The Thursday Report 6.19.2014 – The Monkees Edition

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Janine Gunyan at Janine@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Which Monkees’ songs did Neil Diamond write? The first two readers who give us two Monkees’ songs written by Neil Diamond will receive a special gift, whether they want it or not.

Brandon Ketron is currently entering his third year of law school at Stetson University College of Law, and is a licensed CPA in the State of Virginia. He attended Roanoke College for undergrad where he graduated cum laude with a degree in Business Administration and a concentration in both Accounting and Finance. Brandon plans to pursue an LL.M. in Taxation after successful completion of law school, and then practice in the areas of Estate Planning, Tax, and Corporate and Business Law.

EXECUTIVE SUMMARY

On June 12, 2014, Justice Sonia Sotomayor delivered the opinion of a unanimous Supreme Court in the case of Clark v. Rameker[1] to answer the question of whether assets held under an inherited IRA (and likely other types of qualified retirement plans, such as 401(k)’s would qualify as “retirement funds” under the applicable bankruptcy exemption. The Court held that assets held under an IRA inherited by a non-spouse beneficiary after the death of the IRA owner are not “retirement funds,” and therefore are not protected under federal bankruptcy law.

Debtors who are domiciled in states like Florida, Arizona, Alaska, and Texas, which have statutory creditor protection for inherited IRAs will not be impacted by this decision if they qualify to file bankruptcy in their state of domicile (by having been domiciled there for 730 days prior to filing of a bankruptcy petition), and they elect out of federal bankruptcy exemptions and into the state law exemptions, if applicable. Debtors who live in states that do not have statutes which provide protection for inherited IRAs, or debtors who are domiciled in states that do have such statutes, but have not lived there for 730 days and must therefore file bankruptcy based upon a previous state of domicile, will not be able to exempt inherited IRAs as qualified “retirement funds” as a result of this opinion.

Even where contemplated beneficiaries are anticipated to reside in a state that provides favorable inherited IRA and retirement account creditor exemptions, planners may want to encourage their clients to consider leaving their retirement accounts and IRAs to spendthrift trusts which benefit their intended beneficiaries, in lieu of having such retirement accounts and IRAs payable directly to the beneficiaries.

FACTS:

In 2001, Ruth Heffron died and left an IRA worth about $450,000 to her daughter Heidi Heffron-Clark, a resident of Wisconsin. Heidi elected to take monthly distributions from the IRA as her required minimum distributions. In 2010, Heidi and her husband filed for bankruptcy under Chapter 7 of the Bankruptcy Code, exempting the IRA (then worth around $300,000) under 11 U.S.C. ‘ 522(b)(3)(C). The Clarks’ creditors argued that the inherited IRA did not fall within the meaning of “retirement funds” and thus was not exempt from the bankruptcy estate.

The bankruptcy court ruled in favor of the creditors, stating that inherited IRAs are not “retirement funds, because the funds are not set aside for retirement needs, nor are they distributed upon retirement.” The decision was then appealed to a federal district court. The district court reversed the decision of the bankruptcy court, holding that inherited IRAs do qualify as retirement funds and are exempt from the bankruptcy estate under the ‘ 522(b)(3)(C) exemption. The decision was appealed yet again to the Seventh Circuit, which agreed with the bankruptcy court that inherited IRAs do not qualify for the ‘ 522(b)(3)(C) exemption. This ruling was in conflict with In re Chilton, 674 F.3d 486 (5th Cir. 2012) which held that inherited IRAs were exempt because “the defining characteristic of ‘retirement funds’ is the purpose they are ‘set apart’ for, not what happens after they are ‘set apart’.”

The Supreme Court agreed to hear the case in order to resolve the split in the circuit courts.

The Court found that the language of Title 11 of the United States Code, Section 522(b)(3)(C), which describes protected assets to include “retirement funds” that are “exempt from taxation” under Sections 401, 403, 408, 408A, 414, 457, or 501(a) of the Internal Revenue Code, means that the account has to be characterized as a retirement vehicle for an employee or the contributor and compliant with the rules described in the above referenced Sections.

Further, the Court held that assets held under an IRA inherited by a non-spouse beneficiary are not “retirement funds” that are protected under Section 522(b)(3)(C) because it was Congress’s intent to “help the debtor obtain a fresh start,” and not to provide a windfall to those who would simply inherit by receiving a “free pass.” Specifically, the Court noted that “[a]llowing that kind of exemption would convert the Bankruptcy Code’s purposes of preserving debtors’ ability to meet their basic needs and ensuring that they have a fresh start, into a ‘free pass’.”

