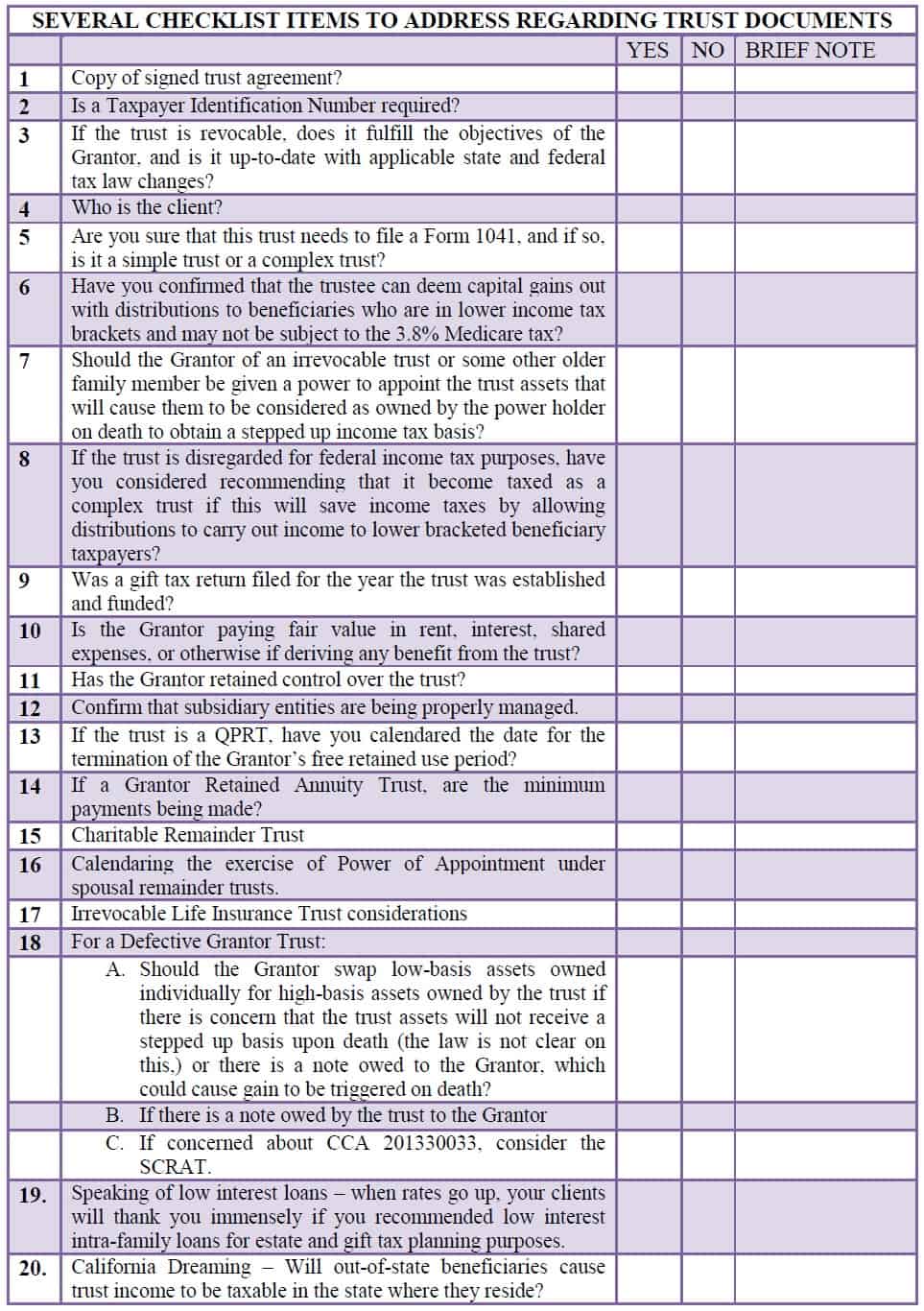

Common Trust Errors

Today, Alan Gassman is speaking to the state FICPA conference in Ft. Lauderdale on Trust Planning from A to Z.

Our outline includes the following checklist that CPAs and other advisors can use to spot and handle common trust administration tax reporting and practical errors.

These items are explained in the outline for the presentation, which will be provided in the next three subsequent Thursday Reports.

One thing we really appreciate is the significant amount of feedback and suggestions that we get from readers. We thank and salute Gordon Spoor, CPA, for everything that he has done and will continue to be doing with respect to trust accounting, tax, and administrative matters and practice, and to many others like Barry Spivey, Esquire and David Stone, Esquire, for all of the work, effort and results derived from what they have done for the trust law and community.

We hope that the following may be considered for inclusion in your practice or anyone else’s.

Reverse Mortgages Explained, Part 1

Today marks the deadline for our Notre Dame materials on reverse mortgages.

We are therefore pleased to provide the first part of our reverse mortgage outline, which will probably become a layman’s guide sometime in the future.

We are concerned that a great many elderly Americans are entering into these arrangements without understanding the real costs and implications associated therewith.

This is evidenced by a default rate exceeding 9%, and lenders being able to sell their loan documents at 10% above the amount owed, with the US government footing the bill for any excess of the amount owed over the value of the house at the time the loan is to be satisfied, and borrowers paying 1.25% a year on top of interest and other expenses to the government.

One key problem is that the program enables Americans who are not necessarily getting good legal or personal advice to make a big mistake by going into debt, while being told that there will be no detrimental effect on them, and that there is absolutely no obligation going forward.

When over 9% of the borrowers cannot keep current with their real estate taxes, insurances, and maintenance it is clear that there is a problem.

To make matters worse, borrowers are not told that the equity that they are giving up is the safest thing that they can own as Floridians, in that a Floridian with a home worth $543,000 or more who has lived there one (1) year can go into a nursing home and qualify for Medicaid, and retain the equity in the home notwithstanding that it may be rented while they are living and sold by their family after death.

If the homeowner has instead entered into a reverse mortgage and keeps other assets that would have to be spent down for Medicaid, then a tremendous disservice has been done to them.

