The Thursday Report – 3.24.16 – Form 8971, Alimony, Guns, and Other Fun!

Florida’s New Alimony Act – Great News for Most Floridians

Backyard Gun Range Bill Signed by Governor Scott

A Refresher on Fiduciary Duties for Directors and Officers

Form 8971 Initial Deadline Update – The IRS Kicks the Can Down the Road Even Further, Delaying the Need to Report & Strictly Adhere to Basis Information as Filed in a Required Estate Tax Return

A Simple Formula to Engage Your Team to Reach a Goal by David Finkel

Richard Connolly’s World – A Focus on Estate & Tax Planning

Thoughtful Corner – Don’t Forget Your Contact Information!

Humor! (or Lack Thereof!)

We welcome contributions for future Thursday Report topics. If you are interested in making a contribution as a guest writer, please email Stephanie at stephanie@gassmanpa.com.

This report and other Thursday Reports can be found on our website at www.gassmanlaw.com.

Quote of the Week

“Success is no accident. It is hard work, perseverance, learning, studying, sacrifice,

and, most of all, love of what you are doing.”

– Pelé

Edson Arantes do Nascimento, also known as Pelé, is a retired Brazilian professional footballer (soccer player) who played as a forward. He is widely regarded as the greatest football (soccer) player of all time and was voted World Player of the Century by the International Federal of Football History and Statistics (IFFHS) in 1999. According to the IFFHS, Pelé is the most successful league goal scorer in the world, with 541 league goals. In total, Pelé scored 1281 goals in 1363 games, earning him a place in the Guinness World Records for most career goals scored in the sport. The President of Brazil named Pelé a national treasure in 1961. Since retiring from the sport in 1977, Pelé has been a worldwide ambassador for football.

We thank Ray Howard of Ray Howard & Associates for this quote and for being our favorite (and possibly only!) fan.

Florida’s New Alimony Act – Great News for Most Floridians

by Alan S. Gassman and Seaver Brown

Leave your honey on or before October 1st,

When the alimony, like your marriage, will be for better or for worse.

Florida’s new law will not disparage,

Judges who calculate alimony at the end of a marriage.

One of the big problems under Florida law has been the lack of guidelines and consistency when it comes to setting alimony in the event of a divorce. As a result, legal and expert fees can skyrocket, and judges who do not have significant financial or mathematical experience can become confused and will render decisions that are extremely disappointing to one spouse and more than fair to the other.

The Florida Legislature has wisely passed new alimony reform rules in Senate Bill 668, which provides specific and relatively easy to follow guidelines with respect to both (1) the amount of alimony as an equal annual payment; and (2) the number of years that it would be paid over. To see a copy of the new Bill, please click here.

As of today, Senate Bill 668 has been passed by both the Florida House and Senate and now only awaits the signature of Governor Rick Scott before it would become effective on October 1, 2016.[1] This new bill will amend several different Florida Statutes that address various aspects of alimony duration, alimony amounts, child support, parenting plans, and time-sharing.[2]

The alimony reform bill would effectively make permanent alimony a thing of the past. Instead, it mandates that judges use certain calculation guidelines when determining how much alimony to award a spouse based on the length of a marriage and the respective income of each party. If the judge deviates from the prescribed calculation guidelines, they must explain why in a separate writing.

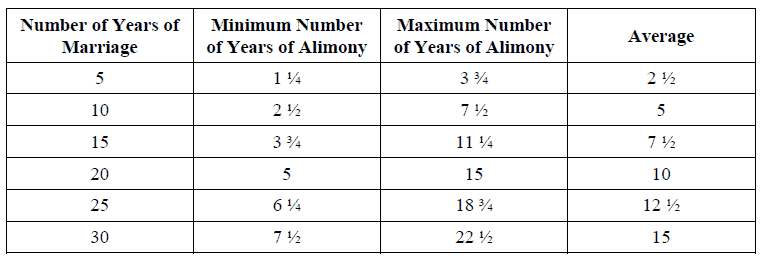

The new statute basically provides that the length of alimony, meaning the number of years after divorce that annual payments would be made, will be between 25% and 75% of the number of years that the parties were married. Therefore, the following would apply, assuming that a divorce would occur after the stated number of years married:

The statute further provides a new formula to calculate the amount of alimony payments that one spouse must make to the other. Prior to this, however, the court is asked to determine the amount of each party’s monthly gross income, including actual and potential income of both non-marital and marital property distributed to each party, and to use the difference between these two numbers.