The Court went on to note that “inherited IRAs do not operate like ordinary IRAs” because unlike ordinary IRAs or Roth IRAs, the owner of an inherited IRA “not only may, but must withdraw its funds… within 5 years of the original owner’s death or take minimum distributions on an annual basis… and “unlike a traditional or Roth IRA, the owner of an inherited IRA may never make contributions to the account.”

Accordingly, the debtors were not entitled to have their inherited IRA excluded from the bankruptcy estate as an exempt asset, and the assets held under such IRA were subject to the claims of their creditors.

COMMENT:

The Three Characteristics Referenced by the Court: Will They Be Universally Applied?

In reaching its holding, the Court described three characteristics of inherited IRAs that distinguish such accounts from tax advantaged retirement accounts that are considered as held for retirement and are therefore afforded protections from creditor claims under the Bankruptcy Code. While the Court viewed these characteristics in the context of an inherited IRA, other types of accounts (which universally may be thought as creditor exempt) might exhibit these characteristics, and there will doubtlessly be years of litigation and uncertainty as a result of this opinion.

The first characteristic is that a holder of an inherited IRA is not able to invest additional monies into the IRA. It is noteworthy that there are frozen pension plans (that are exempt from taxation under Sections 401, 403, 408, 408A, 414, 457, or 501(a) of the Internal Revenue Code) into which contributions cannot be made, but which are clearly held for retirement.

The second characteristic is that a holder of an inherited IRA is required to withdraw monies from such account upon at least an annual (or more frequent) basis in the form of required minimum distributions. In certain situations, an owner of or participant in a retirement account is required to take withdrawals from the account, such as after the holder reaches age 59 2 or has elected to take distributions from the account over a series of substantially equal periodic payments made at least annually.

The third and final characteristic described by the Court is that a holder of an inherited IRA is permitted to withdraw the entire balance of the account at any time, and for any reason, without penalty. Again, an owner of or participant in a retirement account who has attained age 59 2 is entitled to withdraw as much of the assets from the retirement account as he or she desires, without penalty. Additionally, an owner of or participant in a retirement account may be entitled to withdraw amounts as he or she determines from his or her retirement account without penalty, if such individual meets one or more of the exceptions to the 10% penalty tax for early withdrawals from retirement accounts described in Internal Revenue Code Section 72(t) (such as distributions attributable to the owner/participant being disabled or made for certain medical expenses).

The Court did not provide very much discussion with respect to these characteristics, or how they would apply to retirement accounts that are protected from creditors in bankruptcy. In fact, the only discussion in the opinion of the first characteristic is as follows:

Inherited IRAs are thus unlike traditional and Roth IRAs, both of which are ‘quintessential retirement funds.’ For where inherited IRAs categorically prohibit contributions, the entire purpose of traditional and Roth IRAs is to provide tax incentives for account holders to contribute regularly and over time to their retirement savings.

The Court’s only discussion on the second characteristic was to the effect that the Internal Revenue Code requires the withdrawal of all of the funds in an IRA within five years of the death of the IRA owner, or over the life expectancy of the IRA beneficiary through yearly distributions from the IRA. The Court’s sole analysis of this requirement as it relates to inherited IRAs is “that the tax rules governing inherited IRAs routinely lead to their diminution over time, regardless of their holders’ proximity to retirement, is hardly a feature one would expect of an account set aside for retirement.”

Further, the only discussion on the third characteristic indicates that the 10% penalty tax that applies to the withdrawal of funds from a traditional or Roth IRA before the owner or participant reaches the age of 59 2 encourages individuals to leave the funds untouched until they reach retirement age. Inherited IRAs have no such provisions, and according to the Court, “constitute a pot of money that can be freely used for current consumption, not funds objectively set aside for one’s retirement.” The Court also noted that although the 10% penalty tax does not apply to withdrawals of contributions from a Roth IRA because such contributions are made with after-tax income (i.e., they were already subject to income taxes), withdrawals of any gains or investment income from a Roth IRA are in fact subject to the 10% penalty tax absent the application of a limited exception. This is different from an inherited IRA where no withdrawals of assets are subject to the 10% penalty tax.

It will therefore remain to be seen how and when these three characteristics might be universally applied to retirement accounts to determine what other types of accounts will qualify for protection under the Bankruptcy Code.

To Elect Out of Federal Bankruptcy Exemptions or Not to Elect Out?B That is the Question (Which Could Provide the Solution).