Further, we all know that people will tend to make bad decisions based upon emotion and lack of proper advice.

A typical elderly person is not in a good position to realize that she should downsize, move to a retirement type of community, stay out of debt, and remain flexible. Also, the interest rates are pretty darn high, when you consider that in addition to the interest the borrower will have loan costs that can be as much as $6,000 or more.

If you are still interested in reverse mortgages after reviewing the above, then we hope you enjoy what follows:

INTRODUCTION

Definition: A mortgage is a loan agreement secured with real estate as its collateral. Under most mortgages, the borrower makes monthly payments until the loan is repaid. In a reverse mortgage, however, payment is only due if and when one of the following occurs:

(a) the home is sold,

(b) the borrower no longer lives in the home for a period of more than 12 months (this includes if the borrower has to move into a long-term care facility such as a nursing home or an assisted living facility),

(c) the borrower dies, or

(d) the borrower does not keep up with the real estate taxes, insurance and maintenance of the home.

When a husband and wife are joint borrowers, then (b) or (c) may not apply until neither of them is residing in the home.

History: The reverse mortgage came about in 1988, when Congress enacted a federal program aimed at relieving elderly homeowners from the financial burden of typical monthly mortgage payments. Congress found that costs for “health, housing, and subsistence” were on the rise for seniors, while income was being reduced.1 It is of note here that the federal government itself became the insurer on many reverse mortgages. A reverse mortgage insured by the federal government is formally known as a Home Equity Conversion Mortgage (“HECM”), and is only available through a Federal Housing Authority (FHA) approved lender. The United States Department of Housing and Urban Development (HUD) insured its first FHA insured reverse mortgage in 1989.

Information Sources: We have used a number of resources to prepare this outline, but there is no recently published literature on default rates, issuances, or the federal program and its budget, to our knowledge.

HOW REVERSE MORTGAGES WORK

Terms: When a loan is FHA insured, both the lender and the borrower are protected from either party owing any amount on the mortgage in excess of the net proceeds from the sale of the home. This is because HUD guarantees that a borrower who remains in compliance with the terms of the reverse mortgage loan will never have a responsibility above and beyond the actual market value of the home at the time of sale. HUD will therefore pay the lender the difference of any amount owed on the mortgage which exceeds the net proceeds from the sale of the home.

In order to qualify a loan as FHA insured under these terms, lenders and borrowers must follow the HUD guidelines, and borrowers are required to pay an annual mortgage insurance premium equal to 1.25% of the outstanding loan balance. This is in addition to the interest and other loan charges that are incurred.

Types of Reverse Mortgage Loans: There are three main types of Home Equity Conversion Mortgage loan options.

(a) Line of Credit- This is an immediate loan where the borrower receives up to a maximum percentage of the value of the home. HUD regulations provide that only a portion of this loan amount can be taken over the first year, so the borrower will typically receive one lump sum amount when the loan is established, and then the remaining borrowed funds are provided one year thereafter. The Line of Credit was designed for elderly people who want to borrow money to cover major expenses, such as home improvements or medical bills. However, in practice these funds are commonly used for other things, leaving borrowers vulnerable to the possible loss of their home when they cannot keep up with insurance, taxes, and maintenance.

For example, suppose a loan is made against a house valued at $190,000 by a 79 year old borrower in August of 2014. $20,000, plus loan costs (which might be an additional $9,235.50) can be borrowed at the time of the loan closing, and $64,637.50 can be borrowed the year after. Further borrowing is limited to a certain portion of future growth in value of the property, if it goes up in value.

(b) Tenure Loan- The tenure loan is set up in a life payment format, whereby the borrower can receive a small lump sum initially, and then continues to receive a fixed monthly amount for the rest of his or her lifetime. This income stream loan was intended to help borrowers cover their everyday expenses. The loan amounts are to be advanced each month notwithstanding what the value of the house will be, again as long as the borrower maintains the taxes, insurance and maintenance thereof.

For a married 79 year old fully owning his or her home, a typical tenure loan would provide $20,000 cash at closing, and then $667.25 a month (about $8,000 a year) until the death of both the borrower and his or her spouse.

The life expectancy of the surviving spouse of such a married couple (assuming both spouses are 79) is eight (8) years, so the total amount borrowed would be expected to be $102,550.71.

(c) Fixed Term Loan- The fixed term loan is similar to the tenure loan, but it provides for annual or monthly loan amounts that are preset as to the amount received and the duration. For example, a homeowner may borrow $1,000 a month for one hundred and twenty (120) consecutive months, notwithstanding whether the home goes down in value, or whether the lender would prefer not to make further advances or becomes insolvent.

Mortgage Rates: Reverse mortgage borrowers have multiple choices with respect to the interest rates of their loans: whether the interest rate will be fixed, and if capped, what the possible terms of increasing rates will be:

(a) Fixed Interest Rate- The fixed interest option locks the rate in for the duration of the loan, whether that be term or lifetime. Fixed interest loans typically have somewhat higher rates (approximately 5% in August of 2014), but they offer a greater deal of stability. The interest charged is above and beyond the 1.25% per year payment that the borrower must make for the FHA/HUD insurance described above.

(b) Floating Interest Rate- The floating interest rate is subject to change with the market throughout the duration of the loan. A floating interest rate is typically lower to begin with, but can increase considerably. An August 2014 loan might begin at a 2% interest rate but be able to float up to a 12% rate. Typically these loans have a provision in place whereby the increase in rate must be incremental, such as a 2% increase every year.

An example for the married couple described above would be the following choices for a loan taken in August of 2014.

1.) 4.990% fixed with $6,767.50 in closing costs.

2.) 2.935% floating, but guaranteed to not go up by more than 2.00% annually and capped at 7.935%, with closing costs of $9,234.50.

3.) 3.560% floating, but guaranteed not to go up by more 2.00% annually and capped at 8.560%, with closing costs of $5,934.50.