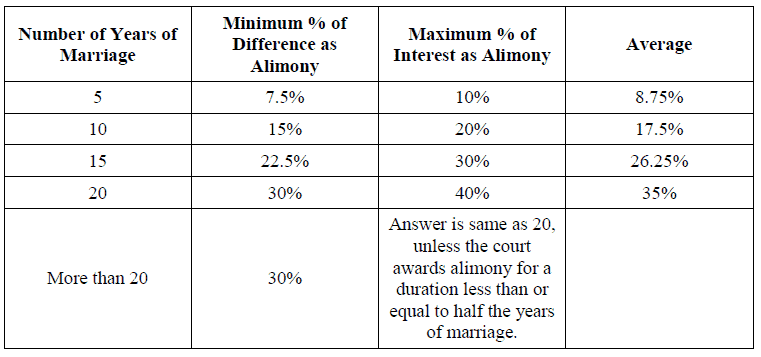

To calculate the alimony amount range, the court uses a formula comprised of the parties’ difference in gross income and years of marriage multiplied by either 1.5% for the low end or 2% for the high end as follows:

- Low End: (0.015 x the number of years of marriage) x the difference in gross income

- High End: (0.020 x the number of years of marriage) x the difference in gross income

For purposes of calculating the alimony amount range, couples who were married for 20 years or more are limited to 20 years of marriage when calculating both the low and high ends of alimony amounts.[3] However, if the court establishes an alimony duration that is equal to or less than half the length of marriage, the court must use the actual years of marriage for the high end alimony amount, up to a maximum of 25 years. Therefore, if a couple was married for 30 years and the court awards one spouse alimony for only 10 years, the court will multiply by 20 for the low end calculation and by 25 for the high end calculation. Furthermore, if the formulas result in a negative number, the alimony amount will be $0.

The following chart can be used to demonstrate how the statute will work:

To illustrate these concepts, here are three examples of how these numbers can work:

Example 1

Mary and John are married for 15 years. Mary earns $250,000 a year, and John earns $150,000 a year. The difference is $100,000.

The minimum and maximum number of years of alimony will be 3.75 years and 11.25 years, respectively. The average is 7.5 years. The minimum annual alimony will be $22,500 [(0.015 x 15) x $100,000]. The maximum annual alimony will be $40,000 [(0.020 x 20) x $100,000].

Example 2

Same facts as Example 1, except now Mary and John have been married for 25 years.

The minimum and maximum number of years of alimony will be 6.25 years and 18.75 years, respectively. The average is 12.5 years. The minimum annual alimony will be $30,000 [(0.015 x 20) x $100,000]. The maximum annual alimony will be $40,000 [(0.020 x 20) x $100,000].

Example 3

Same facts as Examples 1 and 2, except now Mary and John have been married for 40 years.

The minimum and maximum number of years of alimony will be 10 years and 30 years, respectively. The average is 20 years. Assume that the court awards John with only 15 years of alimony, which is less than half the number of years Mary and John were married.

The minimum annual alimony will be $30,000 [(0.015 x 20) x $100,000]. The maximum annual alimony will be $50,000 [(0.020 x 25) x $100,000].

Senate Bill 668 also contains new time-sharing language for parents which requires courts to presume that 50/50 custody is in the best interests of the child. Of course, this is only a presumption that the court must use as a starting point when determining the parenting plan and time-sharing schedule between parents. However, a court must always consider what is in the best interests of the child and will evaluate all factors that affect the welfare and interests of the child, along with the specific circumstances surrounding each family.

Both of these proposed changes have been met with much resistance over the years, and it remains to be seen whether Governor Scott will sign the bill this year or veto it as he did with another proposed alimony reform bill in 2013.

As a result of this statute, there will probably be more divorces than normal filed after October 1, because those who have contemplated leaving a marriage will have more certainty and less in attorney and expert fees to calculate their alimony.

To order flowers for your honey from Publix, call (727) 712-3450, extension 234.

*******************************

[1] Article III, section 8 of the Florida Constitution provides in part that, when the Legislature is in session, the Governor has 7-days following presentation of a bill to sign or veto the bill. If the Legislature adjourns sine die before the bill is presented to the Governor or while the bill is in the Governor’s possession, the Governor has 15 days from the date of presentation to sign or veto. If the Governor does not sign or veto within either of those time frames the bill will become law. Regular sessions of the Legislature begin on the first Tuesday after the first Monday in March and continue for 60 consecutive days.