The Court addressed the underlying purpose of the bankruptcy exemptions, in that they “serve the important purpose of ‘protecting the debtor’s essential needs,'” and stated that the principal purpose of the Bankruptcy Code is

“to grant a fresh start to the honest but unfortunate debtor” and “exceptions to discharge should be confined to those plainly expressed.” Thus, it can be expected that bankruptcy exemptions will be construed narrowly by the U.S. Supreme Court. This is contrary to the typical approach taken by state law exemption statutes, which are commonly construed liberally by state courts in favor of the debtor. Specifically, Florida, Arizona, Texas, and Nevada law expressly provide that their respective state law creditor exemptions are to be construed broadly.[2]

As stated above, a debtor who has been domiciled in a state for at least 730 days prior to the filing of a bankruptcy petition (or was domiciled in a state for the 180 day period or greatest portion thereof immediately prior to such 730 period, if his or her domicile has not been located in a single state for such 730 period) may elect to use the state law creditor exemptions afforded by such state in lieu of the federal exemptions. Therefore, debtors who have been domiciled in a state with favorable creditor exemptions for the requisite time period will be inclined to elect of the federal bankruptcy exemptions and choose to have the applicable state exemptions apply, if the applicable state exemptions do not apply by default. Certain states[3] provide that domiciliaries thereof who file for bankruptcy are required to utilize the applicable state law exemptions instead of the federal bankruptcy law exemptions.

In fact, the debtors in this case elected out of the federal exemptions, and the creditor exemptions afforded by their state of domicile (Wisconsin) applied instead of the federal exemptions. However, Wisconsin does not provide for a creditor exemption for assets held under an inherited IRA as certain other states do (such as Florida, Arizona, Alaska, and Texas).[4] If the debtors had been domiciled in Florida rather than Wisconsin, then they would have been required to utilize Florida’s more favorable exemption with respect to inherited IRAs, which would have removed their inherited IRA from the bankruptcy estate.

In this vein, it is important for debtors who are contemplating the filing of a bankruptcy petition to review their state’s creditor exemptions vis-a-vis the federal exemptions to determine whether it would be advantageous to elect out of the federal exemptions and into the applicable state exemptions. Some debtors may want to delay their bankruptcy filing until they are considered as domiciled in a state with more favorable creditor exemption laws.

Are Rollovers by a Surviving Spouse Really Safe in Bankruptcy?

As a result of this decision there will be at least some degree of continuing uncertainty as to whether IRAs inherited by surviving spouses that have been rolled over or are eligible for rollover into the surviving spouse’s own IRA will be exempt under the federal bankruptcy law. The Court did not seem to expressly address this question in its opinion, and perhaps created uncertainty as to whether assets held under IRAs that have been rolled over or are eligible for rollover by a surviving spouse are protected under federal bankruptcy law. One would think that the following language confirms that the Court assumed that such assets would be protected:

The third type of account relevant here is an inherited IRA. An inherited IRA is a traditional or Roth IRA that has been inherited after its owner’s death. See ”408(d)(3)(C)(ii), 408A(a). If the heir is the owner’s spouse, as is often the case, the spouse has a choice: He or she may “roll over” the IRA funds into his or her own IRA, or he or she may keep the IRA as an inherited IRA (subject to the rules discussed below). See Internal Revenue Service, Publication 590: Individual retirement Arrangements (IRAs), p. 18 (Jan. 5, 2014). When anyone other than the owner’s spouse inherits the IRA, he or she may not roll over the funds; the only option is to hold the IRA as an inherited account.

While a number of commentators have noted that a spousal rollover IRA will be protected, the lack of an express statement by the Court will at least create doubt as to this proposition. Additionally, the Court did not discuss whether an IRA inherited by a spouse that has not yet been rolled over but is eligible for rollover by such spouse will be eligible for the federal creditor exemption for retirement funds. A spousal rollover of an inherited IRA may be effectuated through passive acts, such as the failure to take a required minimum distribution from the decedent’s IRA, in addition to affirmative acts, such as the re-titling of the inherited IRA, the addition of assets to the inherited IRA or a transfer of the assets in the inherited IRA into the spouse’s own IRA. Further, there is no time limit as to when a surviving spouse can roll over an IRA from his or her spouse into his or her own IRA.[5] The IRS has permitted a surviving spouse to roll over an IRA into her own IRA even though she was treated as a beneficiary of the inherited IRA for two tax years following her late husband’s death.[6]

Accordingly, what is the treatment of assets held under an inherited IRA that has passed to a surviving spouse before the spouse has rolled over the inherited IRA? Further, if the surviving spouse effectuates a rollover while she has creditors or an impeding bankruptcy, is it a fraudulent transfer?