4.) 3.656% floating, but guaranteed not to go up by more than 2.00% annually and capped at 13.656%, with closing costs of $4,484.50,

The option that educated or well advised borrowers will choose depends upon their risk tolerance, life expectancy, and a number of other factors. A typical borrower is not savvy enough to understand or take into account these considerations.

If interest rates were to increase dramatically over the term of the loan, the prospective borrower would be best served by either paying the higher closing cost to receive the lowest cap, or electing to use the fixed interest rate option. Alternately, if interest rates stay at today’s levels (which are historical lows), then the prospective borrower would be best served by paying the lowest closing costs. Some borrowers can afford to take risks with floating interest and others cannot. Given that at least 9% of these loans end up in default, it must be assumed that a good many borrowers are not appropriately educated or advised when they make these decisions.

Loan Costs: Loan costs above and beyond the interest for a reverse mortgage are typically 2-3% of the total credit offered. This is not particularly high compared to other loan products. Loan costs may be subsidized by the lender, or the borrower may be directly responsible for them. It is important to consider this factor when looking at the terms of a reverse mortgage. For some reason, the normal rules under the Truth in Lending Act, which apply when people buy cars or take out other kinds of loans, do not have jurisdiction in the reverse mortgage world. Instead, there is a separate disclosure known as the Total Annual Loan Cost or TALC.

Default: If the borrower defaults on the loan by not remaining current with his or her payment of real estate taxes, homeowner’s insurance, or maintenance on the home, then the lender can call the loan into default and demand full repayment. At that point, to avoid foreclosure the borrower must complete one of the following precautionary actions:

(a) correct the default,

(b) pay off the debt, default rate interest, legal expenses, and lender costs;

(c) sell the property and apply the net proceeds to the loan balance, or

(d) deed the property to the lender.

Usage: There were over 770,000 reverse mortgages issued through September of 2012, and 595,000 of these loans remained outstanding as of May of 2013. Banks and financial institutions make a significant amount of money under this program by:

(a) collecting loan origination fees, which commonly range anywhere between $2,500 and $6,000, and/or

(b) selling the loans to investment syndicates and other organizations, who reportedly pay a 10% to 12% of the total amount to be loaned for the right to be the lender.

Many people believe that the high rate of return many lenders receive on the sale of reverse mortgages is evidence that the U.S. Government’s program benefits lenders more than it benefits borrowers. Lenders are not able to charge borrowers more than certain amounts upon origination, but are able to charge interest rates that exceed what an unsubsidized marketplace might provide. The end result may be seen as a government subsidy made primarily to lenders, which in many cases causes harm to borrowers who are supposed to be the beneficiaries of this program. The harm done to borrowers is further discussed below.

*****************************************

1“Sustainable Housing Finance: The Government’s Role in Multifamily and Health Care Facilities Mortgage Insurance and Reverse Mortgages”. Written Testimony of The Office of Housing/Federal Housing Administration U.S. Department of Housing and Urban Development Hearing Before the House Financial Services Committee. May 16, 2013.

This is part one of a two part white paper by some very well-qualified and well-respected lawyers who specialize in dental and other professional practice planning. Tax and health care professionals will appreciate what they have to say.

William Prescott of Wickens, Herzer, Panza, Cook & Batista Co. in Avon, Ohio specializes in representing dentists and other professionals and is a chairman of the Closely Held Businesses Committee of the Tax Section of the American Bar Association.

Bill and two of his colleages, Mark P. Altieri and Kelly A. (Means) VanDenHaute, have written an excellent article entitled “Worker Classification Issues in Professional Practices” that serves as a good refresher for those of us who have been working in this area and an excellent strategy guide for everyone. Hats off to Bill, Mark and Kelly for writing this article and making it available for Thursday Report readers. The article is as follows:

UNDER WHAT CIRCUMSTANCES can a professional worker be properly classified as an employee or independent contractor for federal tax purposes? The following three examples represent common situations where worker classification applies to professional practices.

- The new professional (often forming a new entity, typically an S-corporation) renders professional services to the existing practice owner’s entity. The new professional has not yet purchased any interest of the existing owner’s practice, although a future purchase may be contemplated;

- The retiring professional renders post-closing professional services, typically for six months to a year, following the practice sale to the new owner; and

- The new professional purchases part of the old professional’s practice and the new professional and old professional form a limited liability company (“LLC”) through which professional services are rendered. Usually, each professional is also the sole shareholder of an existing C-corporation or a newly-formed S-corporation that becomes a member of the LLC and through which professional services are provided to the practice.

With limited exceptions, in each situation our conclusion is that the professional is an employee of the professional practice, the entity actually providing services to the public.

Practice consultants frequently question the audit risk in these scenarios where the independent contractor pays its, his, or her applicable self-employment taxes, thereby making the government whole as to those combined taxes that would be paid in an employer/employee setting. The actuality is that the IRS can and will assess Federal income tax, FICA, and FUTA, as well as penalties and interest against the business or practice for misclassification and the deductions for the misclassified independent contract would, for the most part, be lost. Our advice would be not to take unnecessary risks.

The employment tax cases back up this conclusion and the government’s claim against the practice to pay the worker’s taxes. Assuming that the worker did pay its, his, or her applicable taxes, the government’s successful claim against the practice can result in double taxation with the government collecting the same tax twice. There may be a direct credit to the employer under Internal Revenue Code (“IRC”) section 3402(d) for the worker’s income taxes that have already been paid by the worker. Tax Management Portfolios, BNA, Inc., 391-3rd Employment Status – Employee v. Independent Contractor, Helen Marmoll, Esq., p. A-160. Notwithstanding this, the economic impact of misclassification is very expensive to the practice not only in terms of unpaid taxes, fines, and interest, but also due to the time, emotional toll, and advisory costs of a defense. Misclassifying a worker(s) can also have very negative affects upon retirement plans, including disqualification, not to mention the ability to include the worker in the health insurance plan of the practice. Vizicano v. Microsoft Corp., 120 F3d 1006 (9th Cir. 1997), cert. denied, 522 U.S. 1098 (1998) (1998).