[2] The following Florida Statute Sections will be amended as a result of this bill: §61.071, §61.08, §61.13, §61.14, §61.30, §61.192, §61.1827, and §409.2579.

[3] See Example 2 in the same article.

Backyard Gun Range Bill Signed by Governor Scott

by Alan Gassman and Seaver Brown

Governor Scott has signed the “Backyard Gun Range Bill” that was passed by the House and Senate as Senate Bill 130. Its purpose was to restrict individuals from discharging firearms in certain residential areas.

More specifically, it bans individuals from engaging in acts such as recreational target shooting and celebratory shooting in areas with a density of one or more residential dwellings per acre. The Bill also imposes a first degree misdemeanor charge for those individuals who violate the law, punishable by up to one year in jail and a $1,000 fine.

The Bill has three exceptions that will cause it to not apply: (1) to a person lawfully defending life or property or performing official duties requiring the discharge of a firearm; (2) if, under the circumstances, the discharge does not pose a reasonably foreseeable risk to life, safety, or property; or (3) accidental discharge of a firearm.

One of the primary reasons for passing this bill was to keep people from constructing gun ranges in their backyards, which left neighbors understandably concerned for their safety. However, the impact of the Bill is diffused for those who will claim the second exception above. In the past, law enforcement officers and their attorneys expressed concern over the prior rule being too subjective and vague, which only prohibited an individual from “recklessly or negligently discharging a firearm.”[1]

The Bill will therefore have many critics, but will enable law enforcement officers to make a determination as to whether a reasonably foreseeable risk exists where bullets might travel to occupied areas, or hit children or pets that might pass through the line of fire.

Our book entitled, The Legal Guide to NFA Firearms and Gun Trusts, is available on Amazon, and was co-written by Sean Healy, Alan S. Gassman, Lee-ford Tritt, Jonathan Blattmachr, and Kenneth J. Crotty. Our new edition, which covers the requirements for trusts and individuals possessing or using automatic weapons, silencers (“suppressors”), and other Title II firearms is available now as a PDF, and will be available next month on Amazon. Don’t leave home without it! Those who buy the Amazon edition from today forward will receive a free PDF of the post-July 13, 2016 rules. Any and all clients having automatic weapons or suppressors should review and quite possibly update their trusts, or quickly establish a trust, before the more stringent July 13th rules apply.

Click here to see our book on Amazon.

***************************

[1] http://www.heraldtribune.com/article/20140201/WIRE/140209997?p=4&tc=pg.

A Refresher on Fiduciary Duties for Directors and Officers

by Alan Gassman and Lydia Greiner

Florida’s Limited Liability Company Act is intended to give the maximum effect to the concept of freedom of contract. In the formation and enforceability of an LLC’s operating agreement, the statute allows a wide berth for parties to create and structure their company as they see fit.[1] The LLC statute merely serves to provide default provisions for parties to use where they have not agreed to certain elements or functions for the entity. However, the statute does not have all of the answers and, in a situation where the parties have not expressed an agreement and the statute is silent, a court will apply the principles of law and equity to resolve an issue.[2]

Although the Florida statute provides great flexibility for parties, there are some limitations on the freedom of contract related to fiduciary duties and obligations. For example, the statute provides that each manager of a manager-managed LLC and each member of a member-managed LLC owes fiduciary duties of loyalty and care to both the LLC and its members.[3] Further, Florida law provides that an LLC operating agreement may not eliminate the duty of loyalty, the duty of care, or the obligations of good faith and fair dealing as set forth in § 605.4091. The operating agreement, however, may provide reasonable standards to measure these obligations against.[4]

The standards of conduct prescribed by statute for members and managers in the LLC limits the fiduciary duty of loyalty.[5] The statute delineates boundaries for the fiduciary duty of loyalty:

(2) The duty of loyalty is limited to:

(a) Accounting to the [LLC] and holding as a trustee for it any property, profit, or benefit derived by the manager or member, as applicable:

1. In the conduct or winding up of the company’s activities and affairs;

2. From the use by the member or manager of the company’s property; or

3. From the appropriation of a company opportunity;

(b) Refraining from dealing with the company in the conduct or winding up of the company’s activities and affairs as, or on behalf of, a person having an interest adverse to the company, except to the extent that a transaction satisfies the requirement of this section; and

(c) Refraining from competing with the company in the conduct of the company’s activities and affairs before the dissolution of the company.[6]

In a situation where the duties of loyalty and care have not been modified or eliminated from the standards of conduct provided by statute, directors and officers of the entity – or managers, in a manager-managed, and members, in a member-managed LLC – owe both the duties of loyalty, care, and shoulder the obligation of acting with good faith and fair dealing on behalf of the company and its members.[7]