The Court’s failure to address these questions will thus create uncertainty with respect to IRAs inherited by surviving spouses.

Spendthrift Accumulation Trusts – The Answer, and Perhaps a Panacea.

Well versed practitioners already know that retirement accounts and IRAs can be made payable to spendthrift “Accumulation Trusts” which can provide for beneficiaries without being subject to their creditor claims, and stretch out the required minimum distributions from the retirement account or IRA over the life expectancy of the oldest beneficiary of the trust (referred to as the “Designated Beneficiary” under the Regulations).

The Treasury Regulations and a number of Private Letter Rulings have approved the use of discretionary or ascertainable standard trusts as beneficiaries of the retirement accounts and IRAs in order to avoid the 5-year minimum distribution rule.[7] A trust can therefore be structured so that the beneficiaries can only receive distributions as determined by an independent trustee, and can have a spendthrift provision that would prevent the creditors of a beneficiary from reaching the assets of the trust. The trust can receive the retirement account or IRA of the decedent, and the required minimum distributions can be “accumulated” by the trustee for distribution to the beneficiary only if and when the trustee deems it to be appropriate. The life expectancy of the oldest beneficiary of the trust will be used to determine the amount of the required minimum distributions that must be made each year so that, for federal income tax purposes, it is treated similar to the oldest beneficiary having been directly named as the retirement account or IRA beneficiary.

Naming an Accumulation Trust with a spendthrift provision as the beneficiary of a retirement account or IRA will enable the protection of the beneficiaries and their descendants from potential divorce claims, child support claims, poor self-management, and/or spendthrift tendencies. Further, using an Accumulation Trust as a receptacle to receive a retirement account or IRA on the death of the participant/owner can provide creditor protection for those beneficiaries who live outside of states that have exemptions for inherited IRAs. Many practitioners will continue to make the mistake of assuming that all beneficiaries will be protected if the law of the state where the retirement account or IRA participant/owner provides protection, notwithstanding that the creditor exemption status of an inherited IRA will be determined by the law of the state where the beneficiary resides, which cannot be definitely known before the death of the retirement account or IRA participant/owner.

Moreover, a retirement account or IRA that is inherited directly by an individual will be subject to federal estate tax in such individual’s estate, which will not be the case if inherited under an Accumulation Trust that is generation-skipping tax exempt. A beneficiary of an inherited retirement account or IRA typically cannot name his or her own beneficiaries that would inherit such account in the event of the beneficiary’s death before the account is exhausted. However, a beneficiary of an Accumulation Trust can have a power of appointment over the assets of the Trust that will in effect allow the beneficiary to control the disposition of the retirement account or IRA after his or her death.

Planners will want to be careful with drafting powers of appointment under Accumulation Trusts because the ages of the possible appointees are taken into account in determining the Designated Beneficiary under the Trust whose life expectancy will control the amount of the annual required minimum distributions. The authors recommend drafting the power of appointment under the Trust so that it may only be exercisable in favor of individuals who are younger than the applicable beneficiary of the Trust in order to prevent a more rapid required minimum distribution schedule from applying.

There is a downside to having a retirement account or IRA payable to an Accumulation Trust instead of having it payable directly to a surviving spouse. The surviving spouse is unable to roll over the retirement account or IRA into his or her own if it is made payable to an Accumulation Trust. This would result in the surviving spouse being required to take larger required minimum distributions each year than if he or she rolled over the decedent’s retirement account or IRA into his or her own.