From the worker’s standpoint, business expenses of a reclassified employee generally would be nondeductible, subject to the two percent of adjusted gross income limitation under IRC section 67. (References to “IRC” are to the Internal Revenue Code of 1986, as amended.) Also see Independent Contractor or Employee? Training Materials, Department of the Treasury, Internal Revenue Service, October 30, 1996, Training 3320-102 (10-96) TPDS 843381 p. 1-5, available at www.irs.gov/pub/irs-utl/emporind.pdf (Hereinafter “Training Materials”.) For example, in Maimon v. Commissioner, T.C. Summary Opinion 2009-53 (2009), the court held that a doctor was an employee of a medical practice. The doctor sought to be recognized as an independent contractor once he was faced with a large expense resulting from an employment-related lawsuit. Because he was found to be an employee of the practice, he was forced to report his compensation on Form 1040, line 7 and was not entitled to deduct the claimed business expenses on Schedule C. Instead, he was forced to claim the expenses on Schedule A as unreimbursed employee business expenses subject to the aforementioned two percent limitation for miscellaneous expenses. As noted, a worker who is reclassified as an employee cannot maintain an employer-sponsored retirement plan such as a 401(k) plan.

In its 1996 Training Manual referenced above, the IRS recognized that the well-known 20 factor test is an analytical tool and not the legal test for determining worker status. Per the Training Manual and more recent IRS rulings and publications, it has been made clear that the legal test is whether there is a right to direct or control the means and details of the work. Id. P. 2-3; IRS Publication 1779 (Rev. 8-2008); Priv. Ltr. Rel. 2003-23-022 (Feb. 24, 2003). The test divides control into three categories: behavioral control, financial control, and the relationship of the parties. Id.

BEHAVIORAL CONTROL The primary factor of behavioral control involves instructions. Id. Treasury Regulations provide that professional workers who are engaged in an independent trade, business, or profession in which they offer their services to the public are independent contractors and not employees. Treas. Reg. §31.3121(d)-1(c)(2). However, most professionals are not providing services to the public independently, but on behalf of the practice where they work. While the instructions for professional services may be minimal, nearly all practices have policies covering operations to which the worker is subject. Types of instructions may include:

- When to do the work;

- Where to do the work;

- What tools or equipment to use;

- What workers to hire to assist with the work;

- Where to purchase supplies or services;

- What work must be performed by a specified individual; and

- What order or sequence to follow. IRS Publication 15-A (2010).

FINANCIAL CONTROL Financial control considerations included the following:

- Does the worker have a significant investment in the business?

- Is he or she reimbursed for out-of-pocket expenses associated with the business?

- What is the method of payment to compensate the worker? And

- Will the worker directly share in the business profit and loss? PLR 200323022.

As to a significant investment, few professionals individually own the equipment in their offices or rent the equipment from the practice at fair rental value.

Independent contractors almost always have unreimbursed expenses and are generally free to seek out business opportunities. As such, independent contractors typically advertise, maintain a visible business location that they directly pay for, and are available to work in a particular market. IRS Publication 15-A (2010). However, in professional practice settings, the professional is almost always subject to restrictive covenants that restrict the ability to work in a given market, other than for the particular practice, thus further illustrating an employer-employee situation.

Professionals are frequently paid on a commission basis (as a function of productivity) and this does show evidence of an independent contractor relationship. However, it is the practice that customarily sets the fee schedule and bills the clients. This shows financial control. IRS Publication 15-A (2010).

If the worker is free to make decisions that affect the worker’s profit or loss, the worker could be an independent contractor. Examples include types and quantities of supply inventory, the type and amount of monetary or capital investment, and whether to purchase or lease the premises or equipment. Training Materials, p. 2-21. In professional practice settings, professionals do not often have the ability to directly realize a profit or loss considering these factors. Although a professional can work longer or shorter hours (which affects profit), so can non-professional employees. Therefore, this hourly point is not too significant.

In professional practices, the practice almost always maintains control over all financial and business aspects of its operation, including setting fees, billing the clients, collecting the fees, and paying operating expenses. Although it is possible for the professional to be an independent contractor if the worker sets the fees, bills the patients or clients, and pays rent for use of the premises and equipment, this in reality rarely happens.

RELATIONSHIP OF THE PARTIES A nominal independent contractor agreement, in and of itself, is not sufficient evidence for determining a worker’s status. Training Materials, p. 2-22. Under the Treasury Regulation, the designation or description of the parties is immaterial. Treas. Reg. §31.3121(d)-1(a)(3). Therefore, the substance of the relationship, not the label, governs the worker’s status. Id.

Frequently, professionals will incorporate themselves and will further provide that the worker is an employee of his or her corporation and not the practice. Just because a worker receives payment through his or her corporation does not mean that the worker will be found to be an independent contractor relative to the practice. Id. at p. 2-23. Incorporation, therefore, provides no substantive help in establishing independent contractor status.

The ability of the worker to quit or of the practice to freely terminate the services of the worker no longer has, in and of itself, significant bearing on whether the relationship is one of an employee or independent contractor relationship. The term of the relationship, however, may have an impact on worker classification. An indefinite term indicates an employer/employee relationship while a long term or temporary term may indicate either. PLR 200323022.

Next week we will continue the article with a discussion of some interesting cases.

Thoughtful Corner

Robert Chapman’s Ted Talk on Dedication to Employee Welfare

Robert Chapman has been the CEO of Barry-Wehmiller, Inc., which is a $1.5 billion (in sales) company that has an incredible growth and financial achievement track record.

Alan was fortunate enough to meet Mr. Chapman and his wife a couple of years ago and to have dinner with them and a good friend, Srikumar Rao, Ph.D., to talk about the phenomenal success that they have enjoyed both in working to enhance the work environment and life balance education of their employees, and the phenomenal results that this has provided for their company.

Mr. Chapman explains in the below referenced YouTube video that he was trained to be a business manager, and to manage the business, not necessarily the people.

What he has found is that the people we hire will provide us with basic labor using their hands, but we have to take extra steps to receive the contributions of passion, dedication, and “thinking like an owner” by going the extra mile.