These responsibilities require, among other things, that an individual serving the LLC – such as an officer, manager, director, or member in a member-managed LLC – has a duty to not compete with the company or engage in an activity that may be adverse to the entity. For example, if an officer hired a business broker to solicit the sale of his or her portion of the company without disclosing the action to the other members, it would likely breach his or her fiduciary duty of loyalty. The sale of his or her share in the company would likely be considered a “company opportunity” because of the potential benefits from the sale and the failure to disclose material information related to the search for a buyer may be viewed as depriving the LLC and its members of an opportunity.

Further, secretly attempting to sell a portion of the company would likely cause the individual to fail in meeting his or her obligations of good faith and fair dealing. If he or she were to sell the portion of the company, in addition to the monetary benefit he or she may receive, it could trigger the loss of other financial benefits for the company. Whether selling his or her interest would be adverse to the company and not “in good faith” depends on if he or she “reasonably relieve[d] [it] to be in the best interest” of the company.[8] An individual serving an LLC has a duty to ensure that any agreements made on behalf of the company are “fair and reasonable…to the corporation at the time [the agreement] is authorized.”[9]

To determine if a breach of fiduciary duty occurred, courts often look at a variety of factors. The Fourth District Court of Appeals in Old Port Cove Property Owners Association v. Eccelstone, determined whether a breach occurred by examining factors, including the presence of secrecy, fraud, inordinate profit, or unjust enrichment.[10] In Old Port, the court held that there was not a breach of fiduciary duty because it was unable to find any of the aforementioned factors, the developer in his officer-like capacity, disclosed the contract at issue, and it was approved by the organization’s members prior to finalization.

In contrast, the Grossman v. Greenburg case serves as an example of where the court found a breach of fiduciary duty.[11] In Grossman, the defendants failed to disclose a sales commission to the other members in the partnership and “secretly divided” a $450,000 note amongst themselves.[12] The Third District Court of Appeals found a breach of fiduciary duty because the defendants failed to “give notice to the other partners of any profit derived by him without the consent of all the partners.”[13] Additionally, the court found the parties breached their fiduciary duties by failing to receive consent to receive a portion of the sales commission and because they failed to disclose the sale to the other partners.[14]

Where one has breached his or her fiduciary duty leads to a second inquiry: whether there are damages as a result of the breach. In determining whether there is a liability for a breach of fiduciary duty, a court will look to whether:

Any officer or director…who has contracted on behalf of the association with himself, or with another corporation in which he is or becomes substantially interested, or with another for his personal benefit may be liable to the association for that amount by which was unjustly enriched as a result of the contract.[15]

Therefore, liability for any damages stemming from a breach of fiduciary duty depends on a number of factors, including: whether the breach caused any of the members or the company to lose an opportunity, such as the chance to sell their interest in the business or the opportunity to merge with another company.

In conclusion, the LLC operating agreement does not modify the statutory duties of loyalty and care. An officer, director, manager, or a member of a member-managed LLC owes the company and its other members the fiduciary duties of loyalty and care and is obligated to act in good faith. Therefore, individuals serving in these roles must not compete with the company’s affairs or activities. Reflecting on the earlier example, the sale of a portion of one’s interest in the company could potentially undermine the purpose of the corporation, or it may detract or eliminate benefits that flowed from that person’s ownership interest. Examining one’s fiduciary duty is somewhat similar to playing with fire: it’s better for the manager or member to play it safe, or someone may get burned.

***********************************

[1] Fla. Stat. § 605.0111.

[2] Fla. Stat. § 605.0111.

[3] Fla. Stat. § 605.4091(1).

[4] Fla. Stat. § 605.0105(3)(e-f).

[5] Fla. Stat. § 650.04091.

[6] Fla. Stat. § 650.04091(2).

[7] Fla. Stat. § 650.04091.

[8] Old Port Cove Property Owners Association v. Ecclestone, 500 So. 2d 331, 333 (Fla. 4th DCA 1986).

[9] Id., (quoting Avila South Condominium Association v. Kappa Corp., 347 So 2d 599 (Fla. 1977)).

[10] Id., at 335.

[11] Grossman v. Greenburg, 619 So. 2d 406, 407 (Fla. 3rd DCA 1993).

[12] Id.

[13] Id.

[14] Id.

[15] Id., at 333 (quoting Avila South Condominium Association v. Kappa Corp., 347 So. 2d 599 (Fla. 1977)).