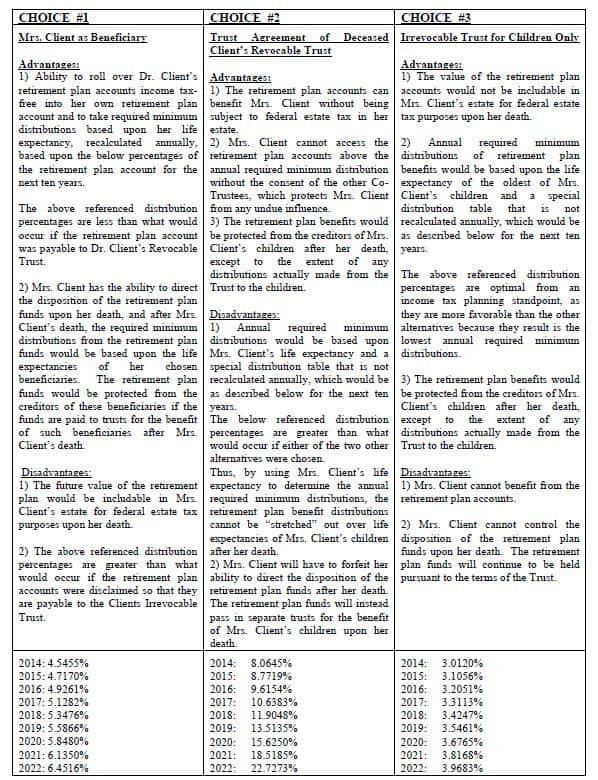

One way to mitigate this downside and to provide for flexibility is to name the surviving spouse directly as the primary beneficiary of the retirement account or IRA, to name an Accumulation Trust for his or her benefit as the secondary beneficiary, and to name an Accumulation Trust established for the benefit of the children and other descendants as the tertiary beneficiary. The surviving spouse could then disclaim all or a portion of the retirement account or IRA into the Accumulation Trust and remain a beneficiary thereof (albeit without a power of appointment), and the trustee of such Trust could further disclaim all or a portion of the retirement account or IRA into an Accumulation Trust for the descendants if the surviving spouse is not in need of the retirement benefits.

Thus, with appropriate disclaimer language, the family and advisors can decide after the decedent’s death whether to have the retirement account or IRA pass (1) directly to the surviving spouse as a rollover IRA; (2) to an Accumulation Trust for the surviving spouse so that payments will come out over the life expectancy of the spouse; or (3) to an Accumulation Trust for a child or children so that the payments will come out over the life expectancy of the oldest child who is a beneficiary of the Trust.

The following chart that shows the required minimum distribution percentages that would apply in each of the three scenarios described above, and the advantages and disadvantages of each scenario, based upon a 75-year-old surviving spouse and the oldest child being 50 years old at the time of the decedent’s death:

CONCLUSION:

Notwithstanding the negative result for the debtor, this Supreme Court decision may do more good than harm by propelling estate planning practitioners and advisors to encourage clients to leave retirement accounts and IRAs into properly structured Accumulation Trusts. Another consequence of this decision will be that many state legislatures will undoubtedly consider the question of providing state law exemption for inherited IRAs so that the bankruptcy will protect these for state citizens who file bankruptcy.

This Court decision provides certainty for retirement accounts and IRAs inherited by individuals other than surviving spouses, but unfortunately also exposes inherited retirement accounts and IRAs of many Americans that are in bankruptcy or might be contemplating bankruptcy. The ramifications of the opinion should cause many Americans with substantial retirement accounts or IRAs to update their estate planning documents and beneficiary designations to protect their children or other beneficiaries from creditors. Further, this case puts the burden on practitioners to carefully navigate the Treasury Regulations and literature on using Accumulation Trusts in order to provide for the creditor protection of retirement accounts and IRAs while avoiding application of the requirement that all retirement account and IRA benefits be distributed within 5 years of the decedent’s death.

The decision does not provide as much certainty as the authors hoped that it would for spousal rollover retirement accounts and IRAs, but it seems probable that they will be protected in bankruptcy. It is also important to remind clients and advisors that this decision will virtually have no impact with respect to beneficiaries who reside in states that have statutes that protect inherited retirement accounts and IRAs as creditor exempt.

Nevertheless, this decision stresses the importance of planners making sure to provide their clients with the advantages and disadvantages (both tax and non-tax) applicable to the various methods of structuring beneficiary designations of retirement accounts and IRAs.

________________________________________

[1] Clark v. Rameker, 573 U.S. _____ (2014)

[2] Goldenberg v. Sawczak, 791 So. 2d 1078, 1081 (Fla. 2001); Gardenhire v. Glasser, 226 P. 911, 912 (Ariz. 1924); Hickman v. Hickman, 234 S.W.2d 410, 413 (Tex. 1950); In re Christensen, 149 P.3d 40, 43 (Nev. 2006).

[3] These states are Alabama, Alaska, Arizona, California, Colorado, Delaware, Florida, Georgia, Idaho, Illinois, Indiana, Iowa, Kansas, Kentucky, Louisiana, Maine, Maryland, Mississippi, Missouri, Montana, Nebraska, Nevada, New Hampshire, New York, North Carolina, North Dakota, Ohio, Oklahoma, Oregon, South Carolina, South Dakota, Tennessee, Utah, Virginia and Wyoming.

[4] Fla. Stat. ‘ 222.21; Ariz. Rev. Stat. ‘ 33-1126; Alaska Stat. Ann. ‘ 09.38.017; Tex. Prop. Code ‘ 42.0021

[5] Treas. Reg. _ 1.408-8, A-5(a).

[6] PLR 9534027.