How many of your employees are thinking like owners, watching your back, and helping you take your business or practice to a higher level on a constant basis? The chances are it is fewer than one in twenty, but in our law firm we believe that the ratio is much higher.

What is the difference? We work to actively engage our team members not only in the process of “doing the work”, but also in the process of “building the cathedral.”

Building the cathedral goes to a medieval conversation made famous by the Dean of all management gurus, Peter Drucker, in telling the story of three men working like slaves during the Renaissance cutting stone to help build a church. When asked what they were doing, the first man replied that he was cutting stone, the second man replied that he was doing the best job of stonecutting in the entire county, and the third man replied that he was building a beautiful cathedral.

Years later the first man had died, the second man was still grueling away, and the third man was an architect designing his own cathedral.

Which of these men are you, and which of these men are your team members?

In subsequent editions, we will discuss ways to help engage team members in the art of improving your professional or business office. To review Robert Chapman’s video, click here.

More about Peter Drucker’s story of the three men working to help build a cathedral can be viewed by clicking here and information on Peter Drucker can be found by clicking here.

Who Said What Joke Contest Answers

Last week, we held a Who Said What Joke Contest, featuring memorable quotes and one-liners from Robin Williams, Joan Rivers, and Joey Bishop.

Below, we have the answers!

- “People say that money is not the key to happiness, but I always figured if you have enough money, you can have a key made.” – Joan Rivers

- “In England, if you commit a crime, the police don’t have a gun and you don’t have a gun. If you commit a crime, the police will say: ‘Stop, or I’ll say stop again.’” – Robin Williams

- “I once called my mother during a hurricane. She got on the phone and said, ‘I can’t talk to you. The lines are down.’” – Joey Bishop

- “I’ve actually gone to the zoo and had monkeys shout to me from their cages, ‘I’m in here when you’re walking around like that?!’” – Robin Williams

- “I was so ugly that they sent my picture to Ripley’s Believe It or Not and he sent it back and said, ‘I don’t believe it.’” – Joan Rivers

- “My doctor is wonderful; once, when I couldn’t afford an operation, he touched up the X-rays.” – Joey Bishop

- “My daughter and I are very close, we speak every single day and I call her every day and I say the same thing, ‘Pick up, I know you’re there.’” – Joan Rivers

- “Do you think God gets stoned? I think so — look at a Platypus.” – Robin Williams

- “Today you can go to a gas station and find the cash register open and the toilets locked. They must think toilet paper is worth more than money.” – Joey Bishop

- “Every so often, Rumsfeld comes out and goes, “I don’t know where. I don’t know when. But something awful’s going to happen. Thank you, that’s all for today, no further questions.” Excuse me, can you give me a clue? What is it, the Central “Intuitive” Agency now?” – Robin Williams

- “The other day I drove home filled with pride and a sense of achievement. ‘Mama,’ I said proudly, ‘I have a new Corvette outside.’ Mama looked at me, shook her head and said sadly, ‘Please, don’t bring her in.’” – Joey Bishop

- “She doesn’t understand the concept of Roman numerals; she thought we fought in World War Eleven.” – Joan Rivers

- “And what’s George W. Bush doing now? He’s a motivational speaker. It’s kind of cool. It’s kind of like having Lindsay Lohan as a guidance counselor.” – Robin Williams

Bonus Round: What famous TV show did Joan Rivers and Robin Williams appear on together in 1977?

Answer: Laugh In

Humor! (Or Lack Thereof!)

Mr. Ed Lawyers Up!

Talking horse negotiates plea deal – will avoid doing hard time in exchange for spilling his guts about Wilbur cooking chicken with 11 special herbs and spices in the “other stable.”

Important Legal Precedent to Use in Your Next Case: Malibu Barbie v. Mattel

Summary of court action: Plaintiff Malibu Barbie asserts that Mattel, Inc. did not provide her with heeled shoes, in the full knowledge that said Plaintiff does not have heels that touch the ground. Said Plaintiff repeatedly falls on her face, being unable to stand without the support of Beach Ryan. Plaintiff alleged the company’s negligence caused her to miss an important spray tan party. Plaintiff asked for remuneration, citing G.I. Joe v. Hasbro, in which parent company was forced to pay veteran’s benefits and disability for injuries suffered in combat.

Defendant Mattel, asserted that the precedent was irrelevant, G.I. Joe’s injuries suffered as a direct result of his function, and that Malibu Barbie has already been supplied with a perfectly good dream house. Defendant alleges that Barbie falls down because she keeps spinning between Ken and Beach Ryan, unable to make up her mind. Defendant also produced a witness, Mermaid Barbie, who testified that Malibu Barbie is lucky to have any feet at all.

Presiding judge required Mattel to provide Malibu Barbie with different matching high heeled shoes for each of her 1,287 outfits.

Upcoming Seminars and Webinars

LIVE FT. LAUDERDALE PRESENTATION:

FICPA ANNUAL ACCOUNTING SHOW

Alan S. Gassman is speaking this afternoon at the FICPA Annual Accounting Show on the topic of TRUST PLANNING FROM A TO Z for 50 minutes, which will include the compliance checklist and explanation mentioned above. If you would like for him to give this talk for your organization please let us know.

********************************************

NEXT WEEK – FANTASTIC LIVE 4 to 5pm CLEARWATER PRESENTATIONS FOLLOWED BY A BACKSTAGE TOUR OF RUTH ECKERD HALL AND ZEV BUFFMAN SPEAKING ON AMAZING STORIES ABOUT HIS UNIQUE AND VARIED LIFE EXPERIENCES.

Board Certified Tax Attorney Michael O’Leary from the Trenam Kemker firm in Tampa, Florida and Christopher Denicolo from Gassman Law Associates will be speaking at the Ruth Eckerd Hall Planned Giving Advisory Council event on Tuesday, September 23, 2014.

Mr. O’Leary’s topic is HOT TOPICS IN CHARITABLE PLANNING AND MORE.