Form 8971 Initial Deadline Update – The IRS Kicks the Can Down the Road Even Further, Delaying the Need to Report & Strictly Adhere to Basis Information as Filed in a Required Estate Tax Return

by Christopher Denicolo

The IRS released Notice 2016-27 to postpone the due date for the first set of Forms 8971 until June 30, 2016. The IRS had previously made the initial due date for filing Forms 8971 as February 29, 2016, and the IRS previously delayed this until March 31, 2016. Now this deadline has been postponed by three more months, the purpose of which was likely to give practitioners additional time to digest and understand the proposed regulations issued by the IRS earlier in March.

As a result of this Notice, the Form 8971 and the Schedules A attached thereto are due before the later of (a) thirty (30) days after the Form 706 (Federal Estate Tax Return) is filed; or (b) June 30, 2016. Please note, however, that this form is required to be filed for estates for which the federal estate tax return is due or actually filed after July 31, 2015.

The text of the Notice is not yet available on the IRS’s website, but should be soon. We hope that it is available by the next Thursday Report, and we will update you as to any further developments with respect to this as they occur.

A Simple Formula to Engage Your Team to Reach a Goal

by David Finkel

David Finkel is the Wall Street Journal bestselling author of SCALE: Seven Proven Principles to Grow Your Business and Get Your Life Back, which can be viewed by clicking here. As the CEO of Maui Mastermind, he has worked with 100,000+ business coaching clients and community members to buy, build, and sell over $5 billion worth of businesses.

Getting your team to buy into your company goals and culture is no simple feat. Here is an interesting example to how one California service business got its team to step up in a big way.

The business is Ablitts Fine Cleaners, the largest and most successful dry cleaners in Santa Barbara, California. Now, before you say, “But David, what can I learn about engaging my team in our company goals from a dry cleaner?” I want you to remember that innovative, sound business-best practices can be found in any industry. Ablitts has a lot to teach.

Ablitts dominates its market in Santa Barbara, and one of the reasons besides its high quality is the free “concierge” level service that offers complimentary pick-up and delivery from your home or office.

Now, you might wonder how Ablitts can afford to offer this type of service without charging extra.

To find out how Ablitts can afford to offer concierge service for free, as well as how they are keeping their young employees thoroughly engaged, involved with the business and eager to meet the concierge service goals, please click here to continue reading this article on inc.com. You can also follow David on Twitter: @DavidFinkel.

Richard Connolly’s World

A Focus on Estate and Tax Planning

Insurance advisor Richard Connolly of Ward & Connolly in Columbus, Ohio often shares with us pertinent articles found in well-known publications such as The Wall Street Journal, Barron’s, and The New York Times. Each week, we will feature some of Richard’s recommendations with links to the articles.

This week, the first article of interest is “Congress Cracks Down on Inheritors’ Tax Loophole” by Ashlea Ebeling. This article was featured on Forbes.com on December 16, 2015.

Richard’s description is as follows:

There’s a dirty secret that when selling inherited property, some beneficiaries overstate the original value of it on their income tax returns to lessen the tax hit. That’s long irked the Internal Revenue Service, and a new law tucked into the summer’s highway bill cracks down on the practice. Although executors and beneficiaries of estates with tax returns filed after July 31, 2015 have to mind the new law, they’re still stuck waiting for Internal Revenue Service guidance on exactly what to do by a February 29, 2016 deadline.

Penalties could be significant. Under the new law, effective for estate returns filed after July 31, 2015 (taxable or not), executors have a new duty to report to the beneficiaries and the IRS the value of specific assets on the estate tax return. In the case of taxable estates, the beneficiaries are then tied to the value the estate puts on an asset, or they face a 20% penalty applied to the underpayment due to the inconsistent basis position.

Please click here to read this article in its entirety.

The second article of interest this week is “Free-Basing for Estate Planners” by David H. Lenok. This article was featured on WealthManagement.com on January 14, 2016.

Richard’s description is as follows:

For the past several years, estate planners have been in a bit of a tizzy. Starting with the gradual increase in the estate and gift tax exemption amounts during the second Bush administration and continuing in more recent years when lawmakers made permanent the portability provisions for spouses to inherit unused lifetime gift and estate tax exemptions from their partners, fewer clients actually require estate tax planning.

One of the answers that the estate-planning community has come to is a renewed focus on income tax. “Basis” has become one of the new buzzwords for estate planning practitioners.

Please click here to read this article in its entirety.