[7] Treas. Reg. ‘ 1.401(a)(9); PLR 200438044; PLR 200228025

TO REGISTER FOR THIS WEBINAR PLEASE CLICK HERE

TO REGISTER FOR THIS WEBINAR PLEASE CLICK HERE

IRS Commissioner Says Taxpayers Have Rights

by Denis Kleinfeld

IRS Commissioner John A. Koskinen has announced that “respecting taxpayer’s rights continues to be a top priority for IRS employees…”

I bet you didn’t know that your rights as a taxpayer were one of the IRS’s top priorities. In fact, according to Nina Olsen, the National Taxpayer Advocate for the IRS, “…taxpayer surveys conducted by my office have found that most taxpayers do not believe they have rights before the IRS and even fewer can name their rights.”

There are in fact three separate laws and each one is called “the Taxpayer Bill of Rights”—The Taxpayer Bill of Rights #1 (1988), the Taxpayer Bill of Rights #2 ((1996), and the Taxpayer Bill of Rights #3 (1998).

Sound confusing?

Of course it is. This is your federal tax law. Nothing done by Congress is intended to be fathomable by taxpayers, or, for that matter, understandable by the IRS employees.

There is nothing new in this new list of taxpayer rights. It is just a list of 10 aspirational concepts meant to educate taxpayers. At best, this is merely a symbolic gesture.

There are no new rights that do not already exist buried someplace in the tax code, and there are no new enforcement protocols or safeguards to help make sure that the IRS respects whatever rights a taxpayer may have.

Curiously, this public relations announcement does not mention any of the specific rights which taxpayers would find helpful. For example, the right to make an audio recording of any interview, or the right to have the Taxpayer Advocate (previously named the IRS Ombudsman) intervene in an enforcement action if the taxpayer is “suffering or about to suffer a significant hardship as the result of the manner in which the Internal Revenue Service is operating.”

What are the 10 core concepts that the IRS Commissioner is touting as part of an effort to regain the taxpayers’ trust in the tax system?

1. The Right to be Informed. That is, somebody from the IRS is going to let you know you are in a world of hurt and that the process is going to be painful.

2. The Right to Quality Service. This should be interesting since the National Taxpayer Advocate told Congress that the IRS is badly underfunded, undermanned, and overburdened with a complex tax law that is incomprehensible under the best of circumstances and far more work than it can handle. Practitioners are commonly faced with situations where IRS personnel simply cannot or will not respond to requests to fix IRS errors, or to give guidance in situations where taxpayers are being wrongly treated or inconvenienced.

3. The Right to Pay No More than the Correct Amount of Tax. A highly unlikely occurrence since dealing with the IRS is an intense adversarial process where they are presumed to be correct and the taxpayer is presumed to be wrong. In other words, the game is rigged.

4. The Right to Challenge the IRS’s Position and Be Heard. Basically, you can tell them you object to being robbed and they can tell you to stuff it.

5. The Right to Appeal an IRS Decision in an Independent Forum. This means you can take the case to Appeals where the appeals’ officer is an employee of the IRS and even to the Tax Court where the judges are either former IRS people or government prosecutors.

6. The Right to Finality. Even if you are dead, the IRS will go after your estate.

7. The Right to Privacy. Meaning that the IRS will be only as intrusive as they want, and will provide each taxpayer with the amount of due process as Congress has allowed in passing the tax statutes. Effectively, the taxpayers will have more privacy in a hostile divorce than a tax audit.

8. The Right to Confidentiality. Think Lois Lerner or what it would be like appearing before Senator Levin’s Subcommittee on Permanent Investigations.

9. The Right to Representation. This is at your own expense. Tax professionals do not come cheap.

10. The Right to a Fair and Just Tax System. Well, the United States doesn’t have one. The taxpayers and the people working at the IRS are both made victims by Congress, confusion, and underfunding.

While I can appreciate the IRS Commissioner’s good intentions in publicly expressing that taxpayers have rights, it is clearly a futile bureaucratic effort to try and rectify a tax system that is fundamentally and profoundly beyond hope.

We are pleased to announce the publication of our two latest books, The Florida Legal Guide for Same Sex Couples – a layman edition, and The Florida Advisor’s Guide to Counseling Same Sex Couples – a professional edition.

For a discount use the top secret 20% off promotional code K2UQPYWT and click here to order the Professional Version ] or here to order the layman version.

Please send us your questions, comments and suggestions on topics related to these books for possible publication, or we might just laugh at you!