Mr. O’Leary’s topic is HOT TOPICS IN CHARITABLE PLANNING AND MORE.

Mr. Denicolo’s topic is PLANNING FOR INHERITED IRAs.

Mr. Denicolo’s topic is PLANNING FOR INHERITED IRAs.

Date: Tuesday, September 23, 2014 | 5:00 p.m.

This presentation is free to members of the Ruth Eckerd Hall Planned Giving Advisory Council, Ruth Eckerd Hall members, and professionals who are attending a Ruth Eckerd Hall Planned Giving Advisory Council event for the first time.

Additional Information: You can contact Suzanne Ruley at sruley@rutheckerdhall.net or via phone at 727-791-7400, David Abelson at david.abelson@morganstanley.com or via phone at 727-773-4626, Alan S. Gassman at agassman@gassmanpa.com or via phone at 727-442-1200 or the Kentucky Fried Chicken located at 1960 Gulf to Bay Blvd, which is close in proximity to this location and available to provide you with crisp, spicy or even crispier chicken, mashed potatoes and gravy, rolls, and slaw! Bring your 32 oz. Kentucky Fried Chicken drink container to the presentation and we will fill it with your choice of club soda or seltzer water, but no sharing permitted.

********************************************

LIVE AVE MARIA SCHOOL OF LAW PROFESSIONAL ACCELERATION WORKSHOP

Alan Gassman will present a full day workshop for third year law students, alumni and professionals at Ave Maria School of Law. This program is designed for individuals who wish to enhance their practice and personal lives.

Date: DATE TO BE DETERMINED | 8:30am – 5pm

Location: Ave Maria School of Law, 1025 Commons Cir, Naples, FL 34119

Additional Information: To register for this program please email agassman@gassmanpa.com

********************************************

FREE LIVE WEBINAR:

Attorney Leslie A. Share will be joining Alan Gassman for a free 30 minute webinar on DEMYSTIFYING U.S. TAX AND ESTATE PLANNING CONSIDERATIONS FOR FOREIGN INVESTORS – CONCEPTS THAT YOU CAN CLEARLY UNDERSTAND AND EXPLAIN TO CLIENTS

Date: Monday, September 29, 2014 | 5:00 p.m.

Location: Online webinar

Additional Information: To register for the webinar, please click here.

********************************************

LIVE CLEARWATER PROFESSIONAL ACCELERATION WORKSHOP

Alan Gassman will be joined by several experienced attorneys and other well respected industry experts during a full day workshop for lawyers and other professionals who wish to enhance their practice and personal lives.

Date: Sunday, October 5, 2014 | 8:30am – 5pm

Location: Clarion Hotel, 20967 US 19 N., Clearwater

Additional Information: To register for this program, please email agassman@gassmanpa.com

********************************************

FREE LIVE WEBINAR

THE BCA’s OF REVERSE MORTGAGES

Alan Gassman will be presenting a webinar about reverse mortgages.

Date: Wednesday, October 8, 2014 | 12:30 p.m.

Location: Online webinar

Additional Information: To register for the webinar, please click here.

********************************************************

LIVE NEW JERSEY PRESENTATION – WHAT NEW JERSEY LAWYERS NEED TO KNOW ABOUT FLORIDA LAW TO REPRESENT SNOWBIRDS AND FLORIDA BASED BUSINESSES:

NEW JERSEY INSTITUTE FOR CONTINUING LEGAL EDUCATION (ICLE) SPECIAL 3 HOUR SESSION

New Jersey song trivia: What song includes the words “Counting the cars on the New Jersey Turnpike, they’ve all gone to look for America”? What year was it recorded and who wrote it?

Alan S. Gassman will be the sole speaker for this informative 3 hour program entitled WHAT NEW JERSEY LAWYERS NEED TO KNOW ABOUT FLORIDA LAW

Here is some of what the New Jersey Bar Invitation for this program provides:

New Jersey residents have always had a strong connection to Florida. We vacation there (it is our second shore), own Florida property (or have favored relatives that do) and have family and friends living there. Sometimes our wealthiest clients move to Florida and need guidance, and you need background in order to continue representation.

There are real and significant differences between the two states that every lawyer should be cognizant of. For example, holographic wills are perfectly legitimate in New Jersey and anyone can serve as an executor of an estate, which is not the case in Florida. Also, Florida=s new rules regarding LLCs are different, and if you are handling estates of New Jersey decedents who owned Florida property, there are Florida law issues that must be addressed. Asset protection differs significantly in Florida too.

Gain the knowledge you need to assist your clients with Florida matters including:

- Florida specific laws involving businesses, trusts, and estates

- Florida tax planning

- Elective share and homestead rules

- Liability Insulation and Planning

- Creditor Protection and Strategies

- Medical Practice Laws

- Staying within Florida Bar Guidelines that allow representation of Florida clients

Comments from past attendees of this program:

- Excellent seminar and materials!!!

- This was one of the best ICLE seminars yet!

- One of the best seminars I have attended.

- Better than mashed potatoes and gravy. Glad he didn’t serve grits!

Date: Saturday, October 11, 2014

Location: TBD

Additional Information: This is a repeat of the same program that we gave last year, but our book is now updated for the new Florida LLC law and changes in estate and trust law. Please tell all of your friends, neighbors, and enemies in New Jersey to come out to support this important presentation for the New Jersey Bar Association. We will include discussions of airboats, how to get an alligator off of your driveway, how to peel a navel orange and what collard greens and grits are. For additional information, please email agassman@gassmanpa.com

********************************************************

LIVE NEW PORT RICHEY PRESENTATION:

Alan S. Gassman, Kenneth J. Crotty and Christopher J. Denicolo will address the North FICPA Group on Financial Analysis and Tax Planning for Investment Products, Including Variable Annuities, Fixed Annuities, Life Insurance Contracts, and Mutual Funds – What Should the Tax and Financial Advisor Know and Advise?

Be there or be an equilateral triangle!

Date: Wednesday, October 15, 2014 | 4:30 p.m.