Thoughtful Corner

Don’t Forget Your Contact Information!

by Alan Gassman

Please put your contact information on your website!

Like many others, we often will go immediately to the website of another professional or a potential client to see what they are about. The website building and maintenance industry is obviously trying to capture emails and information, and many web designers are carelessly not making the phone number, street address, and/or public email addresses of professionals and businesses readily available to those who visit the website.

How confidential is an email that comes through a website provider? Many of us have doubts.

You can copy and paste this Thoughtful Corner into an email to your web provider or whoever handles your website for your firm, company, or charity.

Consider the following questions: Is the primary information needed for contact and otherwise readily available on two or more of your website’s pages? Can the viewer find you individually on a company website, and can they find the most important information about you within 20-30 seconds of getting to the website?

Jim Gulecas, Esquire, used to call the Internet the “World Wide Wait” back when things were very slow. Don’t let your website feel like the World Wide Run-Around! Let those who wish to interact with you get straight to the point without having to go through an additional site like LinkedIn, Facebook, or another public forum.

Please feel free to share this with others.

Humor! (or Lack Thereof!)

Sign Saying of the Week

*************************************

********

The Progress of Civilization

by Ron Ross

In the Stone Age, rocks could be chipped to a sharp edge,

So if someone grabbed your mate by the ear,

And you had tied that stone to a long wooden stick

You could stab that person with a thing called a spear.

In the Bronze Age, tin was mixed with copper.

On the farm, someone might steal your wheelbarrow,

But because you had animal gut strung between ends of a stick

You could shoot that guy with a bronze tipped arrow.

In the Iron Age, the ore was melted and cooled

This was time when you could be called by your feudal lord

And you would be given a weapon to fight off invaders

So you could jab that invader with your iron sword

We sophisticated people live in a legal age

It’s part of our long, semi-civilized journey

But our primitive passions lurk just underneath

So get your car out of my yard, or I’ll call my attorney!

Upcoming Seminars and Webinars

Calendar of Events

LIVE TAMPA PRESENTATION:

2016 FLORIDA TAX INSTITUTE – PLEASE DON’T MISS THIS INCREDIBLE 3-DAY EVENT

The 2016 Florida Tax Institute, organized by the University of Florida Levin College of Law, will feature top speakers in the United States on tax, business, and estate planning issue. This program is designed to be informative, engaging, and state of the art!

For a full conference agenda, please click here. Up to 24 hours of continuing education legal credit will be available in several states, while Accounting, Certified Financial Planner, Certified Trusts and Financial Advisor, and Enrolled Agents PACE credit will be available nationwide.

Be sure to visit our table and check out the new Alan Gassman Channel at InterActive Legal!

Date: Wednesday, March 30, 2016 – Friday, April 1, 2016

Location: Tampa Marriott Waterside | 700 S. Florida Avenue, Tampa, FL 33602

Additional Information: To register for this event, please click here. For more information, please email admin@floridataxinstitute.org.

**********************************************************

LIVE COMPLIMENTARY WEBINAR:

Gary Forster, Eric Boughman, and Alan Gassman will present a free, 30-minute webinar on the topic of THE UNIFORM VOIDABLE TRANSACTIONS ACT, which will likely replace the Uniform Fraudulent Transfer Act in the next 18 months. This will be an important new part of Florida law and your planning. Don’t miss it!

There will be two chances to attend this presentation.

Date: Tuesday, April 12, 2016 | 12:30 PM or 5:00 PM

Location: Online webinar

Additional Information: To register for the 12:30 PM presentation, please click here. To register for the 5:00 PM presentation, please click here. For more information, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE MIAMI PRESENTATION:

FLORIDA BAR WEALTH PROTECTION CONFERENCE

The Annual Florida Bar Wealth Protection Conference in Miami on Thursday, April 14th and Friday, April 15th will definitely be our best program ever! You can attend one or both days.

Speakers will include Barry Engle, Howard Fisher, Michael Markham, Denis Kleinfeld, Jonathan Gopman, Alan Gassman, and many others!

A Thursday evening dinner with the speakers and a post-dinner small group discussion and workshop on Practice Acceleration will be available only to those who attend the live sessions.

The official brochure for this program can be viewed by clicking here.