![]()

LIVE CLEARWATER PRESENTATION:

FICPA SUNCOAST CHAPTER MONTHLY MEETING

Alan S. Gassman will be speaking at the FICPA Suncoast Chapter’s monthly meeting on HOW TO PLAN, STRUCTURE, AND PROTECT WEALTH USING REVOCABLE AND IRREVOCABLE TRUSTS AND TRUST SYSTEMS. A COMPREHENSIVE OVERVIEW WITH A PRACTICAL PLANNING CHECKLIST AND PRACTITIONER TAX COMPLIANCE GUIDE.

Speaker: Alan S. Gassman

Date: TODAY, June 19, 2014 | 4:00 p.m. (100 minute presentation)

Location: Feather Sound Country Club, Clearwater, Florida

Additional Information: For more information, to register and a discount code please email agassman@gassmanpa.com

********************************************************

FREE LIVE WEBINAR:

A POWERFUL 40 MINUTE DOUBLE HEADER WITH JONATHAN BLATTMACHR

Topics:

- Foreign vs. Domestic Asset Protection Trusts: More Than Just Creditor Protection Considerations

- Empowering Your Powers of Appointment: Don’t Leave Out Important Tax and Practical Provisions or Ignore Important Considerations. With Sample Provisions

Date: Tuesday, August 12, 2014 | 12:00 p.m.

Location: Online webinar

Additional Information: To register for the webinar please click here.

********************************************************

LIVE FT. LAUDERDALE PRESENTATION:

FICPA ANNUAL ACCOUNTING SHOW

Alan Gassman will be speaking at the FICPA Annual Accounting Show on Thursday, September 18, 2014 on the topic of ESSENTIAL GUIDE TO BASIC TRUST PLANNING for 50 minutes.

This presentation will introduce basic and intermediate trust planning background and provide attendees with an orderly list of the most commonly used trusts, practical features and traps for the unwary, including revocable, irrevocable and hybrid. The discussion will include tax, creditor protection and probate and guardian considerations.

Date: Wednesday, September 17 through Friday, September 19, 2014

Location: Fort Lauderdale, Florida

Additional Information: For more information about this program please contact Stephanie Thomas at ThomasS@ficpa.org

********************************************************

LIVE NEW JERSEY PRESENTATION:

NEW JERSEY INSTITUTE FOR CONTINUING LEGAL EDUCATION (ICLE) SPECIAL 3 HOUR SESSION

Alan Gassman will be the sole speaker for this informative 3 hour program entitled WHAT NEW JERSEY LAWYERS NEED TO KNOW ABOUT FLORIDA LAW

Here is some of what the New Jersey Bar Invitation for this program provides:

New Jersey residents have always had a strong connection to Florida. We vacation there (it’s our second shore). Own Florida property (or have favored relatives that do) and have family and friends living there. Sometimes our wealthiest clients move to Florida and need guidance, and you need background in order to continue representation.

There are real and significant differences between the two states that every lawyer should be cognizant of. For example, holographic wills are perfectly legitimate in New Jersey and anyone can serve as an executor of an estate, which is not the case in Florida. Also, Florida’s new rules regarding LLCs are different, and if you are handling estates of New Jersey decedents who owned Florida property, there are Florida law issues that must be addressed. Asset protection differs significantly in Florida too.

Attendees will receive Mr. Gassman’s book entitled Florida Law for Tax, Business and Financial Planning Advisors, which has a retail value of $34.95.

Our informative seminar, presented by Clearwater attorney Alan Gassman, highlights issues New Jersey lawyers should be aware of when handling matters for New Jersey residents who own Florida property, reside there part time, have interest in Florida businesses, or who are considering a move to Florida. The Florida Bar rules permit out of state lawyers to continue representation of Florida residents under rules that will be discussed.

Gain the knowledge you need to assist your clients with Florida matters, including:

- Florida specific laws involving businesses, trusts, and estates

- Florida tax planning

- Elective share and homestead rules

- Liability Insulation and Planning

- Creditor Protection and Strategies

- Medical Practice Laws

- Staying within Florida Bar Guidelines that allow representation of Florida clients

Comments from past attendees of this program:

- Excellent seminar and materials!!!

- This was one of the best ICLE seminars yet!

- One of the best seminars I have attended.

- Better than mashed potatoes and gravy. Glad he didn’t serve grits!