Location: Chili’s Port Richey, 9600 US 19 N, Port Richey, Florida

********************************************************

LIVE MIAMI LAKES PROFESSIONAL ACCELERATION WORKSHOP

Alan Gassman and Phil Rarick will be presenting a free half-day workshop for lawyers and other professionals who wish to enhance their practice and personal lives.

Phillip B. Rarick, J.D. has over 30 years of experience in both private and public legal work. Mr. Rarick concentrates in the fields of estate planning (wills and trusts), asset protection, probate, and corporate law. Integrated asset protection with an estate plan designed to protect wealth and secure tax advantages are a primary focus of his practice. He is an active member of the Elder Law Section of the Florida Bar, and the Real Property, Probate and Trust Law section of the Florida Bar Association.

Mr. Rarick is the author of a number of popular guides for fellow attorneys and the public, including Florida Probate Quick Reference Guide and Understanding Living Trusts for Florida Residents.

Mr. Rarick is a past President of the Miami Lakes Bar Association, and has served as a Board Director for 11 years. Mr. Rarick’s email address is PhilRarick@raricklaw.com

Date: Sunday, October 19, 2014 | 1pm – 5pm

Location: Shula’s Hotel, 6842 Main Street, Miami Lakes, FL 33014 | Boardroom

Cost: $35 per person

Additional Information: To register for this program please email agassman@gassmanpa.com

The invitation for this event can be viewed by clicking here.

********************************************************

LIVE CLEARWATER PRESENTATION

Alan Gassman will be speaking at the Pinellas County Estate Planning Council Fall Seminar on PLANNING FOR SAME GENDER COUPLES.

Date: Thursday, October 23, 2014 | 8:00 am

Location: Ruth Eckerd Hall, 1111 N. McMullen Booth Road, Clearwater, FL

Additional Information: To register for this event please email agassman@gassmanpa.com

********************************************************

LIVE PASCO COUNTY PLANNED GIVING (AND DRINKING!) COCKTAIL HOUR AND PRESENTATION:

Alan S. Gassman and Christopher J. Denicolo will be speaking at the Pasco-Hernando State College’s Planned Giving Consortium Luncheon on Planning for Inherited IRA’s in View of the Recent Supreme Court Case – and Demystifying the “Stretch in Trust” Ira and Pension Rules

Date: Thursday, October 23, 2014 | 4:30 p.m.

Location: Spartan Manor, 6121 Massachusetts Avenue, Port Richey, Florida

Additional Information: For more information, please contact Maria Hixon at hixonm@phsc.edu

**********************************************************

LIVE SARASOTA PRESENTATION:

2014 MOTE VASCULAR SURGERY FELLOWS – FACTS OF LIFE TALK SEMINAR FOR FIRST YEAR SURGEONS

Alan Gassman will be speaking on the topic of ESTATE, MEDICAL PRACTICE, RETIREMENT, TAX, INSURANCE, AND BUY/SELL PLANNING – THE EARLIER YOU START THE SOONER YOU WILL BE SECURE

Date: October 25 – 26, 2014 | Alan Gassman is speaking on Sunday, October 26, 2014

Location: TBD

Additional Information: Please contact agassman@gassmanpa.com for additional information.

**********************************************************

LIVE CLEARWATER PRESENTATION:

TAMPA BAY CPA GROUP

Alan Gassman, Ken Crotty and Christopher Denicolo will be presenting THE MATHEMATICS OF ESTATE PLANNING in a 2 hour session at the Tampa Bay CPA Group Fall 2014 Seminar.

Date: November 7, 2014

Location: Marriott Hotel, 12600 Roosevelt Blvd North, St. Petersburg, FL 33716

Additional Information: For more information please contact Richard Fuller at richardf@fullercpa.com.

**********************************************************

LIVE UNIVERSITY OF NOTRE DAME PRESENTATION:

40th ANNUAL NOTRE DAME TAX & ESTATE PLANNING INSTITUTE

Topic #1: PLANNING WITH VARIABLE ANNUITIES AND ANALYZING REVERSE MORTGAGES

This presentation will cover the unique income tax and financial planning characteristics of fixed and variable annuities.

Topic #2: THE MATHEMATICS OF ESTATE AND ESTATE TAX PLANNING

Christopher J. Denicolo, Kenneth J. Crotty and Alan S. Gassman will also be presenting a special Wednesday late p.m. two hour dive into math concepts that are used or sometimes missed by estate and estate tax planners. This will be an A to Z review of important concepts, intended for estate planners of all levels, sizes and ages. Donald Duck has rated this program A+.

Date: November 13 and 14, 2014

Location: Century Center, South Bend, Indiana

We welcome questions, comments and suggestions on variable annuities, which will be Alan Gassman’s topic for this conference.

Additional Information: The focus of this year’s institute will be on “Business Succession Planning: An Income Tax, Estate Tax and Financial Analysis.” As in past years, several sessions are designed to evaluate certain financial products and tax planning techniques so that the audience can better understand and evaluate these proposals in determining not only the tax and financial advantages they offer, but also evaluate limitations and problems they may cause in the future. Given that fewer clients will need high-end estate tax planning with the $5 million exemptions, other sessions will address concerns that all clients have. For example, a session will describe scams that target elderly individuals and how to protect the elderly from these scams. As part of the objective on refreshing or introducing the audience to areas that can expand their practice, other sessions will review the income tax consequences of debt cancellation, foreclosures, short sales, the special concerns that arise in bankruptcy and various planning available to eliminate the cancellation of debt income or at least defer it with a possible step-up basis at death. The Institute will also continue to have sessions devoted to income tax planning techniques that clients can use immediately instead of waiting to save estate taxes far in the future.

********************************************************

LIVE PORT RICHEY PRESENTATION:

Alan Gassman will be speaking to the North Suncoast Estate Planning Council on Planning Opportunities for Same Sex Couples.

Date: Tuesday, November 18, 2014 | 5:30 p.m.

Location: Seven Springs Gold and Country Club, 3535 Trophy Blvd, Port Richey, FL 34655

Additional Information: For more information please contact agassman@gassmanpa.com.