Date: Thursday, April 14th, 2016 and Friday, April 15th, 2016

Location: Hyatt Regency Miami | 400 SE 2nd Avenue, Miami, FL 33131

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE COMPLIMENTARY BLOOMBERG BNA WEBINAR:

Ken Crotty, Christopher Denicolo, and Jerry Hesch will present a free, one-hour webinar on the topic of MATHEMATICS FOR ESTATE PLANNING: ESSENTIAL AND DYNAMIC PLANNING TECHNIQUES THAT CAN BE UNDERSTOOD BY CLIENTS AND MUST BE IMPLEMENTED BY ADVISORS.

This webinar is part of the Bloomberg BNA Essential Elements series and will be moderated by Alan Gassman.

Date: Tuesday, April 19, 2016 | 12:30 PM

Location: Online webinar

Additional Information: To register for this presentation, please click here. For more information, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE (not so complimentary) BLOOMBERG BNA WEBINAR:

Stacy Eastland will present a one-hour webinar on the topic of PULLING THE RABBIT OUT OF THE GRAT HAT: SOME OF THE MOST CREATIVE STRUCTURAL GRAT PLANNING IDEAS WE’VE SEEN OUT THERE.

This webinar is part of the Bloomberg BNA Practical & Creative Planning series and will be moderated by Alan Gassman.

Date: Thursday, April 21, 2016 | 12:30 PM

Location: Online webinar

Additional Information: To register for this presentation, please click here. For more information, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE UNIVERSITY OF MIAMI PRESENTATION:

Alan Gassman will be speaking to LL.M. in Estate Planning students (in their last week of classes!) at the University of Miami for a 4-hour interactive workshop entitled A CRUCIAL KNOWLEDGE AND TECHNIQUE CHECKLIST FOR SOPHISTICATED ESTATE PLANNERS. This talk will include valuable forms, materials, and information on a variety of topics, including:

- Florida Law and Asset Protection for the Sophisticated Estate Planner

- Drafting & Special Considerations for Planning for Same-Sex Couples

- What You Really Need to Know About GST Planning

- What Your Clients Will Appreciate Knowing About Life Insurance

- How to be a Successful and Happy Estate Planner

We thank Tina Soriano, a student in the program who attended the August 2015 presentation at Ava Maria School of Law for students and alumni, and Professor Dennis Calfee of the University of Florida Tax Program for their encouraging words and advice on how to best serve the needs of future estate planners.

Lunch is on us if you RSVP!

Date: Tuesday, April 26, 2016 | 12:00 PM – 4:00 PM

Location: University of Miami | 1320 S. Dixie Highway, Coral Gables, FL 33146

Additional Information: For more information or to RSVP, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE COMPLIMENTARY MAUI MASTERMIND WEBINAR:

Wall Street Journal and Business Week bestselling author David Finkel will present a special, free, one-hour webinar for our clients and friends on the topic of MORE WITH LESS: 5 SIMPLE STEPS TO ENJOY MORE BUSINESS GROWTH AND GREATER PERSONAL FREEDOM BY DOING LESS.

Date: Thursday, April 28, 2016 | 12:00 PM – 1:00 PM

Location: Online webinar

Additional Information: To register for this presentation, please click here. For more information, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE INTERACTIVE LEGAL MELBOURNE, FL/LIVE FEED TO YOUR OFFICE PRESENTATION:

Alan Gassman will be speaking at the Florida Institute of Technology Media Center on FLORIDA PLANNING FOR THE AFFLUENT AND NOT SO AFFLUENT: WHAT YOU NEED TO KNOW AND DO. This talk will include many techniques that can be used in all 50 states and Guam. If you are from Guam, you get a discount!

This will be a live presentation for those who can attend and will feature a simultaneous, live online streaming broadcast. Watch or listen right from the comfort of your own office or join us in Melbourne before visiting the Kennedy Space Center or Ron Jon’s Surf Shop.

Date: Wednesday, May 4, 2016 | Tentative time: 2:00 PM – 3:30 PM

Location: Florida Institute of Technology Media Center | 150 W. University Blvd, Melbourne, FL 32901

Additional Information: For more information or to RSVP, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE NAPLES PRESENTATION:

3RD ANNUAL AVE MARIA SCHOOL OF LAW ESTATE PLANNING CONFERENCE

This one-day conference will take place in Naples, Florida on Friday, May 6, 2016.

On Thursday, May 5, there will be a special dinner with Jonathan Blattmachr. Jonathan will also present at the conference on Friday. Be sure to bring an extra pair of socks because the first pair will get knocked off by Jonathan’s talk!