Date: Saturday, October 4, 2014

Location: TBD

Additional Information: This is a repeat of the same program that we gave last year, but our book is now updated for the new Florida LLC law and changes in estate and trust law. Please tell all of your friends, neighbors and enemies in New Jersey to come out to support this important presentation for the New Jersey Bar Association. We will include discussions of airboats, how to get an alligator off of your driveway, how to peel a navel orange and what collard greens and grits are. For additional information please email agassman@gassmanpa.com

********************************************************

LIVE PASCO COUNTY PRESENTATION:

Alan Gassman, Christopher Denicolo and Kenneth Crotty will be speaking at the Pasco-Hernando State College’s Planned Giving Consortium Luncheon on Hot Topics and Creditor Protection including Inherited IRAs and Planning for Same Gender Couples.

Date: Thursday, October 23, 2014 | Time to be determined

Location: TBD

Additional Information: For more information please contact Maria Hixon at hixonm@phsc.edu

**********************************************************

LIVE UNIVERSITY OF NOTRE DAME PRESENTATION:

40th ANNUAL NOTRE DAME TAX & ESTATE PLANNING INSTITUTE

Please send us your questions, comments and suggestions for Alan Gassman’s talk on Planning with Variable Annuities and Analyzing Reverse Mortgages.

This presentation will cover the unique income tax and financial planning characteristics of fixed and variable annuities, and provide estate and tax planners with a number of strategies for understanding and planning with existing and contemplated contracts. With over One Trillion Dollars of US taxpayer money invested in annuity contracts, more and more clients are showing up in their estate planners’ offices with large annuity contracts and common misunderstandings about “guaranteed income” and “guaranteed rates of return” features. The presentation will cover common policy features, what is actually happening inside of a policy, illustration techniques, and changes that can be made to defer income tax and reduce overall tax liability. Minimum distribution rules that apply to variable annuity contracts will also be discussed.

Date:November 13 and 14, 2014

Location: Century Center, South Bend, Indiana

We welcome questions, comments and suggestions on variable annuities, which will be Alan Gassman’s topic for this conference.

Additional Information: The focus of this year’s institute will be on “Business Succession Planning: An Income Tax, Estate Tax and Financial Analysis.” As in past years, several sessions are designed to evaluate certain financial products and tax planning techniques so that the audience can better understand and evaluate these proposals in determining not only the tax and financial advantages they offer, but also evaluate limitations and problems they may cause in the future. Given that fewer clients will need high-end estate tax planning with the $5 million exemptions, other sessions will address concerns that all clients have. For example, a session will describe scams that target elderly individuals and how to protect the elderly from these scams. As part of the objective on refreshing or introducing the audience to areas that can expand their practice, other sessions will review the income tax consequences of debt cancellation, foreclosures, short sales, the special concerns that arise in bankruptcy and various planning available to eliminate the cancellation of debt income or at least defer it with a possible step-up basis at death. The Institute will also continue to have sessions devoted to income tax planning techniques that clients can use immediately instead of waiting to save estate taxes far in the future.

********************************************************

LIVE NAPLES PRESENTATION:

2nd ANNUAL AVE MARIA SCHOOL OF LAW ESTATE PLANNING CONFERENCE

Date: Friday, May 1, 2015

Location: Ave Maria School of Law, 1025 Commons Circle, Naples, Florida

Additional Information: Jerry Hesch and Alan Gassman will present The Mathematics of Estate Planning. If you liked Donald Duck in Mathematics Land you will love The Mathematics of Estate Planning. This will not be a Mickey Mouse presentation.

Other speakers include Jonathan Gopman, Bill Snyder, Elizabeth Morgan, Greg Holtz, and others.

Please let us know any questions, comments, or suggestions you might have for this amazing conference, which features dual session selection opportunities in one of the most beautiful conference facilities that we have ever seen.

And don’t forget to have a great weekend in Naples with your significant other, or anyone who your significant other doesn’t know! Domino’s Pizza is extra.

LIVE ORLANDO PRESENTATION

49th ANNUAL HECKERLING INSTITUTE ON ESTATE PLANNING

Date: January 12 – 16, 2015

Location: Orlando World Center Marriott 8701 World Center Drive, Orlando, Florida

Additional Information: For more information please visit: https://www.law.miami.edu/heckerling/?op=0

********************************************************

LIVE ST. PETERSBURG PRESENTATION:

ALL CHILDREN’S HOSPITAL FOUNDATION

Date: Thursday, February 12, 2015

Location: St. Petersburg, FL

Additional Information: Please contact Lydia Bennett Bailey at Lydia.Bailey@allkids.org for more information.

********************************************************

LIVE PRESENTATION:

2015 FLORIDA TAX INSTITUTE

Date: Wednesday through Friday, April 22 – 24, 2015

Location: TBD

Additional Information: Please contact Bruce Bokor at bruceb@jpfirm.com for more information.