********************************************************

LIVE FORT LAUDERDALE PRESENTATION:

Alan Gassman will be speaking at the 2015 Representing the Physician Seminar on the topic of DISASTER AVOIDANCE FOR THE DOCTOR’S ESTATE PLAN.

Others speakers include D. Michael O’Leary on Really Burning Hot Tax Topics, Radha V. Bachman on Checklists for Purchase and Sale of a Medical Practice, Cynthia Mikos on Dangers of Physician Recruiting Agreements and Marlan B. Wilbanks on How a Plaintiff’s Lawyer Evaluates Cases Brought by Whistleblowers

Date: January 16, 2015

Location: Renaissance Fort Lauderdale Cruise Port Hotel, 1617 SE 17th Street, Ft. Lauderdale, FL.

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com

********************************************************

LIVE NAPLES PRESENTATION:

2nd ANNUAL AVE MARIA SCHOOL OF LAW ESTATE PLANNING CONFERENCE

Date: Friday, May 1, 2015

Location: Ave Maria School of Law, 1025 Commons Circle, Naples, Florida

Additional Information: Jerry Hesch and Alan Gassman will present The Mathematics of Estate Planning. If you liked Donald Duck in Mathematics Land, you will love The Mathematics of Estate Planning. This will not be a Mickey Mouse presentation.

About their 2 hour presentation:

Enhance your practice and improve your client communications by being able to illustrate the tax savings for a planning technique by using simple to understand illustrative examples.

Attendees will receive a number of easy to use spreadsheet templates, and a free 240 day subscription for unlimited use of the EstateView software that the presenters have developed to enable planners to forecast and illustrate net worth, estate taxes and the impact of various planning techniques, with the ability to have instant and adjustable illustrations using the latest multi-screen and display technology, and customized client specific Word document illustrated letters of explanation produced in seconds.

The use of these spreadsheet examples will also enable you and the client to decide what portion of the client’s investment assets should be retained so that the clients will have the financial security of an income stream no matter how long they live.

Other speakers at the conference include Jonathan Gopman, Bill Snyder, Elizabeth Morgan, Greg Holtz, and others.

Please let us know any questions, comments, or suggestions you might have for this amazing conference, which features dual session selection opportunities in one of the most beautiful conference facilities that we have ever seen.

And don’t forget to have a great weekend in Naples with your significant other or anyone who your significant other doesn’t know! Domino’s Pizza is extra.

NOTABLE SEMINARS BY OTHERS

(We aren’t speaking but don’t tell our mothers!)

LIVE ORLANDO PRESENTATION

49th ANNUAL HECKERLING INSTITUTE ON ESTATE PLANNING

Date: January 12 – 16, 2015

Howard Zaritsky and Lester Law will be giving a fundamentals talk on Monday morning, January 12, 2015 which will include discussion of our JEST trust system. We will be there wearing all of our armor. We take great pride in seeing Lester B. Law of Abbot Downing in Naples, Florida working with Howard on this 3 hour and 15 minute presentation entitled Basis – Banal? Basic? Benign? Bewildering?

The description of this presentation is as follows:

Basis used to be a simple tax concept of only modest importance to estate planners, but recent tax law changes have made income tax planning more important than estate tax planning for some clients, and the use of such techniques as intentional grantor trusts, contingent powers of appointment, private annuities, Alaska community property trusts, joint exempt step-up trusts (JESTs), and trust commutation have made basis sometimes very difficult to determine and even harder to integrate into an estate plan. This session will explore the rules of basis and their increasing importance in estate planning.

Location: Orlando World Center Marriott 8701 World Center Drive, Orlando, Florida

The Google directions from the hotel to the nearest Kentucky Fried Chicken are as follows:

Going back from Kentucky Fried Chicken to the hotel involves the following:

Going back from Kentucky Fried Chicken to the hotel involves the following:

Howard Zaritsky, Lester B. Law, Kentucky Fried Chicken and JESTs – what could be a better experience for your day?

Additional Information: For more information please visit:

https://www.law.miami.edu/heckerling/?op=0

********************************************************

LIVE ST. PETERSBURG PRESENTATION:

ALL CHILDREN’S HOSPITAL FOUNDATION

Date: Thursday, February 12, 2015

Location: St. Petersburg, FL

Additional Information: Please contact Lydia Bennett Bailey at Lydia.Bailey@allkids.org for more information.

********************************************************

LIVE PRESENTATION:

2015 FLORIDA TAX INSTITUTE

Date: Wednesday through Friday, April 22 – 24, 2015

Location: Grand Hyatt Tampa Bay, 2900 Bayport Drive, Tampa, FL 33607

Additional Information: Please contact Bruce Bokor at bruceb@jpfirm.com for more information.

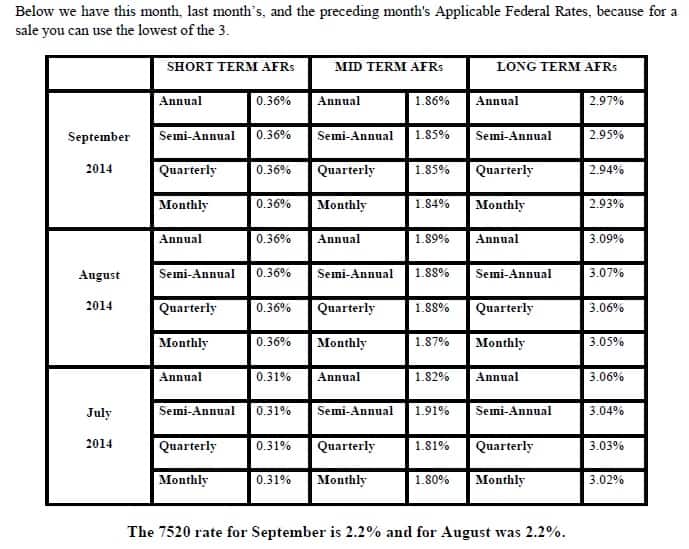

Applicable Federal Rates