Alan’s Friday morning presentation will be entitled COFFEE WITH ALAN: AN INTRODUCTION TO SELECT ESTATE PLANNING AND ASSET PROTECTION STRATEGIES. During this session, Alan will offer an overview of the topics that will be presented throughout the Estate Planning Conference. Attendees new to these specific estate planning areas will find the presentation useful and helpful.

Alan will also moderate the Luncheon Speaker Panel with Jonathan Blattmachr, Stacy Eastland, and Lee-ford Tritt. The panel will cover the topic of WHAT WE WISH WE KNEW WHEN WE STARTED PRACTICING LAW – NON-TAX AND PRACTICAL ADVICE FOR ESTATE PLANNERS YOUNG AND OLD.

Date: Friday, May 6, 2016

Location: Ritz Carlton Golf Resort | 2600 Tiburon Drive, Naples, FL, 34109

Additional Information: For more information, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE BLOOMBERG BNA WEBINAR:

Jonathan Blattmachr will present a one-hour webinar on the topic of FUNDAMENTALS, FINE POINTS, AND INNOVATIVE STRATEGIES FOR LIFE INSURANCE AND USE THEREOF.

This webinar is part of the Bloomberg BNA Practical & Creative Planning series and will be moderated by Alan Gassman.

Date: Tuesday, May 10, 2016 | 1:00 PM

Location: Online webinar

Additional Information: To register for this presentation, please click here. For more information, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE COMPLIMENTARY MAUI MASTERMIND WEBINAR:

Alan Gassman will present a free, 45-minute webinar on the topic of EQUITY STRIPPING AND OTHER ADVANCED ASSET PROTECTION IDEAS.

This webinar will be specially made for and presented in partnership with Maui Mastermind. Clients, advisors, and colleagues of Gassman, Crotty & Denicolo are welcome to attend.

Date: Wednesday, May 11, 2016 | 12:30 PM

Location: Online webinar

Additional Information: To register for this presentation, please click here. For more information, please contact Alan Gassman at agassman@gassmanpa.com.

**********************************************************

LIVE TAMPA PRESENTATION:

MAUI MASTERMIND ACCREDITED INVESTOR WEALTH WORKSHOP

Maui Mastermind will present their three-day ACCREDITED INVESTOR WEALTH WORKSHOP on July 21st – 23rd.

The first two days of this event will feature three speakers: David Finkel, Kevin Bassett, and Alan Gassman, on a variety of topics including advanced asset protection topics, reducing your tax drag, creating more with less, and how to create and sustain rapid growth of your business or company.

Saturday, July 23rd will feature a bonus add-on to the program entitled SCALE YOUR MEDICAL PRACTICE: PROVEN STRATEGIES TO GROW YOUR PRACTICE, INCREASE YOUR CASH FLOW, AND CREATE MORE PERSONAL FREEDOM. This event will feature David Finkel’s presentation on scaling a medical practice.

Watch this space as more details will be forthcoming!

Date: Thursday, July 21st – Saturday, July 23rd

Location: Tampa Marriott Westshore | 1001 N. Westshore Blvd., Tampa, FL, 33607

Additional Information: For more information, please email Alan Gassman at agassman@gassmanpa.com.

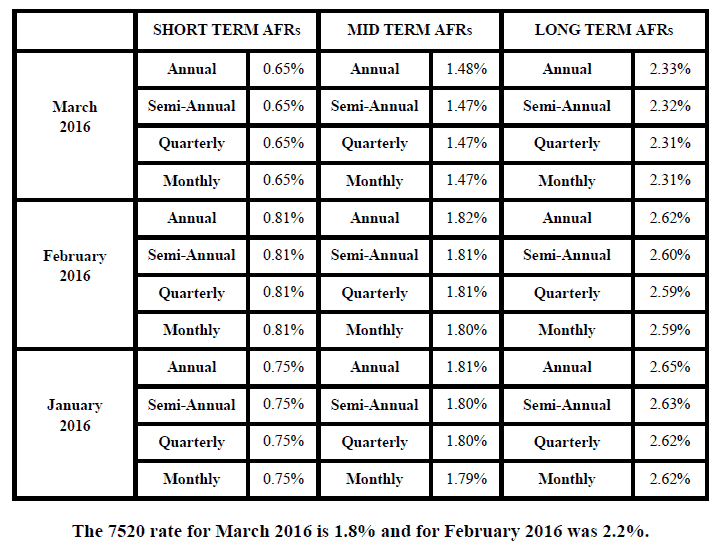

Applicable Federal Rates

Below we have this month, last month’s, and the preceding month’s Applicable Federal Rates, because for a sale you can use the lowest of the 3.